Insights on Canadian Society

Homeownership, mortgage debt and types of mortgage among Canadian families

Archived Content

Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject to the Government of Canada Web Standards and has not been altered or updated since it was archived. Please "contact us" to request a format other than those available.

by Sharanjit Uppal

Start of text box

A dream of many Canadians is to someday own their own home and most take on debt for that reason. This study uses data from the Survey of Financial Security to examine changes in homeownership rates and factors associated with homeownership, the proportion of families who had paid off the mortgage on their principal residence, and the amount of mortgage debt owed by families who had a mortgage. The study also provides information on the types of mortgage rates on the principal residence (fixed rate, variable rate or a combination of both).

- In 2016, 63% of Canadian families owned their homes, up from 60% in 1999. Almost all of this increase was because of population aging, given that families in older age groups are more likely to own their homes.

- In 2016, 43% of Canadian homeowners had paid off the mortgage on their principal residence, down from 46% in 1999. Without population aging, this proportion would have declined to 36% in 2016.

- From 1999 to 2016, mortgage debt represented two-thirds of the overall increase in debt for Canadian families, while consumer debt made up the remainder. In recent years (2012 to 2016), mortgage debt was responsible for 100% of the increase in total debt.

- From 1999 to 2016, the median amount of mortgage debt among Canadian families with a mortgage almost doubled, from $91,900 to $180,000 in 2016 constant dollars. The amount of mortgage debt increased in nearly all demographic groups and in almost all regions of Canada.

- In 2016, almost three-quarters (74%) of Canadian families with a mortgage had a fixed mortgage rate, 21% had a variable mortgage rate, and 5% had a combination of a fixed and variable mortgage rate.

End of text box

Introduction

In recent years, a great deal of research has focused on the levels of debt that families carry and the increase in debt.Note Most of the increase in total debt is from mortgage debt, and the increase in mortgage debt can be attributed to two factors. The first is the rapid increase in housing prices. According to the monthly Home Price Index published by the Canadian Real Estate Association (CREA), housing prices rose by 109% (in nominal terms) from January 2005 to December 2016.Note In comparison, during the same period, the Consumer Price Index (CPI) showed an overall price increase of 22%.Note The second factor is mortgage interest rates, which have been at historically low levels for most of the last decade, making borrowing costs low and acting as an incentive for families to take on new or bigger mortgages.Note

There is a possibility that these historically low mortgage rates would increase as the Bank of Canada normalizes monetary policy. Because mortgage debt is high, there are concerns that certain households may not be able to withstand interest rate hikes. The short-term effect of an interest rate hike depends, in part, on the type of mortgage rate the debt carries. If the mortgage rate is fixed, then a rate hike will not have any immediate effect on mortgage payments or on the outstanding amount to be paid until the end of the term. However, if the rate is variable, an increase in the rate will have either of the following consequences, depending on the type of agreement: (1) it will lead to an immediate increase in payment or an increase in payment after the interest rate reaches a certain threshold; or (2) it will not change the payment, but decrease the repayment of principal and increase the accrued interest. Even for families with a fixed mortgage rate, a higher interest rate may have an impact for those who are not prepared for the possibility of facing higher interest rates at the end of their term. In view of the above, a study on homeownership, current outstanding mortgage debt and types of mortgage rates is important.

While examples of Canadian studies focusing on homeownership and mortgage debt can be found in the literature,Note little is available on the types of mortgage rates across regions or family types. For the first time, the 2016 Survey of Financial Security (SFS) asked about the type of mortgage rate that a family took on their principal residence mortgage debt (see the Data sources, methods and definitions section).

The first part of the article will look at homeownership rates across family characteristics. It will then look at the characteristics of families who had paid off their mortgage, and the amount of mortgage outstanding among families who had not paid off their mortgage debt. In the second part, family characteristics associated with various types of mortgage rates will be examined. Where possible, comparisons will be drawn over time.

In 2016, more than 6 in 10 families owned their principal residence

In 2016, 63% of Canadian families owned their principal residence, up slightly from 60% in 1999 (Table 1).Note Note Almost all of this increase is attributable to a demographic shift—the Canadian population became older, and older age groups are more likely to own their homes.Note

| 1999 | 2016 | |

|---|---|---|

| percent | ||

| All | 60.4 | 62.8Note * |

| Age of major income earner | ||

| 19 to 24 | 12.5 | 10.3 |

| 25 to 34 | 43.4 | 44.4 |

| 35 to 44 | 62.9 | 64.6 |

| 45 to 54 | 72.7 | 70.7 |

| 55 to 64 | 74.7 | 78.3 |

| 65 and over | 67.9 | 68.2 |

| Highest level of education of major income earner | ||

| Less than high school | 57.1 | 51.8Note * |

| High school diploma | 57.1 | 55.6 |

| Non-university postsecondary certificate or diploma | 62.3 | 68.7Note * |

| University degree or certificate | 66.3 | 67.7 |

| Family structure | ||

| Unattached individual | 32.5 | 38.6Note * |

| Couple, no children | 75.1 | 78.0 |

| Couple with children | 78.2 | 78.0 |

| Lone-parent family | 39.9 | 44.8 |

| Other family types | 77.5 | 78.2 |

| Immigrant status of major income earner | ||

| Recent immigrant | 17.4 | 38.7Note * |

| Established immigrant | 64.2 | 69.7Note * |

| Canadian-born individual | 60.8 | 61.9 |

| Labour force status of major income earner | ||

| Paid employee | 62.2 | 64.4 |

| Self-employed | 74.5 | 75.5 |

| Not in labour force | 53.3 | 56.6 |

| Family income quintile | ||

| Bottom quintile | 25.5 | 24.5 |

| Second quintile | 53.1 | 53.0 |

| Third quintile | 67.0 | 69.0 |

| Fourth quintile | 75.0 | 79.4Note * |

| Top quintile | 81.7 | 88.2Note * |

| Family budget | ||

| Yes | 57.5 | 61.7Note * |

| No | 62.9 | 63.8 |

| Amount of credit card balances paid off every month | ||

| Minimum or less than minimum | Note ..: not available for a specific reference period | 51.2 |

| More than minimum but less than full amount | Note ..: not available for a specific reference period | 62.6 |

| Full amount | Note ..: not available for a specific reference period | 73.6 |

| Do not have credit card | Note ..: not available for a specific reference period | 20.3 |

| Someone in the family borrowed money through a payday loan in the past three years | ||

| Yes | Note ..: not available for a specific reference period | 27.8 |

| No | Note ..: not available for a specific reference period | 64.0 |

| Someone in the family ever declared bankruptcy or made a formal proposal or informal financial arrangements to creditors | ||

