Bayesian spatial models for estimating means of sampled and non-sampled small areas

Section 2. Some spatial alternatives to the independent FH model

2.1 Incorporating spatial random effects

Let be the -component vector with the direct estimates of

small areas, and be the diagonal matrix with the sampling variances of

the direct estimates. We denote by the -component vector of small area means. Also,

let

be the -component vector of auxiliary variables

(including the intercept term) for the small area, and A special case of the HB model given in

(1.2)-(1.4) can be expressed as

where is the -component regression coefficient vector, is the model error variance, and is the identity matrix of order The uniform prior (2.3) on the model

parameters is a popularly used noninformative prior, and the resulting

posterior pdf is proper provided that See Berger

(1985) and Datta and Smith (2003) for detailed discussion.

The model (2.2) assumes that are independently distributed over the small

areas with common random effects variance In many small area estimation problems,

however, the area characteristic of interest is closely related to geographical

factors such as population size, ethnicity, age-group and education level. When

available covariates do not fully explain such spatial association, the

independence and equal variance assumptions of random effects fail, and

inference based on the hierarchical model (2.1)-(2.3) may generate unreliable

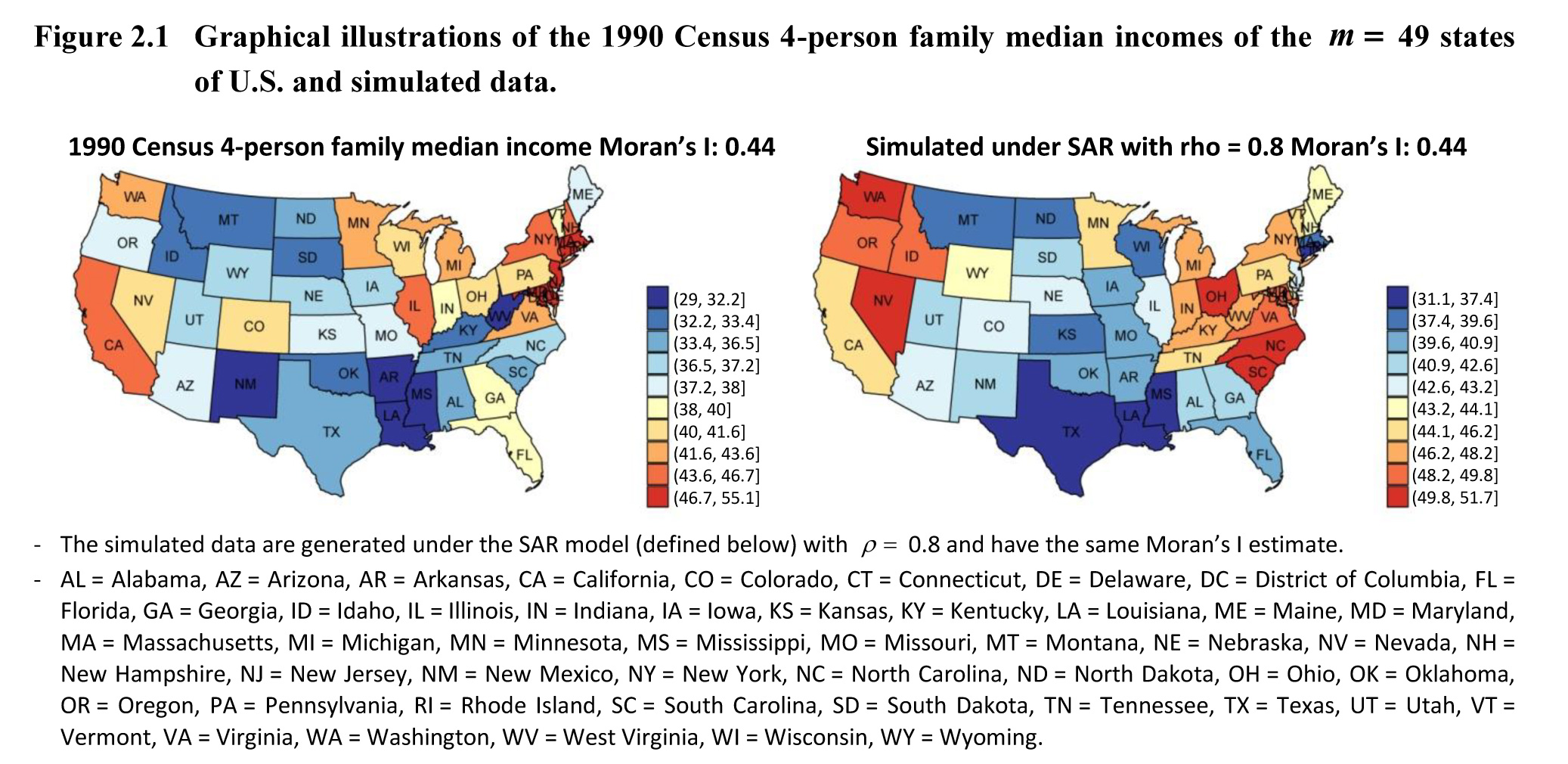

estimates, consequently resulting in erroneous decisions. Figure 2.1

illustrates spatial associations of the 1990 Census 4-person family median

incomes of (scaled by $1,000) the states of the U.S., including the District of

Columbia. Simulated data with the same Moran’s I value are also displayed for

comparison, where Moran’s I is a measure for spatial autocorrelation. The

simulated data are generated under the SAR model (defined below) with 0.8 matching the location and scale with the

Census data. The two panels demonstrate the existence of spatial dependence in

the 1990 Census 4-person family median incomes. In practice, covariates capable

of fully capturing existing spatial variation are not always available, and the

problem can be exacerbated if lurking variables exist, as they introduce

additional variability that cannot be explained by the independently and

identically distributed (i.i.d.) random effects.

Description of Figure 2.1

Figure illustrating the spatial associations of the 4-person family median incomes of 49 states of the U.S., including the District of Columbia, from the 1990 Census (on the left) and from simulated data (on the right). The legends at the right of each figure indicate the color coding by median income bracket scaled by $1,000. The two figures demonstrate the existence of spatial dependence in the 1990 Census 4-person family median incomes.

To address this issue, we

propose to use spatially correlated random effects. Let

be the adjacency matrix which plays an

important role in capturing spatial dependency. In particular, if the and small areas are connected via geographical

boundary or through other mechanisms (for example, air traffic), and otherwise. Also, for The off-diagonal entries, need not be binary; they can take other

positive values, such as the “length” of the geographical border or volumes of

air traffic between the two areas. Since the adjacency matrix is symmetric, its eigenvalues are real. We

denote the largest eigenvalue of by such that Since is non-null and we get as a result that Let be the sum of the row of and

Assuming that diagonal elements of are positive, i.e., all small areas have at

least 1 neighboring area, we define Since is a row stochastic matrix, all of its

eigenvalues are between -1 and 1, with at least one of them is 1. Consequently,

Moreover, and have the same set of eigenvalues, and the

latter matrix is symmetric. So all the eigenvalues of are real, and will be negative. We consider four alternative

spatial dependencies associated with random effects, which are represented by

the following positive definite precision matrices (excluding the scale

parameter

where is the spatial dependence parameter that

represents the strength of spatial dependence (Hodges, 2019, Chapter 5.2)

and is defined as Since the eigenvalues of are between 0 (the smallest eigenvalue) and (the largest eigenvalue, the matrix is nonnegative definite. Each precision matrix

is guaranteed to be positive definite as long as is in the range specified in the respective

definition.

The adjacency matrix of the simultaneous autoregressive (SAR) model

(Whittle, 1954) is

row-normalized so that can vary from -1 to 1 while preserving the

positive definiteness (Banerjee,

Carlin and Gelfand, 2003,

Chapter 4.4). The model (2.5) is a simple version of conditional

autoregressive (CAR) model (Rao and

Molina, 2015, Chapter 9.6.2), where diagonal entries of the

precision matrix are all equal to one. Even though the diagonal elements of a

precision matrix are all equal, the diagonal elements of the inverse may not be

all equal, leading to heteroscedasticity of random effects. We call this model

the simple conditional autoregressive (SCAR) model. The model (2.6) is widely

used conditional autoregressive model (CAR; Banerjee et al., 2003; Besag and Kooperberg, 1995; You and Zhou,

2011), where diagonal entries of the precision matrix are the number of

neighborhoods of the corresponding area. The upper limit of is and in the case of the model with is referred to as the intrinsic autoregressive

(IAR) model (Banerjee et al.,

2003, Chapter 4.3). The model (2.7) is a conditional autoregressive model, which we call

Leroux’s

conditional autoregressive (LCAR), whose precision matrix is given by

the convex combination of and This model has been considered by Leroux, Lei

and Breslow (2000); MacNab (2003); You

and Zhou (2011), where the diagonal element of is the number of neighborhoods of the small area, and the off-diagonal element is -1 if the and the small areas are connected and 0 otherwise.

The conditional autoregressive

models, SCAR, CAR, and LCAR, assume that depends only on neighboring small area means.

In other words, is correlated with only through the means of surrounding areas.

On the contrary, the SAR model assumes that is dependent on all other concurrently, but has stronger (weaker) correlations for

neighboring (remote) areas. The independent FH model can be viewed as a special

case of the SAR, SCAR, or LCAR model with For notational convenience, we include the

independent FH model as part of our model by taking its precision matrix although it is free from

We consider the following HB spatial models

incorporating the five spatial dependencies defined in (2.4)-(2.7):

where is the model scale parameter, and are suitable functions of and and are the lower and upper bounds of under the model. We avoid the term “model error variance”

for as diagonal entries of vary across small areas and are not

necessarily all one.

2.2 Estimation of population means of non-sampled

small areas

In this section, we consider the

case when, in the survey, there are several non-sampled small areas that have

no direct estimates. In many applications, limited resources frequently

preclude the inclusion of many subpopulations in the sample, resulting in

non-sampled small areas. In this section, we consider the case when, in the

survey, there are several non-sampled small areas that have no direct

estimates. In many applications, limited resources frequently preclude the

inclusion of many subpopulations in the sample, resulting in non-sampled small

areas. Non-sampled small areas are sometimes referred to as misaligned areas (Trevisani and Gelfand, 2013) when

they arise from domain misalignment between the direct estimate and auxiliary

variables. For any of these non-sampled areas, the prediction of its mean from

any non-spatial model is only based on its synthetic estimator. We propose to

exploit spatial dependencies in predicting area means of non-sampled small

areas. The predictions of the proposed models are obtained by modifying its

synthetic estimator, using the vector of regression residuals, with more

emphasis on the regression residuals of the neighboring areas.

Without loss of generality, let

there be non-sampled small areas and be the direct estimates of the sampled small areas. Based on the direct

estimates of sampled areas, we consider the following HB

models:

where and which is the subvector of corresponding to the sampled areas.

2.3 Propriety of the posterior distributions

In this section, we establish

propriety of the posterior distributions of spatial small area models given in

(2.8)-(2.10) and (2.11)-(2.13). Let

be the indicator function taking the value 1

when its argument is true and 0 otherwise. We first provide general conditions

for the posterior propriety of the proposed models.

Theorem 1. For all the HB spatial models

given in (2.8)-(2.10) and (2.11)-(2.13), the posterior probability density

functions are proper if the following conditions hold for some positive

constant

- (a)

- (b)

- (c)

where for (2.8)-(2.10), and for (2.11)-(2.13).

If

is a proper pdf, then (a) holds true

automatically, and (b) is satisfied if The condition is obvious since at least observations are needed to estimate components of when no substantive information about it is

available. Also, any bounded function of satisfies in Theorem 1 as their supports are all

bounded. In particular, under the popular family of noninformative priors

the posterior pdfs are proper under the following

conditions.

Corollary 1. For any of the HB spatial

models given in (2.8)-(2.9) and (2.11)-(2.12) with the prior in (2.14), the

posterior pdf is proper as long as and

For the uniform prior

with (which

will be used in this paper), the propriety of the posterior distributions for

models (2.8)-(2.9) are guaranteed as long as the number of small areas is

greater than For the

models incorporating non-sampled areas given in (2.11)-(2.12), the second

condition of Corollary 1.1 becomes and

thus, the posterior pdfs are proper as long as the number of non-sampled areas

is fewer than or at

least areas

have sample.