Local polynomial estimation for a small area mean under informative sampling

Section 5. Simulation study

The set-up of the

simulation study follows the one used in Verret et al. (2015). We

considered a population with

15 small areas and

15 units within each small area. The relatively

small number of small areas and units within areas were chosen so as to

alleviate the computational burden. We used a single auxiliary variable

The

population

-values were generated from a gamma

distribution with mean 10 and variance 50. The population

-values were generated by the following model

where

and

with

0.5 and

2.

We considered a single sample size,

3, within a small

area. We used Conditional Poisson Sampling (CPS) to select unequal probability

samples within the small areas, with probabilities proportional to specified

sizes

(see Tillé,

2006, Chapter 5). We considered two different choices of the sizes

in the

simulation study. The first choice uses

where

The size

measures (5.2) are equivalent to those used by Pfeffermann and Sverchkov (2007)

in their simulation study and satisfy the relationship (2.5) on the weights

The second choice of size measures, following

Asparouhov (2006), involves two different types of size measures: invariant (I)

and non-invariant (NI). For the invariant case,

is

independent of

given

otherwise, it is called non-invariant.

Invariant size measures are given by

Non-invariant

size measures are taken as

where the

random pair

is

generated independently of

using

the same distributions as

and

These

size measures were used by Asparouhov (2006). The

coefficient

controls

for the variation of the weights and the value

controls

the level of informativeness of the sampling design. We chose

0.5 and

and

corresponding to several levels of

informativeness generated by

in (5.3)

and (5.4). Increasing

decreases informativeness, with

corresponding to non-informative sampling. If

some of the

exceeded

one, they were set to one, and the probabilities were recomputed for the

remaining units.

5.1 Performance of

the local polynomial estimator of

We compared the

bias and mean squared error of the estimators

and

The

EBLUP estimator

based on

(1.1) assumes that the sample model coincides with the population model,

thereby ignoring the informativeness of the sampling design. We studied two versions of

investigated by Verret et al. (2015) for

various choices of

that

account for informativeness. They are

EBLUP estimators based on the augmented sample model (1.2). They are denoted as

when

and

when

We

report results only for these

functions, as

they outperform others given in Verret et al. (2015). Finally,

represents our new local polynomial estimator.

The bias and the

mean squared error of the estimators were computed using

1,000 simulated samples selected under a design-model approach. For each run,

we first

generated the population

-values under the population model (5.1) and

computed

the mean

of the small area

in the

generated population. Samples of sizes

were

then selected within the small areas using CPS with probabilities proportional

to specified sizes

given by

(5.2) for the Pfeffermann and Sverchkov (2007) (PS) size measures, and (5.3)

and (5.4) corresponding to the invariant and non-invariant cases in the case of

the Asparouhov (2006) (AP) size measures. From each simulated sample

the

estimates

and

were

computed for each small area

An

optimal bandwidth

was

found for

using

the cross-validation criterion. A grid of the form (0.01, 0.02, 0.03,…,

0.15) covered the possible values for

in

populations generated by (5.1).

For a given

estimator of the small area mean

we considered

the following performance measures:

Average Absolute Bias

where

Average Root Mean Squared Error

Table 5.1

reports on the average absolute bias

of

estimators

and

under

the PS size measures (5.2) and AP size measures (5.3 and 5.4) for

and

Table 5.1

Average absolute bias for the PS and AP size measures

Table summary

This table displays the results of Average absolute bias

for the PS and AP size measures. The information is grouped by Estimator

Generation of

(appearing as row headers),

without

and

and (appearing as column headers).

| Estimator |

without

|

|

|

|

| Generation of |

| PS |

0.309 |

0.020 |

0.004 |

0.011 |

| AP |

|

I |

0.431 |

0.002 |

0.036 |

0.004 |

| NI |

0.425 |

0.010 |

0.035 |

0.005 |

|

|

I |

0.206 |

0.017 |

0.022 |

0.024 |

| NI |

0.219 |

0.019 |

0.016 |

0.016 |

|

|

I |

0.139 |

0.005 |

0.012 |

0.033 |

| NI |

0.137 |

0.008 |

0.013 |

0.019 |

|

|

I |

0.008 |

0.008 |

0.008 |

0.026 |

| NI |

0.006 |

0.006 |

0.006 |

0.021 |

As observed in Verret et al. (2015), the

of the

EBLUP estimator

with

just the auxiliary variable

is quite

a bit larger than those based on the augmented models

and

and the

local polynomial method. This holds regardless of how the size measures have

been generated (PS or AP). The

of

attains

its highest value (0.431) when the design is very informative

and

decreases as

increases. This observation also holds for the

estimators based on the augmented models. The inclusion of

or

as an

augmenting variable, in the model results in small

with the

highest being 0.036. Comparing the

of the

local polynomial estimator

to those

associated with the VRH augmented models, we observe that they are comparable

for

and

and

slightly larger for

Table 5.2 reports the simulation results

on the average root mean squared error

of the

estimators for both the PS size measures (5.2) and the AP size measures (5.3

and 5.4) for

and

The

EBLUP,

based on

model (1.1) without the augmenting variable

has the

largest

(0.740

for I and 0.752 for NI) for the AP size measures corresponding to

and

0.685 for the PS size measure. The

decreases as

increases: 0.608 for I and 0.610 for NI in the

case of non-informative sampling

The

for

and

are

significantly smaller than those associated with

when

sampling is very informative

and for the PS size measure. There are small

differences in terms of

between

our non-parametric approach and the parametric approach in Verret et al.

(2015).

Table 5.2

Average root mean squared error

for the PS and AP size measures

Table summary

This table displays the results of Average root mean squared error

for the PS and AP size measures. The information is grouped by Estimator

Generation of

(appearing as row headers),

without ,

, ,

and

(appearing as column headers).

| Estimator |

without

|

|

|

|

| Generation of

|

| PS |

0.685 |

0.229 |

0.200 |

0.200 |

| AP |

|

I |

0.740 |

0.089 |

0.170 |

0.087 |

| NI |

0.752 |

0.158 |

0.200 |

0.149 |

|

|

I |

0.644 |

0.562 |

0.568 |

0.557 |

| NI |

0.650 |

0.557 |

0.555 |

0.555 |

|

|

I |

0.617 |

0.588 |

0.591 |

0.612 |

| NI |

0.619 |

0.587 |

0.589 |

0.607 |

|

|

I |

0.608 |

0.619 |

0.621 |

0.626 |

| NI |

0.610 |

0.622 |

0.625 |

0.629 |

When the sampling is less informative

the

local linear estimator

is

better than

but its

is

slightly larger than those associated with the parametric estimators

and

In this

case, we observe that the estimated function

is close

to a flat line, and this implies that the local linear approximation is not as

appropriate. This explains why

is

slightly worse than

and

when the

level of informativeness of the sampling is low. A local polynomial estimator

performs well when the function

is

meaningfully non-constant.

When the sample is non-informative

is

better than

and

in both

invariant and non-invariant case. This conclusion is somewhat different from

that of Verret et al. (2015) where for

their

estimators

and

have

equal

and

values.

Verret et al. (2015) used both larger populations and samples, and this

may explain why their augmented models produced estimators as good as the

population model under non-informative sampling designs. Under our simulation

set-up, we found that the

and

of the

EBLUP are small for

values

larger than 6: this corresponds to a sample design that is almost

non-informative. In this case, we

recommend using EBLUP.

5.2 Performance of

the MSE estimators

We now turn to the

performance of the bootstrap procedures for estimating the MSEs of the EBLUP,

VRH and local polynomial estimators. Let

be an

estimator of

and

be the

bootstrap estimator of

From

1,000

simulated populations and samples, we

first computed measures of MSE values as

where

is the

true mean, and

is the

value of the estimator for the

population. Let

be the

bootstrap estimator of

It is

denoted as

for the

EBLUP estimator

and

corresponds to the parametric (unconditional) bootstrap method given by

equation (4.2). For our local polynomial estimator

and the

Verret et al. (2015) estimators,

and

the mse

values, denoted as

and

for

and

respectively, are computed using the

conditional parametric bootstrap method of Section 4. For each selected

sample in the

simulated population

we used

400 bootstraps to compute the

value of

that we

denote as

We

considered two measures to evaluate the performance of

average

absolute relative bias and average confidence interval. These measures are

defined as follows:

Average Absolute Relative Bias:

where

Average Confidence Level:

where

and

Table 5.3 reports

simulation results on the average relative bias

of the

MSE estimators for both the PS size measures (5.2) and Asparouhov size measures

(5.3 and 5.4) for

and

Table 5.3

Average relative bias (%) of mse

for the PS and AP size measures

Table summary

This table displays the results of Average relative bias (%) of mse

for the PS and AP size measures. The information is grouped by Estimator

Generation of

(appearing as row headers),

without , , ,

and

(appearing as column headers).

| Estimator |

without

|

|

|

|

| Generation of

|

| PS |

25.4 |

3.9 |

3.4 |

7.7 |

| AP |

|

I |

39.9 |

9.7 |

14.4 |

7.5 |

| NI |

46.6 |

4.1 |

8.7 |

10.0 |

|

|

I |

16.0 |

2.9 |

3.8 |

5.9 |

| NI |

21.4 |

3.8 |

3.5 |

5.8 |

|

|

I |

13.4 |

6.1 |

6.4 |

5.8 |

| NI |

15.4 |

7.3 |

7.4 |

8.8 |

|

|

I |

4.6 |

4.2 |

4.5 |

6.2 |

| NI |

6.1 |

6.4 |

6.3 |

6.9 |

The

of

based on

the model without the augmenting variable

is very

large when the sampling is very informative

39.9%

for I and 46.6% for NI. The

gradually decreases to around 5% under

non-informative sampling

The

of both

the parametric and non-parametric estimators are smaller in general than 10%,

with the exception of 14.4% for the

estimator

that uses

as an

augmenting variable.

Table 5.4 reports

simulation results on the average confidence level

associated with the MSE estimators for both

the PS size measures (5.2) and the AP size measures (5.3 and 5.4) for

and

and

nominal level of 0.95.

Table 5.4

Average confidence level of mse

for the PS and AP size measures

Table summary

This table displays the results of Average confidence level of mse

for the PS and AP size measures. The information is grouped by Estimator

Generation of

(appearing as row headers),

without , , and

(appearing as column headers).

| Estimator |

without

|

|

|

|

| Generation of

|

| PS |

0.898 |

0.937 |

0.941 |

0.936 |

| AP |

|

I |

0.856 |

0.918 |

0.908 |

0.928 |

| NI |

0.834 |

0.930 |

0.920 |

0.934 |

|

|

I |

0.916 |

0.937 |

0.936 |

0.932 |

| NI |

0.907 |

0.936 |

0.933 |

0.936 |

|

|

I |

0.922 |

0.927 |

0.926 |

0.934 |

| NI |

0.918 |

0.930 |

0.933 |

0.926 |

|

|

I |

0.937 |

0.935 |

0.935 |

0.938 |

| NI |

0.934 |

0.934 |

0.933 |

0.931 |

The EBLUP

estimator

has the

worst coverage when the sample design is very informative. The coverage

improves as the design becomes less informative. The coverage of the other

estimators is between 93% and 95%, with the exception of

(the one

that includes

with

coverage slightly lower.

5.3 Inclusion of an augmenting variable

The local polynomial approach results in an automatic way of obtaining a reasonable

augmented model that is a function of the selection probabilities

However,

given that one does not know whether the design is informative or not, should

we always include an augmenting variable in the model? If the sample design is

not informative it is reasonable to use model (1.1). Note that in this case,

including the augmenting variables,

or

has a very small impact either on the absolute

relative bias of the estimator and absolute relative bias of the estimated MSE.

A similar conclusion was obtained in Verret et al. (2015) who used a

larger population and sample size.

The same question arises with respect to the

use of the local polynomial procedure. In this case, the conclusions are not

quite as clear. If the design is very informative, the local polynomial

approach gains in terms of absolute bias and mean squared error when

or

When the

sampling design is less informative

the

parametric approach in Verret et al. (2015) is the better choice, but by a very small margin.

In a practical situation, the value of

is not

known and the decision to use the augmenting variable in a parametric or

nonparametric model should be taken. To this end, we follow the suggested

procedure in Verret et al. (2015) to provide some guidelines on how to

decide on this choice for an arbitrary

data set. Define

and fit

the following model

to the

sample data by ordinary least squares (OLS). The residuals are

where

and

are the

OLS estimators of

and

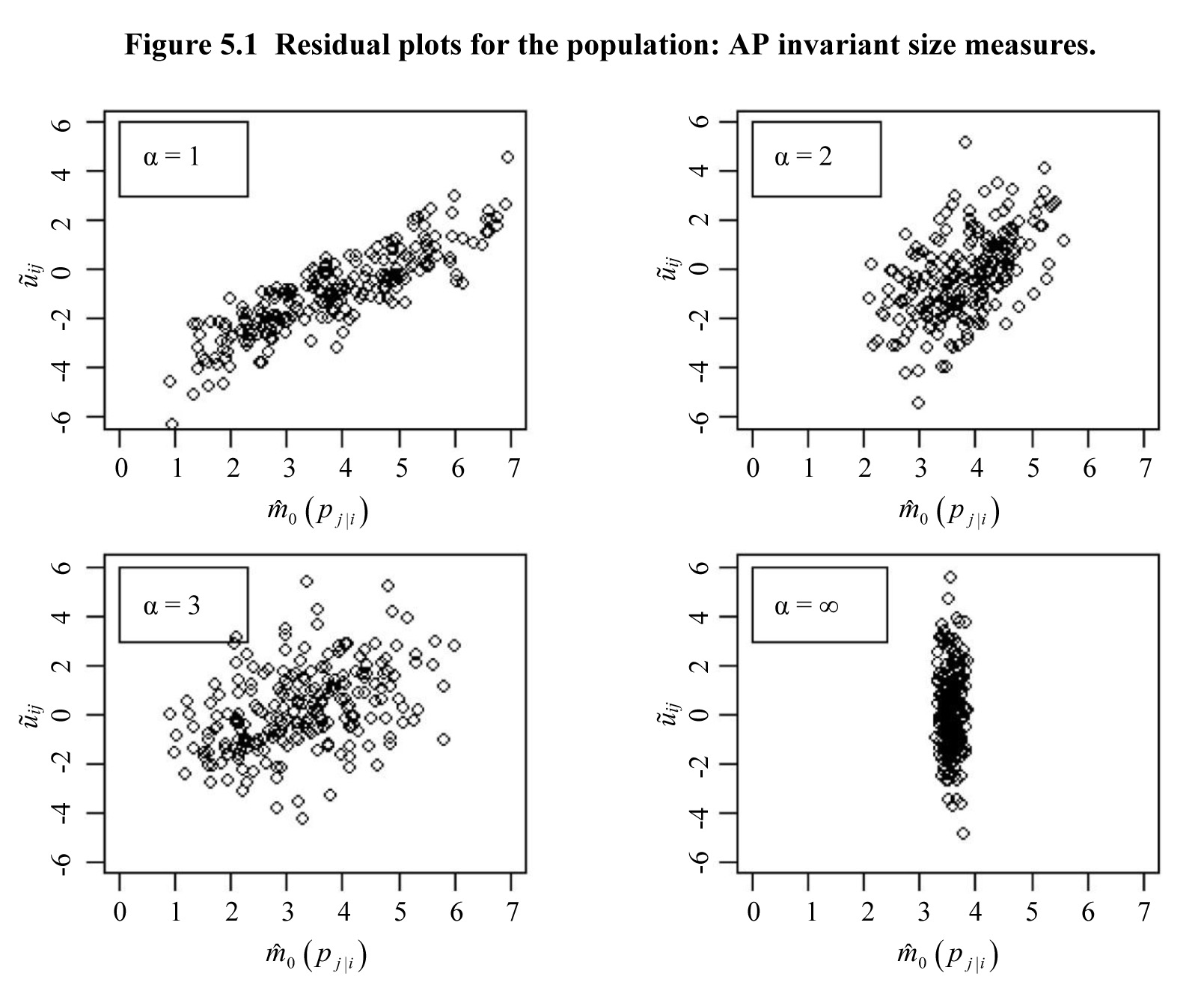

respectively. Figure 5.1 displays

residual plots of

for the

AP measures

and

in the

invariant case. For

the

relationship between

and

is

clearly linear, suggesting that the design is informative. As

increases,

the design is less informative. Note that

is

constant when

Similar

observations hold for the non-invariant case. For the PS size measures the

graph resembled the one given in Figure 5.1 when

Description for Figure 5.1

Figure presenting four scatter

plots, for

is on the y-axis going from -6 to 6.

is on the x-axis, going from 0 to 7. For

the relationship between

and

is linear. As

increases, the linear relationship fades.

is constant, around 4, when

Table 5.5

provides the estimated correlation

coefficients,

for PS

and AP size measures for

and

Table 5.5

Estimated correlation coefficient

for the PS and AP size measures

Table summary

This table displays the results of Estimated correlation coefficient

for the PS and AP size measures. The information is grouped by Estimated correlation coefficient (appearing as row headers), AP, PS and , , and (appearing as column headers).

| Estimated correlation coefficient |

AP |

PS |

|

|

|

|

|

| I |

NI |

I |

NI |

I |

NI |

I |

NI |

|

|

0.870 |

0.850 |

0.450 |

0.510 |

0.240 |

0.210 |

0.007 |

0.001 |

0.800 |

In terms of

we

noticed in Section 5.1 that

is

better than the estimators based on augmented models for

Results

not presented in Table 5.5 show that for

the absolute value of the correlation

coefficient is less than 0.1. On

the basis of this limited simulation, a user could decide on the choice of the

estimator to use for a real data set as follows: i. If

is larger than 0.5, use

ii. If

is less than 0.1, use

iii.

otherwise use

or