| Yes | Note ..: not available for a specific reference period | 44.1 |

| No | Note ..: not available for a specific reference period | 64.8 |

| Region | ||

| Newfoundland and Labrador | 74.6 | 74.4 |

| Prince Edward Island | 67.9 | 66.7 |

| Nova Scotia | 66.5 | 63.9 |

| New Brunswick | 69.4 | 70.8 |

| Québec | 58.0 | 57.0 |

| Montréal | 44.8 | 50.5 |

| Quebec excluding the CMAs of Québec and Montréal | 66.0 | 63.9 |

| Ottawa | 49.0 | 61.2 |

| Toronto | 54.4 | 58.7 |

| Ontario excluding the CMAs of Ottawa and Toronto | 67.5 | 70.1 |

| Winnipeg | 61.5 | 63.4 |

| Manitoba excluding the CMA of Winnipeg | 70.2 | 77.8 |

| Regina | 68.6 | 62.9 |

| Saskatoon | 59.5 | 61.4 |

| Saskatchewan excluding the CMAs of Regina and Saskatoon | 73.6 | 74.1 |

| Calgary | 64.3 | 67.5 |

| Edmonton | 65.2 | 60.7 |

| Alberta excluding the CMAs of Calgary and Edmonton | 72.2 | 69.4 |

| Vancouver | 52.3 | 55.8 |

| British Columbia excluding the CMA of Vancouver | 62.0 | 69.1 |

.. not available for a specific reference period

|

||

Recent immigrants (those who immigrated during the five years preceding the survey) had the largest increase in homeownership.Note The homeownership rate for this group increased from 17% in 1999 to 39% in 2016. Established immigrants (those who immigrated more than five years before the survey) also had a notable increase (6 percentage points).

The homeownership rate for families whose major income earner had a non-university postsecondary certificate increased by 6 percentage points. In contrast, the rate for the lowest educational category (i.e., those who did not complete high school) decreased by 5 percentage points. Families in the top two income quintiles also experienced a significant increase in homeownership (4 percentage points and 7 percentage points, respectively), as well as unattached individualsNote (6 percentage points) and those who maintained a family budget (4 percentage points). Regionally, there were no statistically significant changes in homeownership.

There is a clear association between homeownership and age, largely because homeownership is a life cycle phenomenon. Younger individuals aged less than 35 are less likely to own homes, because many are still in school and others have recently graduated and are in the process of saving money for a down payment. The homeownership rate is higher among middle aged individuals (i.e., those aged 45 to 64); in 2016, homeownership was 71% among families whose major income earner was aged 45 to 54 and 78% among those aged 55 to 64.

Homeownership rates were higher among families whose major income earner had a level of education above a high school diploma (largely because higher educated people have higher incomes). Couple families were more likely to own homes, compared with lone parents and unattached individuals. Families whose major income earner was self-employed were more likely to own their homes than families of paid employees and people who were not in the labour force. Despite the large increase in homeownership rates of recent immigrants, they remained less likely to own their homes than established immigrants and Canadian-born individuals. As expected, families in the top income quintile were more likely to own their homes than those in the bottom quintile.

Certain financial behavioural factors can also be associated with homeownership. In the 2016 SFS, questions related to financial behaviour included whether or not the family had a household budget, had borrowed money through payday loans in the past three years, or had anyone in the family who had ever declared bankruptcy or who made a formal proposal or informal financial arrangements to creditors. Information on payments on credit card balances was also collected.Note Families who paid off their monthly credit card balances in full were more likely to own their homes. However, financial instability (whether measured as having declared bankruptcy or made formal or informal arrangements, or as having borrowed through a payday loan) was negatively associated with homeownership. Declaring bankruptcy or making formal proposals to creditors would make it more difficult to obtain credit from a financial institution, while having borrowed from a payday loan reflects a low level of financial resources and therefore a reduced ability to make a down payment.

There were some regional variations in homeownership. Families in Montréal (51%) were the least likely to be homeowners, whereas families in Newfoundland and Labrador (74%) and areas in Manitoba other than Winnipeg (78%) were the most likely.

Because various personal characteristics are expected to be correlated with each other, a logistic regression was estimated to calculate predicted probabilities of homeownership. Controlling for various characteristics changed some of the conclusions based on descriptive statistics. The predicted probability of owning a home was now higher among those aged 65 and over (0.75), compared with 0.63 for those aged 45 to 54 and 0.46 for those aged 25 to 34 (Table 2). Seniors are more likely to have lower levels of education, be unattached and belong to the lower income quintiles—characteristics that are associated with lower homeownership rates.

| Model 1 | Model 2 | |

|---|---|---|

| predicted probability | ||

| Age of major income earner | ||

| 19 to 24 | 0.34Note * | 0.32Note * |

| 25 to 34 (ref.) | 0.46 | 0.47 |

| 35 to 44 | 0.55Note * | 0.57Note * |

| 45 to 54 | 0.63Note * | 0.65Note * |

| 55 to 64 | 0.74Note * | 0.74Note * |

| 65 and over | 0.75Note * | 0.73Note * |

| Highest level of education of major income earner | ||

| Less than high school (ref.) | 0.59 | 0.62 |

| High school diploma | 0.60 | 0.61 |

| Non-university postsecondary certificate or diploma | 0.66Note * | 0.66Note * |

| University degree or certificate | 0.64Note * | 0.61 |

| Family structure | ||

| Unattached individual (ref.) | 0.47 | 0.48 |

| Couple, no children | 0.67Note * | 0.66Note * |

| Couple with children | 0.79Note * | 0.77Note * |

| Lone-parent family | 0.64Note * | 0.66Note * |

| Other family types | 0.72Note * | 0.72Note * |

| Immigrant status of major income earner | ||

| Recent immigrant | 0.49Note * | 0.47Note * |

| Established immigrant | 0.66Note * | 0.65 |

| Canadian-born individual (ref.) | 0.62 | 0.63 |

| Labour force status of major income earner | ||

| Paid employee (ref.) | 0.62 | 0.62 |

| Self-employed | 0.70Note * | 0.69Note * |

| Not in labour force | 0.62 | 0.62 |

| Family income quintile | ||

| Bottom quintile (ref.) | 0.38 | 0.43 |

| Second quintile | 0.52Note * | 0.54Note * |

| Third quintile | 0.66Note * | 0.65Note * |

| Fourth quintile | 0.75Note * | 0.73Note * |

| Top quintile | 0.83Note * | 0.80Note * |

| Family budget | ||

| Yes (ref.) | Note ...: not applicable | 0.62 |

| No | Note ...: not applicable | 0.63 |

| Amount of credit card balances paid off every month | ||

| Minimum or less than minimum | Note ...: not applicable | 0.61Note * |

| More than minimum but less than full amount | Note ...: not applicable | 0.62Note * |

| Full amount (ref.) | Note ...: not applicable | 0.67 |

| Do not have credit card | Note ...: not applicable | 0.45Note * |

| Someone in the family borrowed money through a payday loan in the past three years | ||

| Yes (ref.) | Note ...: not applicable | 0.45 |

| No | Note ...: not applicable | 0.63Note * |

| Someone in the family ever declared bankruptcy or made a formal proposal or informal financial arrangements to creditors | ||

| Yes (ref.) | Note ...: not applicable | 0.52 |

| No | Note ...: not applicable | 0.64Note * |

| Region | ||

| Newfoundland and Labrador | 0.73Note * | 0.74Note * |

| Prince Edward Island | 0.67Note * | 0.69Note * |

| Nova Scotia | 0.66Note * | 0.68Note * |

| New Brunswick | 0.73Note * | 0.73Note * |

| Québec | 0.58 | 0.55 |

| Montréal | 0.54Note * | 0.54Note * |

| Quebec excluding the CMAs of Québec and Montréal | 0.66Note * | 0.66Note * |

| Ottawa | 0.56 | 0.56 |

| Toronto (ref.) | 0.60 | 0.59 |

| Ontario excluding the CMAs of Ottawa and Toronto | 0.66Note * | 0.68Note * |

| Winnipeg | 0.66Note * | 0.66Note * |

| Manitoba excluding the CMA of Winnipeg | 0.72Note * | 0.71Note * |

| Regina | 0.62 | 0.62 |

| Saskatoon | 0.65 | 0.64 |

| Saskatchewan excluding the CMAs of Regina and Saskatoon | 0.71Note * | 0.72Note * |

| Calgary | 0.64 | 0.63Note * |

| Edmonton | 0.58 | 0.60 |

| Alberta excluding the CMAs of Calgary and Edmonton | 0.67Note * | 0.68Note * |

| Vancouver | 0.58 | 0.57 |

| British Columbia excluding the CMA of Vancouver | 0.68Note * | 0.68Note * |

... not applicable

|

||

When financial behavioural characteristics are included in the model, the result for university education becomes statistically insignificant. This shows that university education has a positive association with homeownership through its effect on financial behaviour. In other words, university education has a positive association with positive or prudent financial behaviours, which in turn have a positive association with homeownership.

The probabilities of owning a home were relatively higher among families living in the Atlantic provinces (from 0.66 to 0.73). Additionally, areas outside large census metropolitan areas (CMAs) in the rest of Canada had higher ownership rates. Areas outside CMAs usually have higher homeownership for two reasons: relatively less expensive house prices and lower availability of rental units. Finally, the probability of owning a home in Montréal (0.54) was the lowest of all regions. The low homeownership in Montréal (and in Quebec in general) can be attributed to the favourable shelter costs of renting compared with owning.Note

In 2016, more than 4 in 10 families had paid off their mortgage

In 2016, 43% of homeowners did not have any mortgage debt on their principal residence; in other words, they had paid off their house. However, this proportion varied across characteristics, particularly age. This is expected, since mortgage debt typically involves large amounts that are contracted at a relatively young age to pay for a house and then slowly repaid over time.

Therefore, it is not surprising that older people are more likely to have paid off their mortgage. In 2016, over 8 in 10 families whose major income earner was aged 65 or over had paid off their mortgage, compared with less than 1 in 10 of those whose major income earner was aged 25 to 34. Other characteristics, however, are also associated with having no mortgage debt. These characteristics can be examined in a regression model controlling for age, with results expressed in predicted probabilities (Table 3).

| Model 1 | Model 2 | |

|---|---|---|

| predicted probability | ||

| Age of major income earner | ||

| 19 to 24 | Note F: too unreliable to be published | Note F: too unreliable to be published |

| 25 to 34 (ref.) | 0.13 | 0.14 |

| 35 to 44 | 0.18Note * | 0.19Note * |

| 45 to 54 | 0.37Note * | 0.38Note * |

| 55 to 64 | 0.51Note * | 0.51Note * |

| 65 and over | 0.71Note * | 0.67Note * |

| Highest level of education of major income earner | ||

| Less than high school (ref.) | 0.44 | 0.45 |

| High school diploma | 0.42 | 0.43 |

| Non-university postsecondary certificate or diploma | 0.41 | 0.42 |

| University degree or certificate | 0.44 | 0.43 |

| Family structure | ||

| Unattached individual (ref.) | 0.44 | 0.43 |

| Couple, no children | 0.46 | 0.45 |

| Couple with children | 0.35Note * | 0.36Note * |

| Lone-parent family | 0.44 | 0.44 |

| Other family types | 0.43 | 0.45 |

| Immigrant status of major income earner | ||

| Recent immigrant | 0.33Note * | 0.34Note * |

| Established immigrant | 0.39Note * | 0.39Note * |

| Canadian-born individual (ref.) | 0.44 | 0.44 |

| Labour force status of major income earner | ||

| Paid employee (ref.) | 0.37 | 0.39 |

| Self-employed | 0.40 | 0.40 |

| Not in labour force | 0.54Note * | 0.52Note * |

| Family income quintile | ||

| Bottom quintile (ref.) | 0.43 | 0.44 |

| Second quintile | 0.41 | 0.42 |

| Third quintile | 0.40 | 0.41 |

| Fourth quintile | 0.43 | 0.43 |

| Top quintile | 0.46 | 0.44 |

| Family budget | ||

| Yes (ref.) | Note ...: not applicable | 0.40 |

| No | Note ...: not applicable | 0.44Note * |

| Amount of credit card balances paid off every month | ||

| Minimum or less than minimum | Note ...: not applicable | 0.30Note * |

| More than minimum but less than full amount | Note ...: not applicable | 0.28Note * |

| Full amount (ref.) | Note ...: not applicable | 0.49 |

| Do not have credit card | Note ...: not applicable | 0.45 |

| Someone in the family borrowed money through a payday loan in the past three years | ||

| Yes (ref.) | Note ...: not applicable | 0.37 |

| No | Note ...: not applicable | 0.43 |

| Someone in the family ever declared bankruptcy or made a formal proposal or informal financial arrangements to creditors | ||

| Yes (ref.) | Note ...: not applicable | 0.34 |

| No | Note ...: not applicable | 0.43Note * |

| Region | ||

| Newfoundland and Labrador | 0.48 | 0.51Note * |

| Prince Edward Island | 0.41 | 0.41 |

| Nova Scotia | 0.44 | 0.47 |

| New Brunswick | 0.43 | 0.45 |

| Québec | 0.39 | 0.37 |

| Montréal | 0.39 | 0.38Note * |

| Quebec excluding the CMAs of Québec and Montréal | 0.42 | 0.43 |

| Ottawa | 0.38 | 0.38 |

| Toronto (ref.) | 0.43 | 0.42 |

| Ontario excluding the CMAs of Ottawa and Toronto | 0.45 | 0.45 |

| Winnipeg | 0.43 | 0.42 |

| Manitoba excluding the CMA of Winnipeg | 0.45 | 0.46 |

| Regina | 0.43 | 0.44 |

| Saskatoon | 0.45 | 0.43 |

| Saskatchewan excluding the CMAs of Regina and Saskatoon | 0.51Note * | 0.51Note * |

| Calgary | 0.43 | 0.43 |

| Edmonton | 0.40 | 0.41 |

| Alberta excluding the CMAs of Calgary and Edmonton | 0.46 | 0.47Note * |

| Vancouver | 0.43 | 0.41 |

| British Columbia excluding the CMA of Vancouver | 0.38Note * | 0.38Note * |

|

... not applicable F too unreliable to be published

|

||

Couples with children were less likely to have paid off their mortgage (0.35), compared with unattached individuals (0.44).Note This is likely because they have more financial responsibilities given the presence of children. Couples with children also tend to have larger houses, which are more costly. Conversely, individuals who were not in the labour force (0.54) were more likely to have paid off their mortgage than those who were in the labour force. This result is not necessarily a surprise, since the group of people outside the labour force includes retirees, and people often continue to work until their debts are paid in full.Note

Recent and established immigrants had a lower probability of having paid off their mortgage (0.34 and 0.39, respectively) than Canadian-born individuals (0.44). The results associated with financial behaviour variables show that the probability of having paid off the mortgage was higher among those who paid off credit card balances in full and those who had never declared bankruptcy.

The results did not show much variation across regions, since most probabilities were not statistically different from the reference region (Toronto). However, homeowners in Newfoundland and Labrador and in Saskatchewan excluding Regina and Saskatoon were more likely to have paid off their mortgage, compared with homeowners in Toronto. In contrast, homeowners in Montréal and British Columbia excluding Vancouver were less likely to have paid off their mortgage.

It is also important to examine changes over time. From 1999 to 2016, the proportion of families who had paid off their mortgage decreased from 46% to 43%. This decline occurred against a backdrop of population aging, which would be associated with a higher rate because older people are more likely to have paid off their mortgage. Population aging slowed down the decline in the proportion of homeowners who had paid off their mortgage. If the age structure had remained the same as in 1999, the decline in the proportion of families who had paid off their mortgage debt would have been significantly larger—falling from 46% in 1999 to 36% in 2016.

From 1999 to 2016, almost all groups experienced a decline in the proportion of homeowners who had paid off their mortgage. The magnitude, however, varied across family characteristics. The decline was relatively large for families whose major income earner was aged 35 to 64—an 11 to 12 percentage point decrease. The younger age group, those aged 25 to 34, saw a 4 percentage point decrease (Table 4).

| 1999 | 2016 | |

|---|---|---|

| percent | ||

| All | 46.3 | 42.7Note * |

| Age of major income earner | ||

| 19 to 24 | Note F: too unreliable to be published | Note F: too unreliable to be published |

| 25 to 34 | 13.4 | 9.4Note * |

| 35 to 44 | 23.2 | 11.6Note * |

| 45 to 54 | 41.3 | 30.4Note * |

| 55 to 64 | 66.1 | 54.2Note * |

| 65 and over | 90.1 | 82.1Note * |

| Highest level of education of major income earner | ||

| Less than high school | 65.3 | 66.7 |

| High school diploma | 41.0 | 44.7 |

| Non-university postsecondary certificate or diploma | 38.7 | 37.8 |

| University degree or certificate | 39.5 | 38.1 |

| Family structure | ||

| Unattached individual | 59.8 | 54.6 |

| Couple, no children | 62.9 | 58.3Note * |

| Couple with children | 25.8 | 14.2Note * |

| Lone-parent family | 28.3 | 22.6 |

| Other family types | 57.0 | 42.1Note * |

| Immigrant status of major income earner | ||

| Recent immigrant | 23.1 | 19.3 |

| Established immigrant | 47.9 | 39.5Note * |

| Canadian-born individual | 46.1 | 44.4 |

| Labour force status of major income earner | ||

| Paid employee | 28.9 | 26.4Note * |

| Self-employed | 41.6 | 39.1 |

| Not in labour force | 82.6 | 76.2Note * |

| Family income quintile | ||

| Bottom quintile | 59.6 | 54.4Note * |

| Second quintile | 49.2 | 43.5Note * |

| Third quintile | 42.6 | 36.3Note * |

| Fourth quintile | 37.7 | 37.5 |

| Top quintile | 42.4 | 41.8 |

| Family budget | ||

| Yes | 36.9 | 38.1 |

| No | 53.4 | 46.5Note * |

| Amount of credit card balances paid off every month | ||

| Minimum or less than minimum | Note ..: not available for a specific reference period | 18.3 |

| More than minimum but less than full amount | Note ..: not available for a specific reference period | 20.1 |

| Full amount | Note ..: not available for a specific reference period | 52.2 |

| Do not have credit card | Note ..: not available for a specific reference period | 60.2 |

| Someone in the family borrowed money through a payday loan in the past three years | ||

| Yes | Note ..: not available for a specific reference period | 23.0 |

| No | Note ..: not available for a specific reference period | 43.0 |

| Someone in the family ever declared bankruptcy or made a formal proposal or informal financial arrangements to creditors | ||

| Yes | Note ..: not available for a specific reference period | 25.0 |

| No | Note ..: not available for a specific reference period | 44.0 |

| Region | ||

| Newfoundland and Labrador | 66.8 | 52.8Note * |

| Prince Edward Island | 52.6 | 41.7 |

| Nova Scotia | 52.5 | 51.1 |

| New Brunswick | 54.9 | 46.6 |

| Québec | 39.7 | 36.8 |

| Montréal | 43.2 | 36.5 |

| Quebec excluding the CMAs of Québec and Montréal | 50.5 | 48.6 |

| Ottawa | 37.3 | 36.9 |

| Toronto | 43.9 | 36.7 |

| Ontario excluding the CMAs of Ottawa and Toronto | 44.9 | 47.7 |

| Winnipeg | 48.1 | 37.4Note * |

| Manitoba excluding the CMA of Winnipeg | 58.3 | 45.5 |

| Regina | 47.1 | 43.4 |

| Saskatoon | 46.4 | 47.2 |

| Saskatchewan excluding the CMAs of Regina and Saskatoon | 66.5 | 53.5Note * |

| Calgary | 35.6 | 36.1 |

| Edmonton | 44.5 | 34.5Note * |

| Alberta excluding the CMAs of Calgary and Edmonton | 46.8 | 45.9 |

| Vancouver | 40.5 | 40.0 |

| British Columbia excluding the CMA of Vancouver | 45.0 | 45.8 |

|

.. not available for a specific reference period F too unreliable to be published

|

||

The decline in the proportion of homeowners who had paid off the mortgage on their principal residence was around 5 to 6 percentage points for the bottom three income quintiles. This proportion did not change for the upper two income quintiles. Other groups that saw a significant decrease in this proportion included couples with children (12 percentage points) and without children (5 percentage points), other family types (15 percentage points), established immigrants (8 percentage points), homeowners not in the labour force (6 percentage points), and homeowners who did not maintain a family budget (7 percentage points). Regionally, significant declines were seen in Newfoundland and Labrador (14 percentage points), Winnipeg (11 percentage points), Edmonton (10 percentage points) and areas of Saskatchewan other than Regina and Saskatoon (13 percentage points).

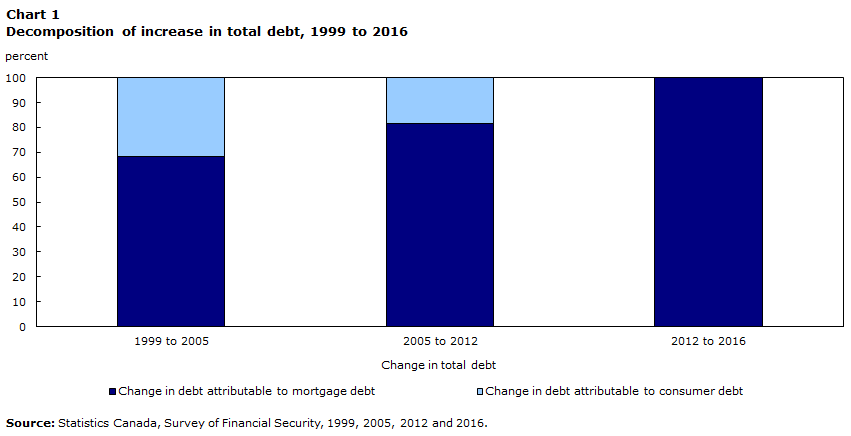

From 2012 to 2016, the increase in total debt was entirely due to mortgage debt

Mortgage debt constitutes the majority of a family’s total debt. In 2016, it accounted for 81% of the total debt of Canadian families, up from 77% in 1999.Note From 1999 to 2016, the average total family debt more than doubled, from $75,300 to $162,400 in 2016 dollars.Note During the same period, average mortgage debt increased from $58,200 to $131,100, an increase of 125%. Consumer debt also rose, but at a slower pace (from $17,000 to $31,300).Note Therefore, most of the increase in total debt resulted from the rise in mortgage debt.

In fact, mortgage debt contributed to 84% of the increase in total debt from 1999 to 2016. Interestingly, the contribution of mortgage debt to the increase in total debt has been more significant in recent years. From 1999 to 2005, 68% of the increase in total debt resulted from the increase in mortgage debt (Chart 1), rising to 82% from 2005 to 2012, then to 100% from 2012 to 2016. The average consumer debt remained unchanged between 2012 and 2016 (at $31,300).

Data table for Chart 1

| Years | Change in debt attributable to mortgage debt | Change in debt attributable to consumer debt |

|---|---|---|

| percent | ||

| 1999 to 2005 | 68.4 | 31.6 |

| 2005 to 2012 | 81.6 | 18.4 |

| 2012 to 2016 | 99.9 | 0.1 |

| Source: Statistics Canada, Survey of Financial Security, 1999, 2005, 2012 and 2016. | ||

Mortgage debt on the principal residence doubled from 1999 to 2016

Among homeowners who had a mortgage, the median mortgage debt was $180,000 in 2016 (Table 5).Note As expected, the level of mortgage debt decreases with age. The median mortgage debt of families whose major income earner was aged 25 to 44 was twice as much as those whose major income earner was aged 65 and over. Higher mortgage debt in the middle age group is consistent with the life-cycle theory of asset accumulation.

| 1999 | 2016 | Change, 1999 to 2016 | ||

|---|---|---|---|---|

| 2016 constant dollars | 2016 constant dollars | percent | ||

| All | 91,900 | 180,000 | 88,100 | 96Note * |

| Age of major income earner | ||||

| 19 to 24 | 87,100 | 160,000 | 72,900 | 84 |

| 25 to 34 | 116,100 | 213,000 | 96,900 | 83Note * |

| 35 to 44 | 96,800 | 200,000 | 103,200 | 107Note * |

| 45 to 54 | 78,800 | 174,000 | 95,200 | 121Note * |

| 55 to 64 | 67,400 | 130,000 | 62,600 | 93Note * |

| 65 and over | 55,300 | 100,000 | 44,700 | 81Note * |

| Highest level of education of major income earner | ||||

| Less than high school | 67,700 | 100,000 | 32,300 | 48Note * |

| High school diploma | 89,800 | 153,600 | 63,800 | 71Note * |

| Non-university postsecondary certificate or diploma | 92,600 | 174,000 | 81,400 | 88Note * |

| University degree or certificate | 110,600 | 210,000 | 99,400 | 90Note * |

| Family structure | ||||

| Unattached individual | 80,200 | 135,000 | 54,800 | 68Note * |

| Couple, no children | 89,800 | 165,000 | 75,200 | 84Note * |

| Couple with children | 96,800 | 205,000 | 108,200 | 112Note * |

| Lone-parent family | 78,800 | 165,000 | 86,200 | 109Note * |

| Other family types | 92,600 | 170,000 | 77,400 | 84Note * |

| Immigrant status of major income earner | ||||

| Recent immigrant | 172,800 | 293,000 | 120,200 | 70Note * |

| Established immigrant | 117,500 | 230,000 | 112,500 | 96Note * |

| Canadian-born individual | 87,000 | 158,600 | 71,600 | 82Note * |

| Labour force status of major income earner | ||||

| Paid employee | 94,900 | 182,000 | 87,100 | 92Note * |

| Self-employed | 103,700 | 200,000 | 96,300 | 93Note * |

| Not in labour force | 58,100 | 110,000 | 51,900 | 89Note * |

| Family income quintile | ||||

| Bottom quintile | 69,100 | 145,000 | 75,900 | 110Note * |

| Second quintile | 79,100 | 160,000 | 80,900 | 102Note * |

| Third quintile | 96,800 | 180,000 | 83,200 | 86Note * |

| Fourth quintile | 103,700 | 175,000 | 71,300 | 69Note * |

| Top quintile | 110,800 | 228,000 | 117,200 | 106Note * |

| Family budget | ||||

| Yes | 92,600 | 180,000 | 87,400 | 94Note * |

| No | 91,200 | 174,000 | 82,800 | 91Note * |

| Amount of credit card balances paid off every month | ||||

| Minimum or less than minimum | Note ..: not available for a specific reference period | 195,000 | Note ...: not applicable | Note ...: not applicable |

| More than minimum but less than full amount | Note ..: not available for a specific reference period | 180,000 | Note ...: not applicable | Note ...: not applicable |

| Full amount | Note ..: not available for a specific reference period | 180,000 | Note ...: not applicable | Note ...: not applicable |

| Do not have credit card | Note ..: not available for a specific reference period | 112,000 | Note ...: not applicable | Note ...: not applicable |

| Someone in the family borrowed money through a payday loan in the past three years | ||||

| Yes | Note ..: not available for a specific reference period | 135,000 | Note ...: not applicable | Note ...: not applicable |

| No | Note ..: not available for a specific reference period | 180,000 | Note ...: not applicable | Note ...: not applicable |

| Someone in the family ever declared bankruptcy or made a formal proposal or informal financial arrangements to creditors | ||||

| Yes | Note ..: not available for a specific reference period | 157,500 | Note ...: not applicable | Note ...: not applicable |

| No | Note ..: not available for a specific reference period | 180,000 | Note ...: not applicable | Note ...: not applicable |

| Region | ||||

| Newfoundland and Labrador | 55,300 | 121,000 | 65,700 | 119Note * |

| Prince Edward Island | 56,700 | 80,700 | 24,000 | 42 |

| Nova Scotia | 59,400 | 101,500 | 42,100 | 71Note * |

| New Brunswick | 48,400 | 89,000 | 40,600 | 84Note * |

| Québec | 71,900 | 150,000 | 78,100 | 109Note * |

| Montréal | 89,800 | 160,000 | 70,200 | 78Note * |

| Quebec excluding the CMAs of Québec and Montréal | 55,300 | 103,000 | 47,700 | 86Note * |

| Ottawa | 126,800 | 206,000 | 79,200 | 62Note * |

| Toronto | 143,700 | 280,000 | 136,300 | 95Note * |

| Ontario excluding the CMAs of Ottawa and Toronto | 96,800 | 145,000 | 48,200 | 50Note * |

| Winnipeg | 69,100 | 170,000 | 100,900 | 146Note * |

| Manitoba excluding the CMA of Winnipeg | 55,300 | 130,000 | 74,700 | 135Note * |

| Regina | 76,000 | 220,000 | 144,000 | 189Note * |

| Saskatoon | 66,300 | 190,000 | 123,700 | 187Note * |

| Saskatchewan excluding the CMAs of Regina and Saskatoon | 49,800 | 110,000 | 60,200 | 121Note * |

| Calgary | 118,900 | 260,000 | 141,100 | 119Note * |

| Edmonton | 89,800 | 250,000 | 160,200 | 178Note * |

| Alberta excluding the CMAs of Calgary and Edmonton | 78,800 | 200,000 | 121,200 | 154Note * |

| Vancouver | 165,900 | 266,000 | 100,100 | 60Note * |

| British Columbia excluding the CMA of Vancouver | 110,600 | 178,000 | 67,400 | 61Note * |

|

.. not available for a specific reference period ... not applicable

|

||||

Families whose major income earner held a university degree had more than twice as much mortgage debt than those whose major income earner did not complete high school. University-educated individuals typically have higher incomes, which allows for better access to credit.

Mortgage debt also varied across the income distribution. The median level of mortgage debt among families in the top income quintile was $228,000, compared with $145,000 among families in the bottom quintile. Mortgage debt was higher for recent and established immigrants ($293,000 and $230,000, respectively) than for Canadian-born individuals ($158,600). Among family types, couples with children ($205,000) had the most mortgage debt, and unattached individuals ($135,000) had the least.

Homeowners who had not borrowed through a payday loan in the past three years and those who had never declared bankruptcy or made a formal proposal or informal financial arrangements to creditors had higher levels of mortgage debt, reflecting a better ability to obtain credit.

Regionally, families in Toronto ($280,000), Vancouver ($266,000), Calgary ($260,000) and Edmonton ($250,000) had the highest median levels of mortgage debt. These markets are among the most expensive in the country. Homeowners residing in New Brunswick ($89,000) and Prince Edward Island ($80,700), where housing prices are lower, had the lowest median mortgage debt.

From 1999 to 2016, mortgage debt doubled from $91,900 to $180,000 in 2016 dollars. This is not a surprise, given that housing prices almost doubled in Canada from 2005 to 2016. Mortgage debt increased significantly among all groups, but there were differences across groups. In percentage terms, among all age groups, families whose major income earner was aged 45 to 54 experienced the largest increase in mortgage debt (121%, or $95,200), followed by those whose major income earner was aged 35 to 44 (107%, or $103,200).

The median mortgage debt more than doubled among families in the bottom two income quintiles and among families in the top quintile. Relatively large increases in mortgage debt were also seen among couples with children (112%, or $108,200) and lone-parent families (109%, or $86,200). In percentage terms, homeowners living in the Prairies experienced the largest increases, and homeowners living in Prince Edward Island were the only ones not to record a significant increase in median mortgage debt over the period.

Almost three-quarters of families had a fixed-rate mortgage in 2016

Given the increase in the relative importance of mortgage debt among Canadian families, it is also important to examine how Canadians finance this debt. For the first time, the 2016 SFS collected information on the type of mortgage rate selected by Canadians on their principal residence: a fixed mortgage rate, a variable mortgage rate or some combination of both.

Homeowners can be motivated to choose a variable rate over a fixed rate in order to benefit from a lower interest rate (and hence lower mortgage payments), even if this means being exposed to a higher risk of rate increase in the near future. Conversely, homeowners who are more risk averse may prefer a fixed rate. These choices depend on the spread between the fixed and variable rate, and the type of mortgage products offered by the financial institutions for different amortization periods. The SFS did not ask respondents as to why they chose a variable rate, fixed rate, or combination of both. As a result, the section below is limited to a discussion of mortgage rate types across family characteristics.

In Canada, the majority of homeowners with a mortgage have a fixed mortgage rate.Note About 74% had a fixed mortgage rate, while 21% had a variable rate and 5% had a combination of both (Table 6). Note Families in the youngest age group, aged 19 to 24, were the least likely to have a fixed mortgage rate (63%).Note Those aged 25 to 34 (80%) and 65 and over (79%) were the most likely to have a fixed mortgage rate. Among the remaining age groups, about 72% had a fixed mortgage rate.

| Fixed | Variable | Combination | |

|---|---|---|---|

| percent | |||

| All | 74.2 | 20.9 | 4.9 |

| Age of major income earner | |||

| 19 to 24 | 62.5 | 32.8Note E: Use with caution | Note F: too unreliable to be published |

| 25 to 34 | 80.2 | 17.2 | 2.6Note E: Use with caution |

| 35 to 44 | 72.4 | 22.0 | 5.6 |

| 45 to 54 | 72.2 | 22.3 | 5.5 |

| 55 to 64 | 73.0 | 21.6 | 5.4 |

| 65 and over | 78.5 | 17.3 | 4.2Note E: Use with caution |

| Highest level of education of major income earner | |||

| Less than high school | 73.9 | 20.6 | 5.6Note E: Use with caution |

| High school diploma | 76.8 | 18.6 | 4.6Note E: Use with caution |

| Non-university postsecondary certificate or diploma | 75.2 | 19.7 | 5.2 |

| University degree or certificate | 71.8 | 23.7 | 4.5 |

| Family structure | |||

| Unattached individual | 81.0 | 15.0 | 4.0Note E: Use with caution |

| Couple, no children | 76.2 | 19.2 | 4.6 |

| Couple with children | 72.0 | 22.8 | 5.1 |

| Lone-parent family | 75.8 | 19.9 | Note F: too unreliable to be published |

| Other family types | 69.6 | 24.9 | 5.5 |

| Immigrant status of major income earner | |||

| Recent immigrant | 84.3 | 12.2Note E: Use with caution | Note F: too unreliable to be published |

| Established immigrant | 69.3 | 27.5 | 3.1Note E: Use with caution |

| Canadian-born individual | 75.5 | 19.0 | 5.5 |

| Labour force status | |||

| Paid employee | 74.7 | 20.5 | 4.8 |

| Self-employed | 65.3 | 28.3 | 6.4Note E: Use with caution |

| Not in labour force | 79.5 | 17.1 | 3.3Note E: Use with caution |

| Family income quintile | |||

| Bottom quintile | 75.2 | 20.5 | 4.3Note E: Use with caution |

| Second quintile | 77.7 | 18.1 | 4.2Note E: Use with caution |

| Third quintile | 77.5 | 17.5 | 5.1Note E: Use with caution |

| Fourth quintile | 70.3 | 24.7 | 5.0 |

| Top quintile | 70.6 | 23.7 | 5.7 |

| Outstanding mortgage debt | |||

| $100,000 and under | 74.4 | 20.0 | 5.6 |

| $100,001 to $200,000 | 75.1 | 20.1 | 4.9 |

| $200,001 to $300,000 | 74.6 | 20.5 | 4.9Note E: Use with caution |

| $300,001 to $400,000 | 74.0 | 23.1 | 2.9Note E: Use with caution |

| Over $400,000 | 70.2 | 25.1 | 4.7Note E: Use with caution |

| Number of years to pay full balance of mortgage | |||

| 0 to 5 | 73.7 | 20.9 | 5.4Note E: Use with caution |

| 6 to 10 | 68.2 | 26.0 | 5.8 |

| 11 to 15 | 74.1 | 21.1 | 4.7Note E: Use with caution |

| 16 to 20 | 73.5 | 21.7 | 4.8 |

| 21 to 25 | 78.9 | 17.3 | 3.8Note E: Use with caution |

| Over 25 | 82.6 | 13.2Note E: Use with caution | Note F: too unreliable to be published |

| Family budget | |||

| Yes | 75.8 | 19.7 | 4.5 |

| No | 72.7 | 22.1 | 5.2 |

| Amount of credit card balances paid off every month | |||

| Minimum or less than minimum | 78.7 | 15.3Note E: Use with caution | Note F: too unreliable to be published |

| More than minimum but less than full amount | 76.3 | 19.5 | 4.2 |

| Full amount | 71.7 | 23.2 | 5.1 |

| Do not have credit card | 86.8 | Note F: too unreliable to be published | Note F: too unreliable to be published |

| Someone in the family borrowed money through a payday loan in the past three years | |||

| Yes | 80.4 | Note F: too unreliable to be published | Note F: too unreliable to be published |

| No | 74.1 | 21.1 | 4.7 |

| Someone in the family ever declared bankruptcy or made a formal proposal or informal financial arrangements to creditors | |||

| Yes | 79.4 | 16.7 | Note F: too unreliable to be published |

| No | 73.7 | 21.3 | 5.0 |

| Region | |||

| Newfoundland and Labrador | 85.0 | 12.7Note E: Use with caution | Note F: too unreliable to be published |

| Prince Edward Island | 87.2 | 12.2Note E: Use with caution | Note F: too unreliable to be published |

| Nova Scotia | 76.1 | 20.3Note E: Use with caution | Note F: too unreliable to be published |

| New Brunswick | 79.6 | 16.3Note E: Use with caution | Note F: too unreliable to be published |

| Québec | 69.0 | 20.5Note E: Use with caution | Note F: too unreliable to be published |

| Montréal | 73.5 | 22.0 | 4.5Note E: Use with caution |

| Quebec excluding the CMAs of Québec and Montréal | 63.0 | 25.3 | 11.7Note E: Use with caution |

| Ottawa | 62.5 | 26.9Note E: Use with caution | Note F: too unreliable to be published |

| Toronto | 67.7 | 29.7 | 2.7Note E: Use with caution |

| Ontario excluding the CMAs of Ottawa and Toronto | 81.1 | 14.9 | 4.0Note E: Use with caution |

| Winnipeg | 77.7 | 21.1Note E: Use with caution | Note F: too unreliable to be published |

| Manitoba excluding the CMA of Winnipeg | 73.0 | 18.0Note E: Use with caution | Note F: too unreliable to be published |

| Regina | 87.0 | Note F: too unreliable to be published | Note F: too unreliable to be published |

| Saskatoon | 83.7 | Note F: too unreliable to be published | Note F: too unreliable to be published |

| Saskatchewan excluding the CMAs of Regina and Saskatoon | 80.2 | 12.7Note E: Use with caution | Note F: too unreliable to be published |

| Calgary | 79.4 | 16.3Note E: Use with caution | Note F: too unreliable to be published |

| Edmonton | 81.8 | 17.2Note E: Use with caution | Note F: too unreliable to be published |

| Alberta excluding the CMAs of Calgary and Edmonton | 88.3 | 9.0Note E: Use with caution | Note F: too unreliable to be published |

| Vancouver | 64.8 | 29.6 | 5.6Note E: Use with caution |

| British Columbia excluding the CMA of Vancouver | 79.2 | 17.7 | Note F: too unreliable to be published |

|

E use with caution F too unreliable to be published Source: Statistics Canada, Survey of Financial Security, 2016. |

|||

Homeowners who had a relatively small number of years remaining to pay off their mortgage were less likely to have a fixed rate, compared with those whose remaining amortization period was longer. Among those who reported that they would take at least 25 years to pay the full balance of their mortgage, 83% had a fixed rate, compared with 68% among those who had 6 to 10 years left to pay and 74% among those who had 0 to 5 years left.

A model was estimated to study the characteristics of families who were more (or less) likely to choose a fixed mortgage rate over a variable mortgage rate.Note This analysis is not meant to estimate a model of mortgage choice, but to see which types of families are likely to have a particular type of mortgage rate.

The results by age indicate that the youngest families (aged 19 to 24) were less likely than families with a major income earner aged 25 to 34 to have a fixed mortgage rate, but other age differences were statistically insignificant (Table 7). Couples with children (with a predicted probability of 0.72) and other family types (0.71) were less likely to have a fixed rate than unattached individuals (0.80).

| Model 1 | Model 2 | |

|---|---|---|

| predicted probability | ||

| Age of major income earner | ||

| 19 to 24 | 0.58Note * | 0.58Note * |

| 25 to 34 (ref.) | 0.78 | 0.78 |

| 35 to 44 | 0.73 | 0.73Note * |

| 45 to 54 | 0.75 | 0.74 |

| 55 to 64 | 0.73 | 0.73 |

| 65 and over | 0.74 | 0.74 |

| Highest level of education of major income earner | ||

| Less than high school (ref.) | 0.72 | 0.72 |

| High school diploma | 0.75 | 0.75 |

| Non-university postsecondary certificate or diploma | 0.75 | 0.74 |

| University degree or certificate | 0.74 | 0.74 |

| Family structure | ||

| Unattached individual (ref.) | 0.80 | 0.80 |

| Couple, no children | 0.76 | 0.76 |

| Couple with children | 0.72Note * | 0.72Note * |

| Lone-parent family | 0.75 | 0.75 |

| Other family types | 0.71Note * | 0.71Note * |

| Immigrant status of major income earner | ||

| Recent immigrant | 0.83 | 0.83 |

| Established immigrant | 0.71 | 0.72 |

| Canadian-born individual (ref.) | 0.75 | 0.75 |

| Labour force status of major income earner | ||

| Paid employee (ref.) | 0.75 | 0.75 |

| Self-employed | 0.67Note * | 0.67Note * |

| Not in labour force | 0.78 | 0.78 |

| Family income quintile | ||

| Bottom quintile (ref.) | 0.76 | 0.75 |

| Second quintile | 0.78 | 0.78 |

| Third quintile | 0.77 | 0.77 |

| Fourth quintile | 0.70Note * | 0.70Note * |

| Top quintile | 0.70Note * | 0.71 |

| Outstanding mortgage debt | ||

| $100,000 and under (ref.) | 0.74 | 0.75 |

| $100,001 to $200,000 | 0.75 | 0.75 |

| $200,001 to $300,000 | 0.74 | 0.74 |

| $300,001 to $400,000 | 0.74 | 0.73 |

| Over $400,000 | 0.73 | 0.73 |

| Number of years remaining to pay full balance of mortgage | ||

| 0 to 5 | 0.75Note * | 0.76Note * |

| 6 to 10 (ref.) | 0.69 | 0.69 |

| 11 to 15 | 0.74 | 0.74 |

| 16 to 20 | 0.73 | 0.73 |

| 21 to 25 | 0.78Note * | 0.78Note * |

| Over 25 | 0.83Note * | 0.83Note * |

| Family budget | ||

| Yes (ref.) | Note ...: not applicable | 0.76 |

| No | Note ...: not applicable | 0.73Note * |

| Amount of credit card balances paid off every month | ||

| Minimum or less than minimum | Note ...: not applicable | 0.78 |

| More than minimum but less than full amount | Note ...: not applicable | 0.76 |

| Full amount (ref.) | Note ...: not applicable | 0.73 |

| Do not have credit card | Note ...: not applicable | 0.82 |

| Someone in the family borrowed money through a payday loan in the past three years | ||

