StatCan COVID-19: Data to Insights for a Better Canada Outlook of rural businesses and impacts related to COVID-19, second quarter of 2021

StatCan COVID-19: Data to Insights for a Better Canada Outlook of rural businesses and impacts related to COVID-19, second quarter of 2021

Archived Content

Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject to the Government of Canada Web Standards and has not been altered or updated since it was archived. Please "contact us" to request a format other than those available.

by Marina Smailes, Andrew Balcom and Jason Wong

Text begins

By the end of the first quarter of 2021, real gross domestic product (GDP) rose by 1.4%, and edged up 0.3% compared with the first quarter of 2020.Note While COVID-19 vaccination rates slowly rose and restrictions on businesses and individuals eased in the second quarter of 2021, businesses still faced a high degree of uncertainty due to the pandemic’s third wave.

The impacts of the pandemic on businesses vary across industry and region. Using the results of the Canadian Survey on Business Conditions (CSBC),Note second quarter of 2021, this analysis focuses on businesses in rural areas.Note This survey was conducted from early April to early May 2021, with the aim of developing a detailed understanding of current business practices and business expectations moving forward, as well as of the ongoing pandemic’s effects on businesses.

Results of the CSBC, second quarter of 2021, show that the most common challenges rural businesses expect to face over the next three-monthNote horizon are the rising cost of inputs, the cost of insurance, government regulations and recruiting skilled employees.

Within the next 12 months, 6.3% of rural businesses plan to sell, close or transfer, a decrease from 7.3% of businesses reporting the same plans in the first quarter of 2021. Conversely, one in seven rural businesses (14.1%) plan to expand, restructure, invest or acquire other businesses in the next 12 months.

Rural businesses were less likely than urban businesses to consider having to lay off staff over the next 12 months if they continue to operate at their current level of revenue and expenditures (16.0% rural, 21.7% urban). Over the same 12-month horizon, 16.0% of rural businesses plan on training existing employees in new skills, although this figure ranged from 33.2% of manufacturing businesses to 3.6% of real estate, rental and leasing businesses.

Rising cost of inputs remains largest obstacle over the next three months for rural businesses

The top obstacle businesses expect to face over the next three months is the rising cost of inputs, for both rural (42.5%) and urban (36.8%) businesses. Inputs include labour, capital, energy and raw materials. The Raw Materials Prices Index was up 56.4% year-over-year in April 2021,Note while the Unit Labour Cost remained virtually unchanged from the fourth quarter of 2020 (increased by +0.1%).Note

While the cost of inputs remained the same top obstacle from the first quarter of 2021,Note the second and third most-common obstacles are now the cost of insurance (32.7% rural, 24.9% urban) and government regulations (29.4% rural, 21.9% urban). Recruiting skilled employees remains the fourth most-common obstacle.

In addition, rural businesses are more than twice as likely to expect the speed of internet connections to be an obstacle (18.5%) compared to urban businesses (8.1%) in the second quarter of 2021. Rural access to high speed internet can be limited in some areas, with only approximately 23% of rural households having access to a 50/10 Mbps internet connection.Note After the rising cost of inputs, urban businesses’ second most-common obstacle was attracting new or returning customers (29.9%) which was less of a perceived obstacle for rural businesses (18.0%).

Data table for Chart 1

| Obstacles for business | Rising cost of inputs | Cost of insurance | Government regulations | Recruting skilled employees |

|---|---|---|---|---|

| percent | ||||

| Rural business | 42.5 | 32.7 | 29.4 | 29.4 |

| Urban business | 36.8 | 24.9 | 21.9 | 27.5 |

|

Note: Urban businesses are provided for comparison only and may not have the same top four obstacles as rural businesses. Source: Canadian Survey on Business Conditions, second quarter of 2021. |

||||

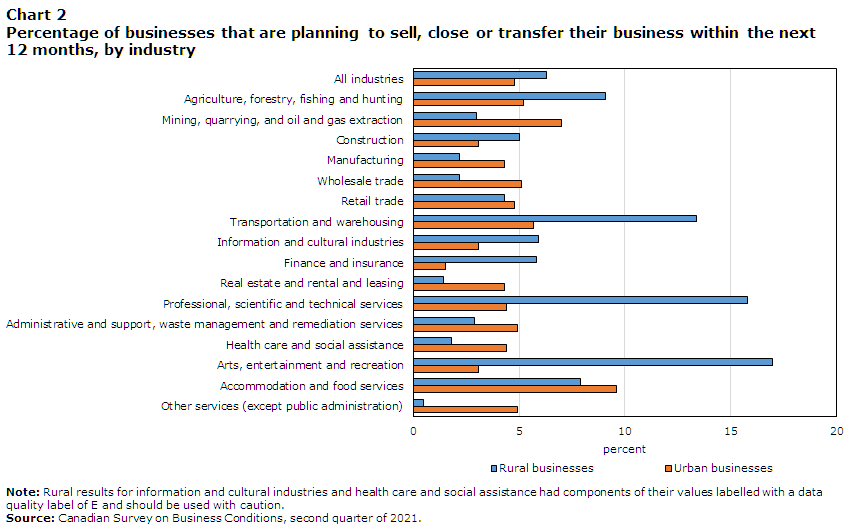

Decrease in plans to sell, close, or transfer led by real estate and rental and leasing industry

In the second quarter of 2021, 6.3% of rural businesses and 4.8% of urban businesses reported intentions of selling, closing or transferring, compared to 7.3% and 6.2%, respectively, in the first quarter. Rural businesses in two industries were three to five times more likely to have plans to sell, close, or transfer compared to their urban counterparts: arts, entertainment and recreation (17.0% of rural businesses, 3.1% of urban businesses) and professional, scientific and technical services (15.8% rural, 4.4% urban).

When looking at rural businesses by industry across both quarters, the general decrease in the percentage of businesses planning to sell, close, or transfer was largely due to four industries: real estate and rental and leasing (-18.8 percentage points), arts, entertainment and recreation (-16.7 percentage points), accommodation and food services (-13.8 percentage points), and other services (except public administration; -11.0 percentage points). Activities at offices of real estate agents and brokers rose to record highs in March 2021, reaching $19.4 billion.Note

There were two industries where the percentage of rural businesses that had plans to sell, close, or transfer increased by 10 to 12 percentage points between the two quarters: transportation and warehousing and professional, scientific and technical services.

Data table for Chart 2

| Rural businesses | Urban businesses | |

|---|---|---|

| percent | ||

| All industries | 6.3 | 4.8 |

| Agriculture, forestry fishing and hunting | 9.1 | 5.2 |

| Mining, quarrying, and oil and gas extraction | 3.0 | 7.0 |

| Construction | 5.0 | 3.1 |

| Manufacturing | 2.2 | 4.3 |

| Wholesale trade | 2.2 | 5.1 |

| Retail trade | 4.3 | 4.8 |

| Transportation and warehousing | 13.4 | 5.7 |

| Information and cultural industries | 5.9 | 3.1 |

| Finance and insurance | 5.8 | 1.5 |

| Real estate and rental and leasing | 1.4 | 4.3 |

| Professional, scientific and technical services | 15.8 | 4.4 |

| Administrative and support, waste management and remediation services | 2.9 | 4.9 |

| Health care and social assistance | 1.8 | 4.4 |

| Arts, entertainment and recreation | 17.0 | 3.1 |

| Accommodation and food services | 7.9 | 9.6 |

| Other services (except public administration) | 0.5 | 4.9 |

|

Note: Rural results for information and cultural industries and health care and social assistance had components of their values labelled with a data quality label of E and should be used with caution. Source: Canadian Survey on Business Conditions, second quarter of 2021. |

||

Some businesses demonstrate optimistic outlooks in their plans over the next 12 months to expand, restructure, invest in, and/or acquire other businesses. One in seven (14.1%) rural businesses were contemplating at least one of these changes compared to one in nine (11.7%) urban businesses. Rural businesses that were most likely to plan for expansion, restructuring, investment, and/or acquisition were in the industries of administrative and support, waste management and remediation services (26.3%), and accommodation and food services (24.4%). These rural businesses were also more likely to plan for these changes than their urban counterparts, by 13 to 15 percentage points.

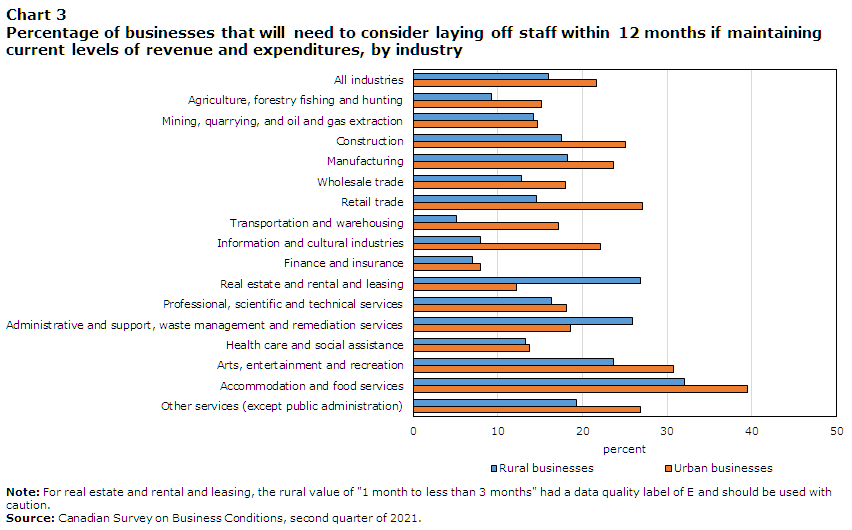

Rural businesses were less likely to consider layoffs to adjust to the pandemic and had similar plans to urban counterparts when it comes to investing in training and skills development

While there is optimism for reduced restrictions in the summer of 2021, some businesses expect to consider layoffs within the next 12 months, if their current revenue and expenditure levels remain the same.

The percentage of rural businesses that expect to consider layoffs within the next 12 months should their current financial situation remain unchanged was 16.0%, below that of their urban counterparts at 21.7%. The industries with the highest rates of rural businesses that would have to consider layoffs were accommodation and food services (32.0%), real estate and rental and leasing (26.9%), administrative and support, waste management and remediation services (25.9%), and arts, entertainment and recreation (23.7%). The industries with the lowest rates were transportation and warehousing (5.1%), finance and insurance (7.0%), and information and cultural industries (7.9%).

The largest rural-urban difference by industry was in real estate and rental and leasing, where the percentage of rural businesses that would need to consider layoffs should their financial situation remain the same over the next 12 months was 14.7 percentage points higher than urban businesses (26.9% for rural, and 12.2% for urban). The second-largest rural-urban difference was in information and cultural industries, where urban businesses who may consider layoffs was 14.2 percentage points higher than rural (7.9% for rural, and 22.1% for urban).

Data table for Chart 3

| Rural businesses | Urban businesses | |

|---|---|---|

| percent | ||

| All industries | 16.0 | 21.7 |

| Agriculture, forestry fishing and hunting | 9.2 | 15.1 |

| Mining, quarrying, and oil and gas extraction | 14.2 | 14.7 |

| Construction | 17.5 | 25.1 |

| Manufacturing | 18.2 | 23.6 |

| Wholesale trade | 12.8 | 18.0 |

| Retail trade | 14.5 | 27.1 |

| Transportation and warehousing | 5.1 | 17.1 |

| Information and cultural industries | 7.9 | 22.1 |

| Finance and insurance | 7.0 | 7.9 |

| Real estate and rental and leasing | 26.9 | 12.2 |

| Professional, scientific and technical services | 16.3 | 18.1 |

| Administrative and support, waste management and remediation services | 25.9 | 18.6 |

| Health care and social assistance | 13.2 | 13.7 |

| Arts, entertainment and recreation | 23.7 | 30.8 |

| Accommodation and food services | 32.0 | 39.5 |

| Other services (except public administration) | 19.3 | 26.9 |

|

Note: For real estate and rental and leasing, the rural value of "1 month to less than 3 months" had a data quality label of E and should be used with caution. Source: Canadian Survey on Business Conditions, second quarter of 2021. |

||

Businesses continue to adapt in response to the pandemic, including retraining employees to fit business needs. Over the next 12 months, a similar share of urban and rural businesses plan on training current employees in new skills (17.2% and 16.0%, respectively).

Among certain rural industries, over 20% of businesses plan on retraining employees: manufacturing (33.2%), retail trade (26.2%), arts, entertainment and recreation (24.6%), finance and insurance (24.3%), and health care and social assistance (21.6%). In these industries, a higher percentage of rural businesses plan on implementing retraining compared to their urban counterparts.

Industries where few rural businesses are planning on training their staff in new skills include real estate and rental and leasing (3.6%) and transportation and warehousing (4.5%).

Data table for Chart 4

| Rural businesses | Urban businesses | |

|---|---|---|

| percent | ||

| All industries | 16.0 | 17.2 |

| Agriculture, forestry fishing and hunting | 15.7 | 13.9 |

| Mining, quarrying, and oil and gas extraction | 8.6 | 15.5 |

| Construction | 14.5 | 15.8 |

| Manufacturing | 33.2 | 22.9 |

| Wholesale trade | 13.0 | 17.0 |

| Retail trade | 26.2 | 16.9 |

| Transportation and warehousing | 4.5 | 9.0 |

| Information and cultural industries | 11.5 | 29.3 |

| Finance and insurance | 24.3 | 19.7 |

| Real estate and rental and leasing | 3.6 | 15.8 |

| Professional, scientific and technical services | 11.2 | 20.3 |

| Administrative and support, waste management and remediation services | 13.2 | 17.4 |

| Health care and social assistance | 21.6 | 15.4 |

| Arts, entertainment and recreation | 24.6 | 14.3 |

| Accommodation and food services | 19.3 | 21.7 |

| Other services (except public administration) | 9.7 | 15.1 |

| Source: Canadian Survey on Business Conditions, second quarter of 2021. | ||

References

Statistics Canada. (2021). Canadian Survey on Business Conditions, second quarter of 2021.

Statistics Canada. (2021). Canadian Survey on Business Conditions, first quarter of 2021.

Methodology

From April 1 to May 6, representatives from businesses across Canada were invited to take part in an online questionnaire about how COVID-19 is affecting their business. This iteration of the Canadian Survey on Business ConditionsNote used a stratified random sample of business establishments with employees classified by geography, industry sector, and size. Estimation of proportions is done using calibrated weights to calculate the population totals in the domains of interest.

Businesses were classified as rural or urban based on their geographic location. The 2016 Census Subdivision Boundary File was used to identify all businesses’ Census Subdivisions (CSD) based on location. Businesses located in CSDs classified as either Census Metropolitan Areas or Census Agglomerations were classified as urban. All businesses in other locations were classified as rural.

- Date modified: