State space time series modelling of the Dutch Labour Force Survey: Model selection and mean squared errors estimation

Section 6. Concluding remarks

There is a gradually increasing interest among NSIs in

the use of STS models for the production of monthly figures on the labour

force. In the Netherlands, such a model has been applied in the production of

official LFS figures since 2010. STS models constitute a type of small area

estimation (SAE), where sample information from preceding periods is used to

obtain more precise estimates, as well as to account for the rotating panel

design, often used in Labour Force Surveys.

Ignoring the hyperparameter uncertainty in the MSEs of

STS model-based estimates results in underestimation of the MSEs of domain

estimates. Particularly when series are short, which is often the case at NSIs,

the bias due to ignoring hyperparameter uncertainty can be substantial. Most

applications of SAE procedures in the literature are based on multilevel

models, where it is common practice to account for hyperparameter uncertainty.

The literature on STS models applied in the context of SAE is rather limited,

with most applications ignoring hyperparameter uncertainty in the MSE

estimates. Whether the bias in the obtained MSEs becomes substantial, depends

on the structure of the model and on the length of the series. The present work

describes a Monte-Carlo simulation applied to the STS model used by Statistics

Netherlands for estimating monthly unemployment. The simulation serves two

purposes. Firstly, it establishes the amount of bias in the DLFS MSEs when

hyperparameter uncertainty is ignored. In addition to that, several MSE

estimation methods available in the literature for the STS framework are

compared in this simulation, and the best approach for the Dutch LFS is

established. Secondly, simulating the distributions of the hyperparameter

estimators is useful for obtaining better insights into the dynamics of the

unobserved components in the STS model, and thus, ascertain the necessity to

model the components as time-variant. In the case of the DLFS, the simulation

shows that it might be worth considering a more restricted version of the

model, where the rotation group bias is time-invariant and the population white

noise is ignored. For both reasons, it is advisable to conduct a simulation as

described in this paper as part of the model implementation process into official

statistical production.

The comparison of the MSE estimation procedures also

sheds new light on their properties. The asymptotic approximation is not

applicable to cases where hyperparameters are close to zero because the

information matrix of the hyperparameter estimates becomes (almost) singular.

The non-parametric bootstraps, being less dependent on normality assumptions,

perform better than their parametric counterparts under both Pfeffermann and Tiller

(2005) and Rodriguez and Ruiz (2012) approaches, except in very short series.

The most important finding is that the PT bootstraps have positive biases and

consistently outperform the RR bootstraps, where the biases are generally

negative and larger (in absolute terms) than those produced by the Kalman

filter. This is contrary to the claim of Rodriguez and Ruiz (2012) about the

superiority of their method in short time series. Apparently, their findings

are purely heuristic and are based on a simple model (random walk plus noise),

while Pfeffermann and Tiller (2005) prove that their bootstrap approach

produces MSE estimates with a bias of correct order.

The variances of the PT MSE estimators are larger than

the variances of the RR MSE estimators. Differences between MSEs of the PT and

RR MSE estimators are modest to moderate (MSEs of the RR MSE estimators are 28

to 8 percent lower than those of the PT estimators, depending on the model and

the time series length). More importantly, the tendency of the RR MSE

estimators to have negative biases, sometimes exceeding those of the Kalman

filter, renders these bootstrap methods inapplicable. Hence, the

methods should be generally considered for

other survey data too, despite the fact that these methods may occasionally be

outperformed by the

methods.

For very short time series, the non-parametric

bootstraps do not seem to be an option for a model of the presented complexity.

The PT parametric bootstrap, however, corrects the negatively biased MSE up to

a small positive bias (1.4 to 4.4 percent, depending on the model). For the

present series length of 114 months, the negative MSE bias can be reduced from

about -2.4 to 1.9 percent with the non-parametric method of Pfeffermann and Tiller

(2005) in the model with a time-invariant RGB. The true Kalman filter root MSEs

are about 20 smaller than the standard errors of the GREG estimates in all the

four models applied to the DLFS data. In general, the biases in the Kalman

filter MSE estimates are relatively small in the DLFS application. Therefore,

it may be deemed sufficient to rely on these naive MSE estimates for

publication purposes.

Acknowledgements

We thank the National Statistical Office of the

Netherlands, Statistics Netherlands, for funding this research, as well as the

Associate Editor and the two anonymous reviewers for careful reading of this

manuscript and valuable comments. The views expressed in this paper are those

of the authors and do not necessarily reflect the policy of Statistics

Netherlands.

Appendices

A. Simulated densities of the hyperparameters under the four versions

of the DLFS model

This appendix presents the hyperparameter density

functions obtained from simulations where the four versions of the DLFS model

(see Table 5.1) act as the data generating process. The x-axes depict variance

hyperparameters on a log-scale, while the y-axes stand for frequencies. The x-axis

may be extended due to outliers.

Description for Figure A.1

Figure showing the hyperparameter distributions under the complete DLFS model (Model 1) for eight variance hyperparameters: and The normal

density function with the same mean and variance is superimposed on each graph.

The x-axes show

the variance hyperparameters on a log-scale and the y-axes stand for

frequencies. The x-axis may be extended due to outliers.

For the x-axis goes from -80 to -10 and the

y-axis goes from 0 to 0.75. The values are highly concentrated around the mean creating

a peak and are above the normal curve.

For the x-axis goes from -100 to -10 and

the y-axis goes from 0 to 0.075. There are extreme values at the left. The

distribution is bimodal.

For the x-axis goes from -100 to 0 and the

y-axis goes from 0 to 0.2. There are extreme values at the left. The

distribution is bimodal and very flat.

For the x-axis goes from -0.5 to 0.75 and

the y-axis goes from 0 to 3. The distribution seems close to the normal one.

For the x-axis goes from -1.0 to 0.5 and

the y-axis goes from 0 to 3. The distribution seems close to the normal one.

For the x-axis goes from -12.5 to 1.0 and

the y-axis goes from 0 to 3. The values are highly concentrated around the mean

creating a small peak.

For and the x-axes

go from -30 to 2 and the y-axes go from 0 to 3. The values are concentrated

around the mean creating a peak and are above the normal curve.

Description for Figure A.2

Figure showing the hyperparameter distributions under the complete DLFS

model (Model 2) for seven variance hyperparameters: and The normal

density function with the same mean and variance is superimposed on each graph.

The x-axes show

the variance hyperparameters on a log-scale and the y-axes stand for

frequencies. The x-axis may be extended due to outliers.

For the x-axis goes from -80 to -10 and the

y-axis goes from 0 to 0.75. The values are highly concentrated around the mean

creating a peak and are above the normal curve.

For the x-axis goes from -100 to 0 and the

y-axis goes from 0 to 0.3. The distribution is bimodal and the normal curve is

very flat.

For the x-axis goes from -50 to 2 and the

y-axis goes from 0 to 3. The values are highly concentrated around the mean

creating a high peak and are above the normal curve.

For the x-axis goes from -20 to 1 and the

y-axis goes from 0 to 3. The values are concentrated around the mean creating a

peak.

For the x-axis goes from -80 to 0 and the

y-axis goes from 0 to 2. The values are highly concentrated around the mean

creating a high peak and are above the normal curve.

For and the

x-axes go from -100 to 0 and the y-axes go from 0 to 2. The values are

concentrated around the mean creating a high peak and are above the normal

curve.

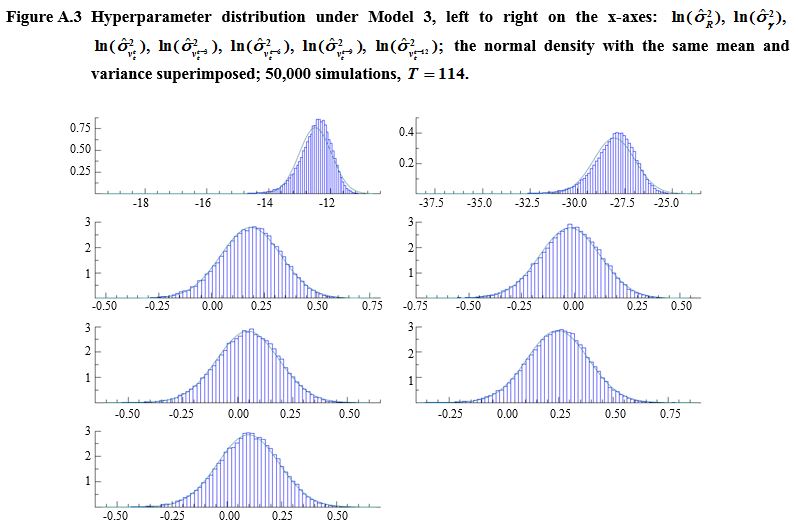

Description for Figure A.3

Figure showing the hyperparameter distributions under the complete DLFS

model (Model 3) for seven variance hyperparameters: and The normal

density function with the same mean and variance is superimposed on each graph.

The x-axes show

the variance hyperparameters on a log-scale and the y-axes stand for

frequencies.

For the x-axis goes from -18 to -10 and the

y-axis goes from 0 to 0.75. The values are concentrated around the mean and

asymmetric but close the normal curve.

For the x-axis goes from -37.5 to -25 and

the y-axis goes from 0 to 0.3. The values are concentrated around the mean and

asymmetric but close the normal curve.

For and the x-axes go from -0.50 to 0.50 and

the y-axes go from 0 to 3. The values are very close to the normal curve.

For the x-axes go from -0.25 to 0.75 and

the y-axes go from 0 to 3. The values are very close to the normal curve.

Description for Figure A.4

Figure showing the hyperparameter distributions under the complete DLFS

model (Model 4) for six variance hyperparameters: and The normal

density function with the same mean and variance is superimposed on each graph.

The x-axes show

the variance hyperparameters on a log-scale and the y-axes stand for

frequencies.

For the x-axis goes from -17 to -11 and the

y-axis goes from 0 to 0.75. The values are concentrated around the mean and

asymmetric but close the normal curve.

For and the x-axes go from -0.25 to 0.75 and

the y-axes go from 0 to 3. The values are very close to the normal curve.

For and the x-axes go from -0.50 to 0.50 and

the y-axes go from 0 to 3. The values are very close to the normal curve.

B. Predictive performance of the four DLFS models

Table B.1

Root mean square deviations of GREG estimates of the numbers of unemployed from their one-step-ahead predictions, per wave

Table summary

This table displays the results of Root mean square deviations of GREG estimates of the numbers of unemployed from their one-step-ahead predictions. The information is grouped by W (appearing as row headers), Model 1, Model 2, Model 3 and Model 4 (appearing as column headers).

| W |

Model 1 |

Model 2 |

Model 3 |

Model 4 |

|

|

|

|

|

|

|

|

|

|

|

|

| 1 |

34,370 |

33,582 |

34,641 |

34,370 |

33,582 |

34,641 |

34,518 |

33,754 |

34,881 |

34,525 |

33,757 |

34,885 |

| 2 |

30,130 |

29,770 |

29,410 |

30,130 |

29,770 |

29,410 |

30,138 |

29,780 |

29,418 |

30,144 |

29,779 |

29,409 |

| 3 |

35,792 |

32,631 |

34,654 |

35,792 |

32,631 |

34,654 |

35,714 |

32,535 |

34,499 |

35,716 |

32,532 |

34,499 |

| 4 |

39,647 |

38,556 |

36,797 |

39,647 |

38,556 |

36,797 |

39,753 |

38,640 |

36,891 |

39,743 |

38,633 |

36,889 |

| 5 |

38,271 |

37,622 |

36,341 |

38,271 |

37,622 |

36,341 |

38,183 |

37,528 |

36,225 |

38,177 |

37,523 |

36,226 |

References

Bailar, B. (1975). The

effects of rotation group bias on estimates from panel surveys. Journal of

the American Statistical Association, 70, 23-30.

Bartlett, M.S. (1946). On

the theoretical specification and sampling properties of autocorrelated

time-series. Supplement to the Journal of the Royal Statistical Society, 8, 27-41.

Binder, D.A., and Dick,

J.P. (1990). A method for the analysis of seasonal ARIMA models. Survey Methodology, 16, 2, 239-253. Paper

available at http://www.statcan.gc.ca/pub/12-001-x/1990002/article/14533-eng.pdf.

Bollineni-Balabay, O., van

den Brakel, J. and Palm, F. (2016a). Multivariate state space approach to

variance reduction in series with level and variance breaks due to survey

redesigns. Journal of the Royal Statistical Society: Series A (Statistics in

Society), 179, 377-402.

Bollineni-Balabay, O., van

den Brakel, J. and Palm, F. (2016b). State space time series modelling of the Dutch Labour

Force Survey: Model selection and MSE estimation, - Extended version. Discussion

paper, Statistics Netherlands, Heerlen. https://www.cbs.nl/en-gb/background/2016/41/state-space-time-series.

Cochran, W. (1977). Sampling

Techniques. New York: John Wiley & Sons, Inc.

Doornik, J. (2007). An

Object-Oriented Matrix Programming Language Ox 5. Timberlake Consultants

Press, London.

Durbin, J., and Koopman,

S.J. (2002). A simple and efficient simulation smoother for state space time

series analysis. Biometrika, 89, 603-615.

Durbin, J., and Koopman,

S.J. (2012). Time Series Analysis by State Space Methods. Number 38.

Oxford University Press.

EUROSTAT (2015). Task

force on monthly unemployment - revised report. Working group labour market

statistics.

Hamilton, J. (1986). A standard

error for the estimated state vector of a state-space model. Journal of

Econometrics, 33, 387-397.

Harvey, A. (1989). Forecasting,

Structural Time Series Models and the Kalman Filter. Cambridge University

Press, Cambridge.

Koopman, S.J. (1997). Exact

initial kalman filtering and smoothing for nonstationary time series models. Journal

of the American Statistical Association, 92, 1630-1638.

Koopman, S.J., Shephard,

N. and Doornik, J. (2008). SsfPack 3.0: Statistical Algorithms for Models in

State Space Form. Timberlake Consultants Press, London.

Krieg, S., and van den

Brakel, J. (2012). Estimation of the monthly unemployment rate for six domains

through structural time series modelling with cointegrated trends. Computational

Statistics & Data Analysis, 56, 2918-2933.

Lemaître, G., and Dufour,

J. (1987). An integrated method for weighting persons and

families. Survey Methodology, 13, 2, 199-207. Paper available at

http://www.statcan.gc.ca/pub/12-001-x/1987002/article/14607-eng.pdf.

ONS (2015). A state space model for LFS estimates: Agreeing the

target and dealing with wave specific bias. Report of the 29th meeting of the Government Statistical

Service Methodology Advisory Committee. http://www.ons.gov.uk/ons/guide-method/method-quality/advisory-committee/previous-meeting-papers-and-minutes/mac-29-papers.pdf.

Pfeffermann, D. (1991). Estimation

and seasonal adjustment of population means using data from repeated surveys. Journal

of Business and Economic Statistics, 9, 163-175.

Pfeffermann, D. (2013). New

important developments in small area estimation. Statistical Science, 28, 40-68.

Pfeffermann, D., and Rubin-Bleuer,

S. (1993). Robust joint modelling of labour force series of small

areas. Survey Methodology, 19, 2, 149-163. Paper available

at http://www.statcan.gc.ca/pub/12-001-x/1993002/article/14458-eng.pdf.

Pfeffermann, D., and Tiller,

R. (2005). Bootstrap approximation to prediction MSE for state-space models

with estimated parameters. Journal of Time Series Analysis, 26, 893-916.

Pfeffermann, D., Feder,

M. and Signorelli, D. (1998). Estimation of autocorrelations of survey errors

with application to trend estimation in small areas. Journal of Business and

Economic Statistics, 16, 339-348.

Rao, J.N.K., and Molina,

I. (2015). Small Area Estimation. New York: John Wiley & Sons, Inc.

Rodriguez, A., and Ruiz,

E. (2012). Bootstrap prediction mean squared errors of unobserved states based

on the Kalman filter with estimated parameters. Computational Statistics and

Data Analysis, 56, 62-74.

Särndal, C.-E., Swensson,

B. and Wretman, J. (1992). Model Assisted Survey Sampling. Springer.

Tiller, R. (1992). Time

series modelling of sample survey data from the US current population survey. Journal

of Official Statistics, 8, 149-166.

van den Brakel, J., and

Krieg, S. (2009). Estimation of the monthly unemployment rate through

structural time series modelling in a rotating panel design. Survey Methodology, 35, 2, 177-190. Paper available at

http://www.statcan.gc.ca/pub/12-001-x/2009002/article/11040-eng.pdf.

van den Brakel, J., and

Krieg, S. (2015). Dealing with small sample sizes, rotation group bias

and discontinuities in a rotating panel design. Survey Methodology, 41, 2, 267-296. Paper available at

http://www.statcan.gc.ca/pub/12-001-x/2015002/article/14231-eng.pdf.

Zhang, M., and Honchar,

O. (2016). Predicting survey estimates by state space models using multiple

data sources. Paper for the Australian

Bureau of Statistics’ Methodology Advisory Committee.