| Yes (ref.) | Note ...: not applicable | 0.74 |

| No | Note ...: not applicable | 0.74 |

| Someone in the family ever declared bankruptcy or made a formal proposal or informal financial arrangements to creditors | ||

| Yes (ref.) | Note ...: not applicable | 0.76 |

| No | Note ...: not applicable | 0.74 |

| Region | ||

| Newfoundland and Labrador | 0.85 | 0.84 |

| Prince Edward Island | 0.87Note * | 0.86Note * |

| Nova Scotia | 0.75 | 0.75 |

| New Brunswick | 0.79 | 0.78 |

| Québec | 0.69 | 0.69 |

| Montréal | 0.72 | 0.72 |

| Quebec excluding the CMAs of Québec and Montréal | 0.61Note * | 0.60Note * |

| Ottawa | 0.64 | 0.64 |

| Toronto (ref.) | 0.70 | 0.71 |

| Ontario excluding the CMAs of Ottawa and Toronto | 0.81Note * | 0.80Note * |

| Winnipeg | 0.77 | 0.77 |

| Manitoba excluding the CMA of Winnipeg | 0.72 | 0.72 |

| Regina | 0.87Note * | 0.87Note * |

| Saskatoon | 0.83 | 0.83 |

| Saskatchewan excluding the CMAs of Regina and Saskatoon | 0.80 | 0.80 |

| Calgary | 0.81Note * | 0.81Note * |

| Edmonton | 0.82Note * | 0.82Note * |

| Alberta excluding the CMAs of Calgary and Edmonton | 0.88Note * | 0.88Note * |

| Vancouver | 0.65 | 0.66 |

| British Columbia excluding the CMA of Vancouver | 0.79Note * | 0.79Note * |

... not applicable

|

||

Families in the fourth and fifth income quintiles were less likely to have a fixed-rate mortgage, compared with those in the bottom quintile. In addition, families whose major income earner was self-employed were less likely to have a fixed rate than families whose major income earner was a paid employee.

While the amount of outstanding mortgage debt did not have any association with the type of mortgage rate, the amortization period did.Note Compared with those who had 6 to 10 years left (0.69) to pay the full balance of their mortgage, homeowners who had 0 to 5 years (0.75), 21 to 25 years (0.78) and more than 25 years (0.83) left were more likely to have a fixed-rate mortgage.Note The results for homeowners who had 11 to 20 years left to pay their mortgage were statistically insignificant. As more of the mortgage payment goes to principal, families with just a few years remaining on their mortgage may be tempted to secure their payments over last few years of their amortization period; they may also benefit from advantageous fixed rates offered by lenders. At the other end of the spectrum, people with long amortization periods may want to opt for more stability, given the long time left before their mortgage is paid off.

Finally, when financial behaviour variables are added in the model, the results showed that families who maintained a household budget were more likely to pick a fixed rate, perhaps reflecting the fact that those who budget prefer the certainty of fixed payments over time.

Conclusion

Although homeownership rates have remained relatively constant in Canada, debt has been increasing in recent years. From 2012 to 2016, mortgage debt accounted for the entire increase in debt among Canadian families with debt. In 2016, mortgage debt accounted for 81% of total debt among Canadian families. The increase in mortgage debt has several implications for the housing market in Canada.

First, the increase in mortgage debt implies that Canadians could take longer to pay off their houses. From 1999 to 2016, the proportion of Canadians who had paid their houses in full declined from 46% to 43%. If not for the aging of the population, the decline would have been even more pronounced. This is because older individuals are typically more likely to have paid off their house in full than younger people.

Second, the results suggest that even though mortgage debt increased in almost every demographic group, the magnitude of the increase was not the same for every group. Specifically, mortgage debt was higher among couples with children, homeowners aged 25 to 44, homeowners with higher education and higher-income families. These groups also recorded the largest increase in mortgage debt from 1999 and 2016. However, debt also increased notably among some vulnerable groups, including lone parents and recent immigrants.

Third, the increase in mortgage debt also suggests that the financial choices of Canadians regarding the type of mortgage rate are important. In 2016, three-quarters of Canadians financed their mortgages via fixed-rate loans, with some types of families being particularly more likely to choose a fixed rate, including older Canadians, homeowners in low income quintiles, and homeowners with a longer amortization period.

Finally, the results suggest that there are some important regional variations in homeownership, mortgage debt and the type of mortgage rate. These differences may be related to variations in prices, regional economic conditions, differences in housing conditions, and differences in local preferences and choices. More research will be needed to better understand regional differences in mortgage debt, homeownership and type of mortgage rate.

Sharanjit Uppal is a senior researcher with Statistics Canada’s Insights on Canadian Society.

Start of text box 1

Data sources

Data from the 1999, 2005, 2012 and 2016 Survey of Financial Security (SFS) were used in this study. The SFS is a voluntary survey that collects information from a sample of Canadian families on their assets, debts, employment, income and education. Information is collected on the value of all major financial and non-financial assets, and on the money owing on mortgages, vehicles, credit cards, student loans and other debts.

The SFS covers the population living in the 10 provinces. Excluded from the survey coverage are people living on reserves and in other Aboriginal settlements in the provinces; official representatives of foreign countries living in Canada and their families; members of religious and other communal colonies; members of the Canadian Forces living on military bases or in military camps; and people living full time in institutions, such as inmates of penal institutions and chronic care patients living in hospitals and nursing homes.

In this study, individual characteristics such as age and education reflect those of the major income earner of the family.

Definitions

Family refers to the economic family, defined as two or more people living in the same dwelling who are related by blood, marriage or adoption, or who are living common law, as well as single people who are living either alone or with others to whom they are unrelated.

Total debt pertains to total family debt and includes mortgage debt on the principal residence and all other real estate (Canadian and foreign), as well as consumer debt.

Mortgage debt refers to debt owed by families on their principal residence and all other real estate (Canadian and foreign).

Consumer debt includes outstanding debt on credit cards, personal and home equity lines of credit, and secured and unsecured loans from banks and other institutions (including vehicle loans), as well as other unpaid bills.

Income quintiles are based on the total before-tax economic family income adjusted for family size (i.e., divided by the square root of the family size).

End of text box 1

Start of text box 2

In 2016, about 7% of all Canadian families carried mortgage debt on properties other than their principal residence (Chart 2).Note Among those who had such debt, the median debt was $183,000. Some types of families were more likely to fall into this category. About 17% of the self-employed and 14% of families in the upper income quintile carried other mortgage debt. Other groups that were more likely to have such debt included families whose major income earner was aged 45 to 64 (10%), had a university degree (9%), was an established immigrant (9%), belonged to other family types (11%) or was a resident of Alberta (10%).

Data table for Chart 2

| 2016 | |

|---|---|

| proportion (%) | |

| Province of residence is Alberta | 10.0 |

| Top income quintile | 14.4 |

| Self-employed | 16.7 |

| Established immigrant | 9.1 |

| Other family type | 10.7 |

| University degree | 9.4 |

| Aged 45 to 64 | 9.8 |

| All families | 6.9 |

| Source: Statistics Canada, Survey of Financial Security, 2016. | |

End of text box 2

- Date modified: