Small area estimation for unemployment using latent Markov models

Section 4. The proposed model

In

this section, the proposed SAE model based on LMMs is illustrated. It can be

considered as a compromise between the YRG model based on (3.1), which leads to

possible oversmoothing, and the computationally demanding alternative proposed

in Datta et al. (1999), based on (3.2). We first outline a general

description on LMMs and then move to the specification of the area level model

and to its estimation.

4.1 Preliminaries

In

LMMs, the existence of two types of process is assumed: an unobservable

finite-state first-order Markov chain

with state space

and an observed process, which in our case

corresponds to

with

and

It is assumed that the distribution of

depends only on

specifically, the

are conditionally independent given the

In addition, the latent state to which a small

area belongs at a certain time point only depends on the latent state at the

previous occasion.

The

state-dependent distribution, namely the distribution of

given

can be a continuous or discrete. Such a

distribution is typically taken from the exponential family. Thus, the overall

vector of parameters of LMM, denoted by

includes parameters of the Markov chain,

denoted by

and the vector of parameters

of the state-dependent distribution. In fact,

the model consists of two components, the measurement model and the latent

model, which concern the conditional distribution of the response variables

given the latent variables and the distribution of the latent variables,

respectively. By jointly considering these components, the so-called manifest

distribution is obtained: it is the marginal distribution of the response

variables, once the latent variables have been integrated out.

The

measurement model, based on parameters

can be written as

Moreover, the parameters

of the Markov chain are:

- the vector of initial probabilities

where

- the transition probability matrix

- is the probability that area

visits state

at time

given that at time

it was in state

In

this work we consider homogeneous LMMs, namely LMMs where, in agreement with

the previous definition, the transition probability matrix is constant in time.

Generalizations to non-homogeneous hidden Markov chains and time-varying

transition probabilities could also be considered (Bartolucci and Farcomeni,

2009). Individual covariates could be included in the measurement or in the

latent model. When the covariates are included in the measurement model (Bartolucci

and Farcomeni, 2009), they affect the response variables directly and the

latent process is conceived as a way to account for the unobserved

heterogeneity between areas. Differently, when the covariates are in the latent

model (Vermunt and Magidson, 2002; Bartolucci, Pennoni and Francis, 2007) they

influence initial and transition probabilities of the latent process. In a SAE

context, we will consider the former approach, so that auxiliary information

can be used to improve predictions. Bayesian inference approaches to LMMs are

already available in the literature (e.g., in Marin, Mengersen and Robert,

2005; Spezia, 2010). In the following section we illustrate how to incorporate

an LMM into an area level SAE model.

4.2 Proposed approach to area level SAE

The

proposed model is based on two levels in an HB framework: at the first level, a

sampling error model is assumed, then an LMM is used as linking model. The

latter is based on two equations, corresponding to the measurement model and to

the latent component. In particular, we adopt the following structure:

- Latent Model, based on the initial

probabilities

and on the transition probabilities

already defined.

Here

is the

vector of the regression coefficients for the

latent state to which area

at time

belongs,

is the corresponding error variance, and

is the matrix of sampling variances, which is

assumed to be known.

It

must be noticed that, while in the classical area level SAE models

heterogeneity is modeled using continuous (usually Normally distributed) random

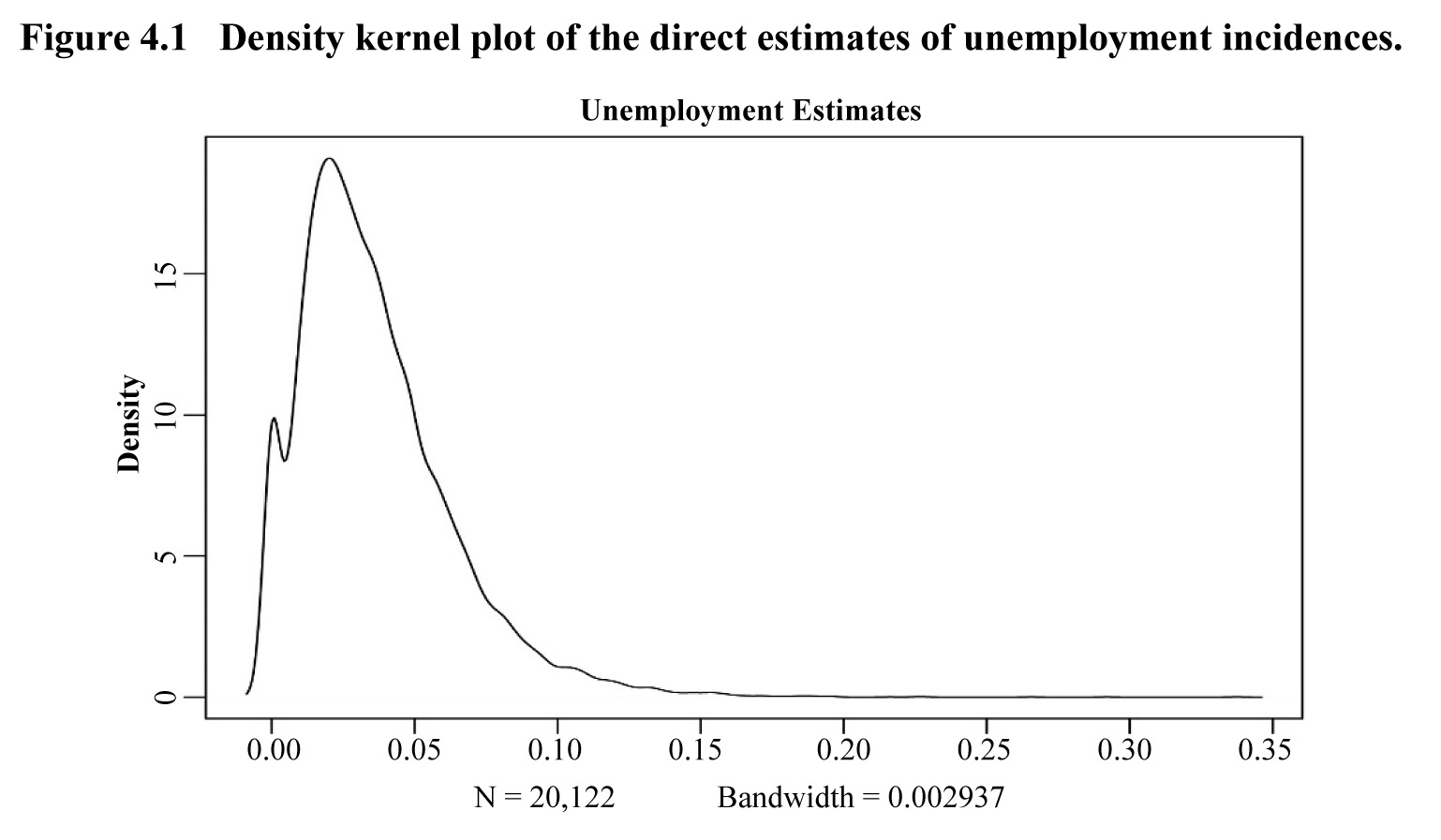

variables, here it is modeled with a discrete dynamic variable. As we can

deduce from Figure 4.1, our data have a skewed distribution. However, the

empirical distribution is not far from a Normal distribution. D’Alò,

Di Consiglio, Falorsi, Ranalli and Solari (2012) show that the differences

in estimates between adopting a Normal or a Binomial model are not as relevant

as expected and Normal models are often used for estimation of unemployment

rates (You et al., 2003; Boonstra, 2014). Finally adopting the Normal

distribution has computational advantages which are clarified later in this

section.

Description for Figure 4.1

Figure presenting a density kernel plot of the direct estimates of unemployment incidences (N = 20,122 and bandwidth = 0.002937). Density from 0 to 20 is on the y-axis and unemployment estimates from 0 to 0.35 are on the x-axis. The distribution is skewed with a right tail and a peak reached for an unemployment estimate of about 0.025.

The

model parameters of interest can be divided into three groups:

- the matrix of small area parameters:

- the vector of the measurement parameters:

- the set of latent parameters:

To

complete the Bayesian formulation of the proposed model, it is necessary to

choose priors for the model parameters. Small area parameters do not need a

specific prior because direct estimates based on observed data are available;

therefore, a set of priors is chosen for the measurement and the latent

parameters. Regarding

diffuse normal priors are assumed for the

regression coefficients. These priors are conjugate and computationally more

convenient than the usually flat priors over the real line (see Rao, 2003,

Chapter 10). In particular, we assume

with

and

is a known diagonal matrix.

Variances

are unknown and, therefore, it is necessary to

set a prior also on these parameters. The choice of the prior distribution for

the variance components is critical as in Bayesian mixed models the posterior

distributions of these parameters are known to be sensitive to this

specification. The inverse Gamma distribution is a popular choice, see e.g., You

et al. (2003) and Datta, Lahiri, Maiti and Lu (1999) among others. Gelman

(2006), Gelman, Jakulin, Pittau and Su (2008), and Polson and Scott (2012) propose

to assume a half-Cauchy distribution for the variance of the random effect.

Alternatively, a Uniform distribution can also be considered. Fabrizi

et al. (2016) conduct an exhaustive sensitivity analysis when using a

latent class model in a multivariate setting and find no significant difference

among these different alternatives. For this reason, we choose the same prior

distribution considered in You et al. (2003) and use an inverse Gamma

distribution with shape parameter

and scale parameter

then

where

are set to very small values. This choice

makes it also easier to derive the full conditional distributions for the Gibbs

sampler.

For

a system of Dirichlet priors is set on the

initial probabilities and on the transition probabilities. The Dirichlet

distribution is a conjugate prior for the multinomial distribution. This means

that if the prior distribution of the multinomial parameters is Dirichlet then

the posterior distribution belongs to the same family. The benefit of this choice

is that the posterior distribution is easy to compute and, in some sense, it is

possible to quantify how much our beliefs have changed after collecting the

data. Then, we assume

4.3 Estimation and model selection

In this work we make use of a

data augmentation Markov Chain Monte Carlo (MCMC) method (Tanner and Wong,

1987; Liu, Wong and Kong, 1994; Van Dyk and Meng, 2001) based on the Gibbs

sampler, in which the latent variables are treated as missing data (Marin et al.,

2005; Germain, 2010). There are two main reasons for this choice. First of all,

there is evidence that data augmentation has a better performance than other

methods, as the marginal updating scheme (Boys and Henderson, 2003). Moreover,

it simplifies the process of sampling from the posterior distribution. Details

on this method and the full conditionals employed in the Gibbs sampler are

given in Appendix A.1.

The choice of the number of

latent states is a crucial step in applications. In the framework of LMMs, this

requires a model selection procedure. From a Bayesian perspective, a

fundamental goal is the computation of the marginal likelihood of the data for

a given model. In this paper we use a model selection method based on the

marginal likelihood and to estimate this quantity we use the method proposed by

Carlin and Chib (1995), applied for each available model on the basis of the

output of the MCMC algorithm. Technical details are provided in Appendix A.2.

A well-known problem occurring

in Bayesian latent class and LMMs is the label switching. This implies that the

component parameters are not identifiable as they are exchangeable. In a

Bayesian context, if the prior distribution does not distinguish the component

parameters between each other, then the resulting posterior distribution will

be invariant with respect to permutations of the labels. Several solutions have

been proposed; for a general review see Jasra, Holmes and Stephens (2005). The

easiest approach is to use relabeling techniques retrospectively, by

post-processing the MCMC output (Marin et al., 2005). However, in our

case, we are interested in the prediction of the small area parameters, whose

distribution depends on the number of areas in each latent state. Therefore, we

do not use the post-processing approach and the MCMC output is permuted at

every iteration according to the ordering of the mean of the response variables

in each class.