Economic and Social Reports

Business ownership among persons with disabilities in Canada

DOI: https://doi.org/10.25318/36280001202101200004-eng

Skip to text

Text begins

Abstract

This paper provides a sociodemographic profile of business owners with disabilities using 2017 administrative tax data. It evaluates how sociodemographic characteristics of business owners with disabilities intersect and compares them with those of business owners without disabilities. It also examines the firm-level measures of these businesses, including firm size, industry, exports and financial characteristics.

Authors

Amélie Lafrance-Cooke and Robby Bemrose are with the Economic Analysis Division at Statistics Canada.

Acknowledgements

This study was funded by Women and Gender Equality Canada. The authors would like to thank Danny Leung, Lyming Huang, April Doreleyers, Marysa Vachon, Julie Burns, Nicole Yaansah, Sarah Jane Ferguson, Patrice Rivard, Winnie Chan and Haleigh Prevost for their helpful comments.

Introduction

According to the 2017 Canadian Survey on Disability (CSD), approximately 3.7 million Canadians aged 25 to 64 have a disability and, as a result, are limited in their daily activities (Morris et al. 2018). While about 65% of these working-age Canadians were also in the labour force, they are disproportionately underrepresented in the labour force compared with persons without disabilities (i.e., 85% of persons without disabilities are in the labour force). Previous research has shown that persons with disabilities face challenges and barriers in the labour market that can negatively impact their earnings (Jones 2011; Lechner and Vazquez-Alvarez 20103 and increase their likelihood of being in low-income groups (Wall 2017). The COVID-19 pandemic further highlighted the vulnerability of this population, particularly in terms of unique challenges that they may face, which intensified over the pandemic. These include reliance on help outside the household for daily activities and the likelihood of not having Internet access,Note which became an important asset to connect with others virtually and purchase goods online.

A potential solution to low labour force participation rates for persons with disabilities is self-employment or owning a business (Kitching 2014). Entrepreneurship can offer an entry into the labour market, which, in turn, can lead to improved income. It can provide more flexibility in the pace of work and, potentially, a greater ability to work from home (Kitching 2014).

According to the 2017 CSD, 8.6% of persons with disabilities were self-employed in 2016, compared with 11.1% of persons without disabilities. This contrasts slightly with evidence in the United States and in Europe, where higher self-employment rates were found among persons with disabilities (Kitching 2014). Nevertheless, such studies have found that persons with disabilities face specific barriers to entrepreneurship, including difficulties accessing capital and lack of appropriate and sensitive business support or advice (Boylan and Burchardt 2002). New businesses created by entrepreneurs with disabilities are less likely to become viable businessesNote (Renko, Harris and Caldwell 2015).

There have been few Canadian studies on business owners with disabilities, most likely because of the lack of available data on this group of individuals. The Survey on Financing and Growth of Small and Medium Enterprises (SFGSME) collects information on small and medium-sized enterprises that are majority-owned by persons with disabilities, but this survey is infrequent (i.e., every three years) and is limited in scope (e.g., there are limits to intersectional analysis). Nevertheless, it offers a glimpse of the profile of businesses that are majority-owned by persons with disabilities. Data for 2017 show that a small proportion (0.5%) of small and medium enterprises are majority-owned by persons with disabilities (Huang 2020). The majority of these businesses have between one and fewer than four employees, they tend to have sales growth between 1% and 10% per year, and a minority are exporters. In addition, the owners of businesses majority-owned by persons with disabilities tend to be young (younger than 49 years old), and they tend to have a postsecondary education or higher.

More recently, the quarterly Canadian Survey on Business Conditions has been collecting information to measure the impact of COVID-19 on businesses, including businesses majority-owned by persons with disabilities. While the survey cannot be used to examine the characteristics of businesses majority-owned by persons with disabilities before the pandemic, it continues to be an important contributor to the understanding of the effects of the pandemic on diverse groups of businesses. Results from the first survey undertaken in April 2020 suggest that businesses majority-owned by a person with disabilities may have been more negatively impacted. For instance, 4.7% of such businesses closed permanently, compared with 1.0% of businesses on average. About one-half of businesses majority-owned by a person with disabilities experienced a drop in revenue of more than 40% in early 2020 compared with the same period in 2019, relative to one-third of businesses on average.

The lack of recurring and comprehensive data on business ownership among persons with disabilities presents challenges in providing a full picture of this group, which, in turn, is needed to design policies to address barriers to business ownership. This paper attempts to fill this gap by providing a sociodemographic profile of business owners with disabilities using 2017 administrative tax data. It evaluates how sociodemographic characteristics of business owners with disabilities intersect and compares them with those of business owners without disabilities. It also examines the firm-level measures of these businesses. To the best of the authors’ knowledge, the administrative data have never been used for this type of study in Canada.

Data and methods

The data used to generate the sociodemographic characteristics of business owners with disabilities and the firm-level measures of the businesses they own are from the Canadian Employer–Employee Dynamics Database (CEEDD). This linkable employer–employee dataset is based on processed administrative data sources from Statistics Canada; the Canada Revenue Agency (CRA); Employment and Social Development Canada; and Immigration, Refugees and Citizenship Canada (Chan, Liu and Morissette 2018). The key variables used for this study are found in the T1 personal master file (T1PMF) in the CEEDD, which includes information from form T2201 Disability Tax Credit Certificate. The disability deduction claim is the variable used to identify individuals with disabilities.Note

There were four main data processing steps in the methodology. The first step entailed identifying persons with disabilities within the population of individual tax filers, together with extracting the associated sociodemographic and geographic variables. The second step involved aggregating the individual ownership shares for a business from the reporting units in the tax files to statistical units that correspond with the data collected at the firm level (i.e., enterprise). The third step consisted of linking the individuals with disabilities, along with their demographic variables, to the shareholders of the private enterprises they own and acquiring the associated firm-level measures. The fourth step involved deriving the ownership share of each enterprise by gender, immigrant status and disability status. Two approaches were used to identify the businesses owned by persons with disabilities, as follows: (1) the business has one or more owners who claim the disability tax credit (DTC), and (2) the business ownership share is greater than or equal to 51% for owners who claim the DTC. The subsequent sections describe the details of these processing steps.

Individual-level tax files

Persons with disabilities were identified in the individual-level T1PMF data file (General Income Tax and Benefit Return) if there was a claim made for either the DTC or the attendant care expenses deduction in the 2017 tax year, both of which are discussed in more detail in the next section. The T1PMF sociodemographic variables for this study are largely limited to age, gender and income. The geographic variable, province or territory of residence in the T1PMF, was also included. To obtain information on the immigrant status, the CEEDD Longitudinal Immigration Database (IMDB) file was linked to the T1PMF. The IMDB file contains immigration-related information for foreign-born individuals who have become landed immigrants in Canada since 1980 (Chan, Liu and Morissette 2018).

Enterprise-level ownership share

The business ownership share for incorporated businesses is found in the CEEDD T2 Corporation Tax Return, Schedule 50 Shareholder Information (T2S50) and for unincorporated businesses in the CEEDD T1 Financial Declaration and Business Declaration (T1FDBD). The pre-processing steps applied to generate the ownership share in these files can be found in a paper by Grekou, Li and Liu (2018). With the shareholder data, the main objective is to aggregate the percentage ownership shares to the enterprise-level statistical unit. For the incorporated businesses, this is done by linking the T2S50 by the Business Number (BN) to the National Accounts Longitudinal Microdata File (NALMF). The NALMF is an enterprise-level database that includes all enterprises that filed a Corporation Income Tax Return (T2), Statement of Remuneration Paid (T4 slip) or payroll statement of account for source deductions (PD7) (Grekou, Gu and Yan 2020). The NALMF provides the structure to link reporting units in the administrative data (i.e., BN) to institutional units (i.e., enterprise). Following the approach presented by Grekou, Li and Liu (2018), when the enterprise consists of more than one BN, the ownership share is adjusted by multiplying the individual ownership shares by the quotient of assets reported at the BN and enterprise level. If the enterprise has only one associated BN, the ownership share at the BN level is directly assigned to the enterprise. If assets are missing, each individual is assigned an equal ownership share of the enterprise. A similar approach is followed for the unincorporated businesses in the T1FDBD, using methods found in the paper by Grekou, Li and Liu (2018).

Identifying the business owners and firm-level data

The business owners are identified by linking the individual-level tax file (T1PMF) to the ownership share files of the incorporated (T2S50) and unincorporated (T1FDBD) businesses. There are 3,052,951 individuals (including duplicates, because an individual could own multiple businesses) in the T2 incorporated data; 2,927,428 were found in the T1 file (≈ 96%). There are 1,359,427 individuals in the T1 unincorporated data; 1,350,303 were found in the T1 file (≈ 99%). Business owners could be missing from the individual tax returns because they did not submit their taxes or they were late filing. The information could also have been entered incorrectly in either of the tax files.

The NALMF firm-level data are linked to the incorporated business ownership data by enterprise identifier to obtain the number of employees,Note North American Industry Classification System industry, capital cost allowance, net income, total assets, research and development (R&D) spending, total revenue, and exports for each firm. The same variables for the unincorporated businesses are already included in the T1FDBD file.Note

Ownership share by different subgroups

The firm-level ownership share is used to calculate the portion of ownership for each category within the gender and immigrant status variables. The individual ownership shares of the firm are summed by the categories to determine the percentage amount of each category within the firm. If the share of a category is greater than or equal to 51%, the class is labelled as majority-owned. If the share between the categories is the same, there is equal ownership. If there is no dominant category of ownership and the categories do not sum to 100%, the firm is labelled as missing. As described by Grekou, Li and Liu (2018), this can occur because only the shareholders with at least 10% of the shares of a private corporation are reported in the T2S50, and shareholders’ information can be misfiled or missing. The intersection of these demographic dimensions of ownership is evaluated through cross tabulations.

Disability tax credit: What is it and how well does it capture the population of persons with disabilities?

The DTC is a non-refundable tax credit that was introduced in 1988 to allow persons with disabilities to reduce the amount of income tax that they may have to pay. To be eligible for the DTC, an individual must experience difficulties performing activities of daily living, such as walking, speaking, feeding oneself or hearing, or other debilitating conditions that affect day-to-day living.Note An individual applying for the DTC must have a medical practitioner fill out form T2201 Disability Tax Credit Certificate, which certifies that the individual has a severe and prolonged disability. If the individual’s medical condition improves, they will no longer be eligible to receive the DTC. Persons can claim the DTC for their spouse or dependants, but this article will focus on individual claims.

In addition to the DTC, persons with disabilities can claim attendant care expenses. These may be fees paid for full-time care in a nursing home or salaries and wages of an attendant providing care within a person’s home. In most cases, the DTC and attendant care expenses cannot both be claimed. As a result, for the purposes of this paper, the number of persons with disabilities also includes persons claiming attendant care expenses, consisting of about 1,000 individuals who did not claim the DTC.

In 2017, about 841,000 Canadians aged 15Note and older claimed the DTC, representing 3.0% of the total number of individuals who completed a tax return, and 802,000 of these claimants were aged 25 and older, which is the age group studied in this paper. This comparesNote with the 6.2 million Canadians aged 15 and older with disabilities based on the 2017 CSD, of whom about 2.7 million had a severe or very severe disability, limiting their daily activities. The considerably lower number of individuals identified in the tax data is to be expected because individuals with disabilities might not have enough taxable income to claim the DTC or might not be in the labour force. In addition, some persons with disabilities may not be claiming the DTC because they thought they did not meet the criteria, they did not know that the tax credit existed or they were not able to obtain a completed certificate (T2201) from their doctor (Duclos and Langlois 2003).

Among persons aged 25 and older, more than half (56.4%) of individuals who claim the DTC are older than 65, 55% of whom are women (Chart 1). The share of women who claim the DTC increases with age; for persons aged 25 to 44, 54.1% of claimants are men. The gender distribution of persons claiming the DTC is similar to the sex distribution in the CSD among individuals aged 45 and older: 53.1% of persons with disabilities aged 45 to 64 are women, and 56.2% of persons with disabilities aged 65 and older are women. In contrast, among the 25-to-44 age group, women represent 58.7% of persons with disabilities based on the CSD.

Data table for Chart 1

| Age group | Male | Female | Male | Female |

|---|---|---|---|---|

| count | percent | |||

| 25 to 44 years | 53,104 | 45,144 | 54.1 | 45.9 |

| 45 to 64 years | 118,189 | 127,539 | 48.1 | 51.9 |

| 65 years and older | 188,497 | 230,000 | 45.0 | 55.0 |

|

Note: Excludes individuals for whom age or gender is missing. Source: Statistics Canada, Canadian Employer–Employee Dynamics Database. |

||||

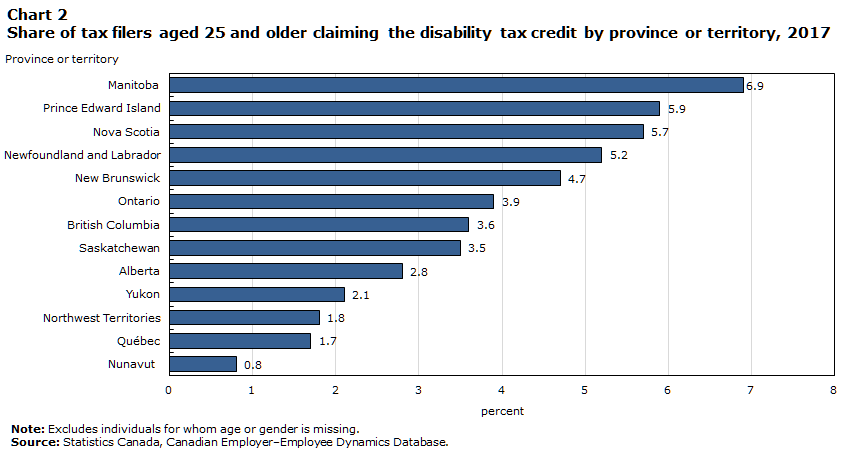

At the provincial and territorial level, a higher share of individuals claimed the DTC in Manitoba (6.9%) and in the Atlantic provinces, ranging from 4.7% in New Brunswick to 5.9% in Prince Edward Island (Chart 2).

Data table for Chart 2

| Province or territory | Percent |

|---|---|

| Manitoba | 6.9 |

| Prince Edward Island | 5.9 |

| Nova Scotia | 5.7 |

| Newfoundland and Labrador | 5.2 |

| New Brunswick | 4.7 |

| Ontario | 3.9 |

| British Columbia | 3.6 |

| Saskatchewan | 3.5 |

| Alberta | 2.8 |

| Yukon | 2.1 |

| Northwest Territories | 1.8 |

| Québec | 1.7 |

| Nunavut | 0.8 |

|

Note: Excludes individuals for whom age or gender is missing. Source: Statistics Canada, Canadian Employer–Employee Dynamics Database. |

|

What is also noticeable from Chart 2 is the low share of DTC claimants in Quebec compared with the other regions. Low shares of persons with disabilities in Quebec have been presented in the literature (e.g., Dunstan 2003; Mackenzie 2013; Arim 2015). The low share of disability claims could be a result of the Revenu Québec provincial disability tax credit, which might be claimed instead of the federal DTC.

With the form T2201 Disability Tax Credit Certificate, it is possible to determine the type and number of disabilities accepted by the CRA for each individual who claims the tax credit, such as markedly restricted mobility or walking, vision and speech. Nearly three-quarters (68.2%) of individuals claiming the credit specify mobility or restricted walking as a disability (Table 1). The second most common disability is mental functions necessary for everyday life, which 39.1% of individuals specify on form T2201.

| Type of impairment | Number | Percentage of individuals claiming the DTCTable 1 Note 1 |

|---|---|---|

| Mobility | 573,679 | 68.20 |

| Mental function necessary for everyday life | 328,971 | 39.10 |

| Dressing | 226,398 | 26.90 |

| Eliminating | 111,436 | 13.30 |

| Feeding | 93,131 | 11.10 |

| Speech | 61,588 | 7.30 |

| Hearing | 61,487 | 7.30 |

| Life sustaining therapy | 55,635 | 6.60 |

| Vision | 53,186 | 6.30 |

| Other | 5,215 | 0.60 |

Source: Statistics Canada, Canadian Employer–Employee Dynamics Database. |

||

Results

Sociodemographic characteristics of business owners with disabilities

This section describes the type of disability and sociodemographic characteristics (i.e., age, gender, immigrant status and income) of the business owners with disabilities. Of the individuals that claim the DTC, 1.3% (17,575) are shareholders of unincorporated businesses (T1FDBD) and 1.2% (23,526) are shareholders of incorporated (T2S50) businesses.Note Note Results in this section will be presented separately for the two types of businesses.

Business owners with disabilities tend to be older than business owners without disabilities and a higher share are women

| Type of impairment | Unincorporated | Incorporated | ||

|---|---|---|---|---|

| number | percentage | number | percentage | |

| Mobility | 9,930 | 56.50 | 13,088 | 55.60 |

| Dressing | 3,589 | 20.40 | 5,026 | 21.40 |

| Mental function necessary for everyday life | 2,356 | 13.40 | 3,980 | 16.90 |

| Eliminating | 1,973 | 11.20 | 2,770 | 11.80 |

| Life sustaining therapy | 1,645 | 9.40 | 2,226 | 9.50 |

| Feeding | 1,302 | 7.40 | 1,993 | 8.50 |

| Hearing | 1,170 | 6.70 | 1,409 | 6.00 |

| Vision | 784 | 4.50 | 1,189 | 5.10 |

| Speech | 608 | 3.50 | 1,015 | 4.30 |

| Other | 14 | 0.10 | 21 | 0.10 |

|

Note: Summing the percentages does not equal to 100% because of individuals specifying more than one disability. Source: Statistics Canada, Canadian Employer–Employee Dynamics Database. |

||||

The types of disability of the business owners are presented in Table 2. The distribution of disabilities for business owners of both incorporated and unincorporated businesses is similar. A mobility disability was reported by more than half of business owners, as the most common disability, followed by dressing and mental function disabilities.

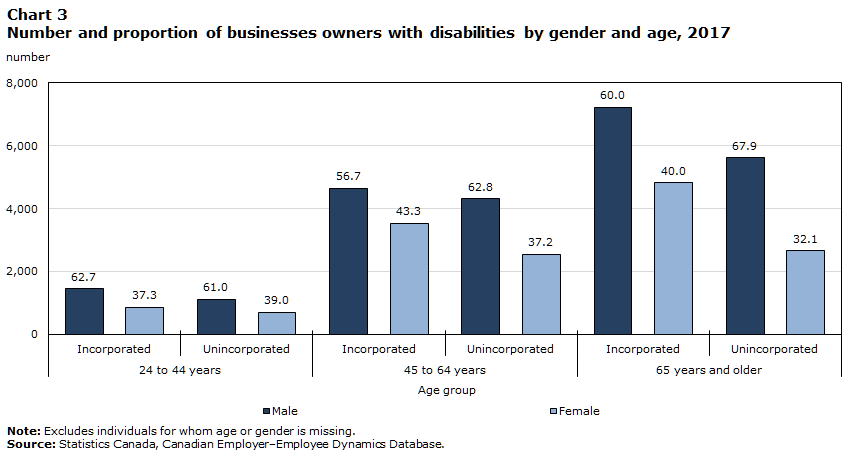

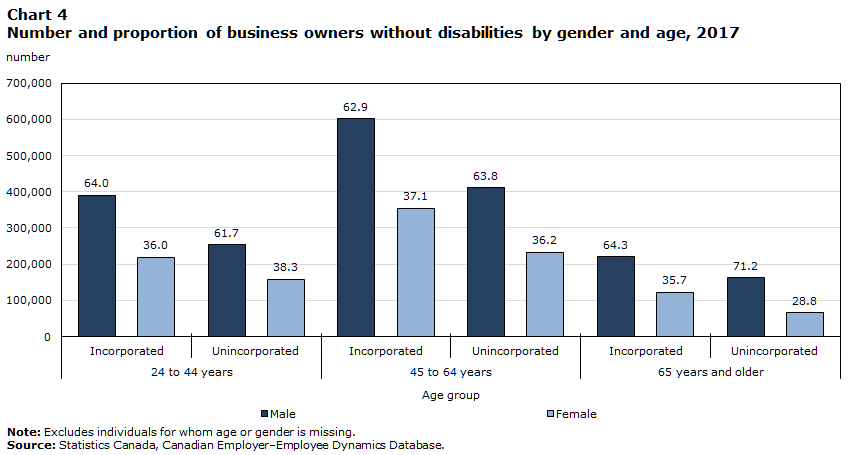

The age distribution among business owners with disabilities (Chart 3) is noticeably different than that among business owners without disabilities (Chart 4). The number of business owners with disabilities increases with age for both unincorporated and incorporated businesses, with the majority of business owners aged 65 and older (Chart 3). This is driven by the fact that more than half of DTC claimants are aged 65 and older. In contrast, business owners aged 45 to 64 without disabilities represent the largest proportion of business owners (Chart 4).

There is a larger share of women with disabilities aged 45 and older who own incorporated businesses compared with unincorporated businesses (Chart 3). In particular, 40.0% of owners of incorporated businesses aged 65 and older who claimed the DTC are women, compared with 32.1% of owners of unincorporated businesses. Among the 45-to-64 age category of business owners with disabilities, 43.3% of incorporated businesses and 37.2% of unincorporated businesses are owned by women. These two shares are higher than what is observed for business owners without disabilities (37.1% and 36.2%) (Chart 4). Nevertheless, while women account for a larger share of DTC claimants among older age groups, business ownership remains male-dominated.

Data table for Chart 3

| Age group | Male | Female | Male | Female | |

|---|---|---|---|---|---|

| number | percent | ||||

| 24 to 44 years | Incorporated | 1,448 | 862 | 62.7 | 37.3 |

| Unincorporated | 1,114 | 712 | 61.0 | 39.0 | |

| 45 to 64 years | Incorporated | 4,643 | 3,539 | 56.7 | 43.3 |

| Unincorporated | 4,304 | 2,549 | 62.8 | 37.2 | |

| 65 years and older | Incorporated | 7,212 | 4,817 | 60.0 | 40.0 |

| Unincorporated | 5,609 | 2,652 | 67.9 | 32.1 | |

|

Note: Excludes individuals for whom age or gender is missing. Source: Statistics Canada, Canadian Employer–Employee Dynamics Database. |

|||||

Data table for Chart 4

| Age group | Male | Female | Male | Female | |

|---|---|---|---|---|---|

| number | percent | ||||

| 24 to 44 years | Incorporated | 390,346 | 219,181 | 64.0 | 36.0 |

| Unincorporated | 254,250 | 158,081 | 61.7 | 38.3 | |

| 45 to 64 years | Incorporated | 601,891 | 355,163 | 62.9 | 37.1 |

| Unincorporated | 410,941 | 232,675 | 63.8 | 36.2 | |

| 65 years and older | Incorporated | 221,020 | 122,909 | 64.3 | 35.7 |

| Unincorporated | 162,356 | 65,778 | 71.2 | 28.8 | |

|

Note: Excludes individuals for whom age or gender is missing. Source: Statistics Canada, Canadian Employer–Employee Dynamics Database. |

|||||

Immigrant business owners with disabilities are younger than non-immigrant business owners with disabilities

Few immigrant business owners claim the DTC. For example, among incorporated businesses, immigrant business owners represent 22.3% of business owners who do not claim the DTC, compared with 7.6% of businesses owners who claim the DTC (Table 3). Since similar shares of the Canadian population of immigrants and non-immigrants have disabilities,Note the lower share of immigrants claiming the DTC may be because of a higher proportion of immigrants, particularly recent immigrants, who are not aware of the tax credit.

| Incorporated | Unincorporated | |||

|---|---|---|---|---|

| number | share of all incorporated (percent) | number | share of all unincorporated (percent) | |

| Business owners with disabilities | ||||

| Immigrant | ||||

| 25 to 44 years | 327 | 1.50 | 222 | 1.30 |

| 45 to 64 years | 956 | 4.20 | 771 | 4.60 |

| 65 years and older | 438 | 1.90 | 239 | 1.40 |

| 25 years and older | 1,721 | 7.60 | 1,232 | 7.30 |

| Non-immigrant | ||||

| 25 to 44 years | 1,983 | 8.80 | 1,604 | 9.50 |

| 45 to 64 years | 7,226 | 32.10 | 6,082 | 35.90 |

| 65 years and older | 11,591 | 51.50 | 8,022 | 47.40 |

| 25 years and older | 20,800 | 92.40 | 15,708 | 92.70 |

| Business owners without disabilities | ||||

| Immigrant | ||||

| 25 to 44 years | 187,605 | 9.80 | 112,807 | 8.80 |

| 45 to 64 years | 214,453 | 11.20 | 150,995 | 11.80 |

| 65 years and older | 24,895 | 1.30 | 15,309 | 1.20 |

| 25 years and older | 426,953 | 22.30 | 279,111 | 21.70 |

| Non-immigrant | ||||

| 25 to 44 years | 421,922 | 22.10 | 299,524 | 23.30 |

| 45 to 64 years | 742,601 | 38.90 | 492,621 | 38.40 |

| 65 years and older | 319,034 | 16.70 | 212,825 | 16.60 |

| 25 years and older | 1,483,557 | 77.70 | 1,004,970 | 78.30 |

|

Note: Excludes individuals for whom age is missing. Source: Statistics Canada, Canadian Employer–Employee Dynamics Database. |

||||

Immigrant business owners who claim the DTC are younger than non-immigrant owners who claim the DTC, in the case of both unincorporated and incorporated businesses. For instance, 77.1% of immigrant business owners with disabilities are aged 25 to 64, compared with 46.3% of non-immigrant business owners with disabilities (Table 3). More than one-half of immigrant business owners with disabilities are in the 45-to-64 age group.

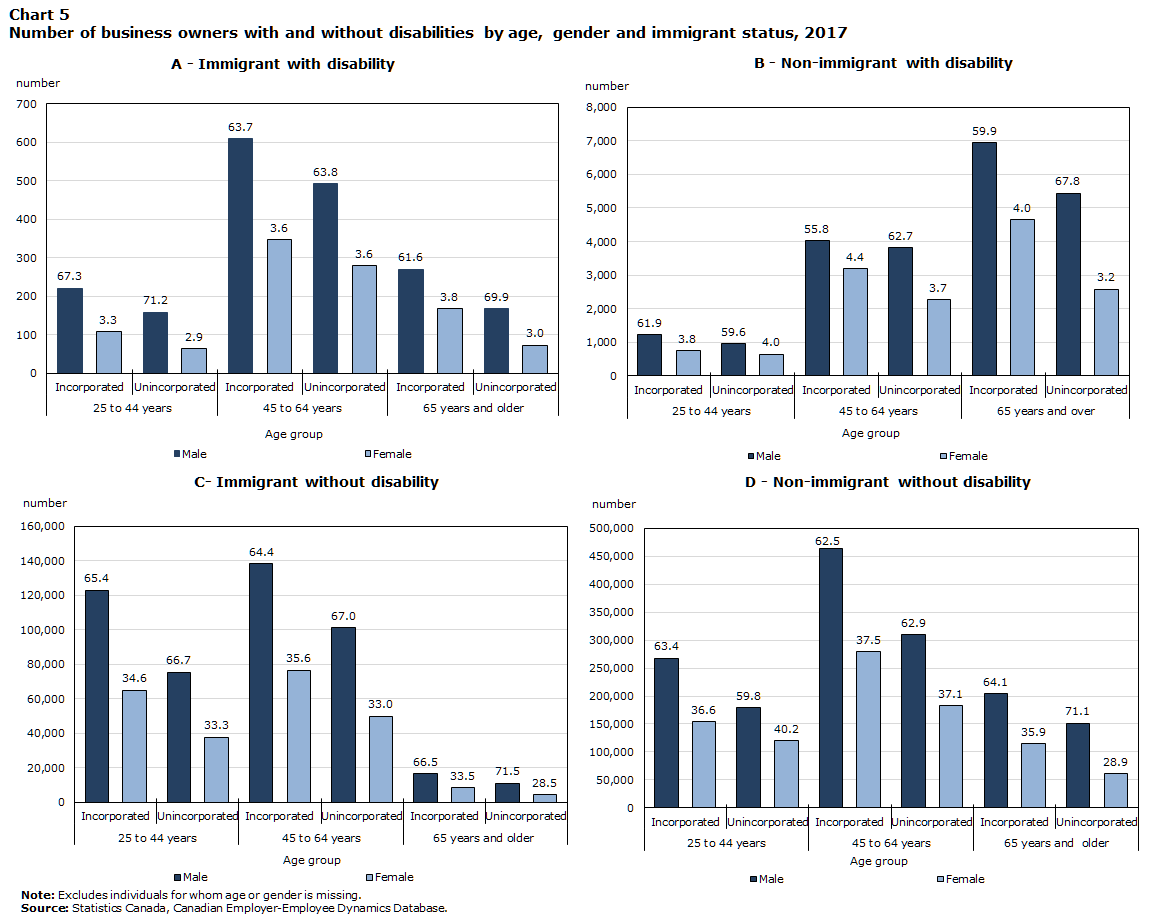

Among immigrant business owners, there is a higher share of male business owners, regardless of disability. For instance, among the youngest age category (25 to 44 years), 71.2% of owners of unincorporated businesses are men (Chart 5A), compared with 59.6% of non-immigrant business owners (Chart 5B). Moreover, the gender distribution among immigrant business owners between the age groups (Chart 5A) is similar to that of business owners without disabilities (Chart 5C).

In terms of the type of business, there are more women business owners of incorporated businesses than of unincorporated businesses in the oldest age category, whether the business owners are immigrants or non-immigrants. For example, 38.4% of immigrant business owners aged 65 and older of incorporated businesses are women, compared with 30.1% for unincorporated businesses (Chart 5A). In addition, 40.1% of non-immigrant business owners in the same age group of incorporated businesses are women, compared with 32.2% for unincorporated businesses. For how gender and immigrant status intersect when measured as an ownership share at the firm level, please see the appendix.

The median income of business owners without disabilities is consistently higher than the median income of those with disabilities

The total personal income of each business owner can also be found in the T1PMF. The median total personal income of business owners without disabilities is consistently higher than that of business owners with disabilities (Table 4), regardless of gender. Moreover, this median income ratio is generally lower in the 45-to-64 age group. For instance, the median income of women owners with disabilities is approximately 71.0% to 74.2% of that of women business owners without disabilities. In contrast, while the median income ratio is below 1 in the oldest age group (65 years and older), it is higher than among younger age groups (younger than age 65) and ranges between 88.3% and 96.1%.

Data table for Chart 5

| With disability | ||||||

|---|---|---|---|---|---|---|

| Age group | Male | Female | Male | Female | ||

| number | ||||||

| Immigrant | 25 to 44 years | Incorporated | 220 | 107 | 67.3 | 3.3 |

| Unincorporated | 158 | 64 | 71.2 | 2.9 | ||

| 45 to 64 years | Incorporated | 609 | 347 | 63.7 | 3.6 | |

| Unincorporated | 492 | 279 | 63.8 | 3.6 | ||

| 65 years and older | Incorporated | 270 | 168 | 61.6 | 3.8 | |

| Unincorporated | 167 | 72 | 69.9 | 3.0 | ||

| Non-immigrant | 25 to 44 years | Incorporated | 1,228 | 755 | 61.9 | 3.8 |

| Unincorporated | 956 | 648 | 59.6 | 4.0 | ||

| 45 to 64 years | Incorporated | 4,034 | 3,192 | 55.8 | 4.4 | |

| Unincorporated | 3,812 | 2,270 | 62.7 | 3.7 | ||

| 65 years and older | Incorporated | 6,942 | 4,649 | 59.9 | 4.0 | |

| Unincorporated | 5,442 | 2,580 | 67.8 | 3.2 | ||

| Without disability | ||||||

|---|---|---|---|---|---|---|

| Age group | Male | Female | Male | Female | ||

| number | ||||||

| Immigrant | 25 to 44 years | Incorporated | 122,730 | 64,875 | 65.4 | 34.6 |

| Unincorporated | 75,218 | 37,589 | 66.7 | 33.3 | ||

| 45 to 64 years | Incorporated | 138,098 | 76,355 | 64.4 | 35.6 | |

| Unincorporated | 101,112 | 49,883 | 67.0 | 33.0 | ||

| 65 years and older | Incorporated | 16,554 | 8,341 | 66.5 | 33.5 | |

| Unincorporated | 10,946 | 4,363 | 71.5 | 28.5 | ||

| Non-immigrant | 25 to 44 years | Incorporated | 267,616 | 154,306 | 63.4 | 36.6 |

| Unincorporated | 179,032 | 120,492 | 59.8 | 40.2 | ||

| 45 to 64 years | Incorporated | 463,793 | 278,808 | 62.5 | 37.5 | |

| Unincorporated | 309,829 | 182,792 | 62.9 | 37.1 | ||

| 65 years and older | Incorporated | 204,466 | 114,568 | 64.1 | 35.9 | |

| Unincorporated | 151,410 | 61,415 | 71.1 | 28.9 | ||

|

Note: Excludes individuals for whom age or gender is missing. Source: Statistics Canada, Canadian Employer–Employee Dynamics Database. |

||||||

| DTC | non-DTC | DTC/non-DTC | |

|---|---|---|---|

| dollars | median | ||

| Incorporated | |||

| Age group and gender | |||

| 25 to 44 years, female | 44,181 | 54,500 | 0.81 |

| 25 to 44 years, male | 54,306 | 62,848 | 0.86 |

| 45 to 64 years, female | 43,908 | 61,832 | 0.71 |

| 45 to 64 years, male | 51,867 | 72,956 | 0.71 |

| 65 years and older, female | 58,501 | 63,436 | 0.92 |

| 65 years and older, male | 62,583 | 70,860 | 0.88 |

| Unincorporated | |||

| Age group and gender | |||

| 25 to 44 years, female | 25,415 | 36,664 | 0.69 |

| 25 to 44 years, male | 37,897 | 45,781 | 0.83 |

| 45 to 64 years, female | 30,553 | 41,181 | 0.74 |

| 45 to 64 years, male | 34,332 | 46,281 | 0.74 |

| 65 years and older, female | 42,352 | 44,487 | 0.95 |

| 65 years and older, male | 44,710 | 46,534 | 0.96 |

|

Notes: DTC = disability tax credit. Median excludes individuals with a total income of zero and individuals for whom age or gender is missing. Source: Statistics Canada, Canadian Employer–Employee Dynamics Database. |

|||

Characteristics of businesses owned by persons with disabilities

As described in the methods section, there are two ways to identify businesses owned by persons with disabilities: the first is based on whether a business has one or more owners who claim the DTC, and the second is based on the shareholders and majority ownership among persons who claim the DTC. When the former measure is applied, 1.6% of businesses are owned by persons claiming the DTC. When the latter is used, it is 0.9%. The following sections will focus on the first measure.Note

This section describes the firm-level characteristics of the businesses that are owned by persons with disabilities compared with those of businesses owned by persons without disabilities, aged 25 and older. An enterprise is included if at least one of the shareholders claimed the DTC.

A slightly higher share of incorporated businesses owned by persons with disabilities have fewer than one employee compared with businesses owned by persons without disabilities

Of the total number of businesses, 1.5% of unincorporated businesses are owned by persons with disabilities, compared with 1.7% of incorporated businesses. The firm size distribution of businesses owned by persons with and without disabilities is fairly similar, in that the majority of incorporated and unincorporated enterprises have fewer than five employees (Table 5). In unincorporated businesses, 96.8% of businesses owned by a DTC claimant are in this size category, largely because of the high proportion (89.0%) of self-employed individuals without paid help. There are more incorporated businesses in the larger size categories, and these shares are very similar across businesses owned by persons with and without disabilities. For instance, 9.0% of businesses owned by persons with disabilities have 5 to 20 employees, compared with 10.4% of businesses owned by persons without disabilities. A slightly higher share of businesses owned by persons with disabilities (64.6%) have fewer than one employee compared with businesses owned by persons without disabilities (58.5%), and this is consistent with evidence in the United Kingdom that suggests that entrepreneurs with disabilities are more likely to work alone than employ others (Jones and Latreille 2011).

| With disabilities | Without disabilities | |||

|---|---|---|---|---|

| number | share | number | share | |

| Incorporated | ||||

| Firm size | ||||

| 0 to fewer than 1 | 20,234 | 64.6 | 1,057,086 | 58.5 |

| 1 to fewer than 5 | 7,039 | 22.5 | 492,643 | 27.3 |

| 5 to fewer than 20 | 2,827 | 9.0 | 187,618 | 10.4 |

| 20 to fewer than 100 | 1,073 | 3.4 | 62,043 | 3.4 |

| 100 and over | 135 | 0.4 | 8,271 | 0.5 |

| Total | 31,308 | 100 | 1,807,661 | 100 |

| Unincorporated | ||||

| Firm size | ||||

| fewer than 1 | 15,466 | 89.0 | 1,013,336 | 89.7 |

| 1 to fewer than 5 | 1,363 | 7.8 | 87,610 | 7.8 |

| 5 to fewer than 20 | 471 | 2.7 | 25,323 | 2.2 |

| 20 to fewer than 100 | 61 | 0.4 | 2,697 | 0.2 |

| 100 and over | 24 | 0.1 | 176 | 0.00 |

| Total | 17,385 | 100 | 1,129,142 | 100 |

| Source: Statistics Canada, Canadian Employer–Employee Dynamics Database. | ||||

There are notable differences in the industry distribution of businesses owned by persons with and without disabilities

The industry distribution of businesses varies across business types (i.e., unincorporated and incorporated) and between businesses owned by persons with and without disabilities (Table 6). Among unincorporated businesses, nearly two-thirds of DTC claimant-owned businesses operate in real estate and rental and leasing (27.8%); agriculture, forestry, fishing and hunting (26.6%); and professional, scientific and technical services (10.4%). This compares with one-half of businesses not owned by DTC claimants. The share of non-DTC-claimant-owned businesses that operate in construction (10.4%) is double the share of DTC claimant-owned businesses (5.2%).

DTC claimant-owned incorporated businesses are more likely to operate in finance and insurance (14.6% compared with 9.4%) and in real estate and rental and leasing (14.6% compared with 9.9%) than non-DTC-claimant-owned businesses. In contrast, non-DTC-claimant-owned businesses (16.1%) are more likely than DTC claimant-owned businesses (12.6%) to operate in professional, scientific and technical services. Notably, the share of businesses operating in goods-producing industries is almost identical between DTC claimant-owned (22.4%) and non-DTC-claimant-owned (22.3%) businesses.

| Unincorporated | Incorporated | |||

|---|---|---|---|---|

| DTC | Non-DTC | DTC | Non-DTC | |

| Industry | share | |||

| Agriculture, forestry, fishing and hunting | 26.6 | 14.5 | 5.8 | 4.2 |

| Mining, quarrying, and oil and gas extraction | 0.2 | 0.2 | 1.2 | 0.9 |

| Utilities | 0.9 | 0.5 | 0.0 | 0.1 |

| Construction | 5.2 | 10.4 | 11.6 | 13.5 |

| Manufacturing | 1.7 | 1.9 | 3.9 | 3.6 |

| Wholesale trade | 1.0 | 1.1 | 4.2 | 4.0 |

| Retail trade | 5.0 | 5.1 | 7.0 | 7.4 |

| Transportation and warehousing | 4.1 | 7.2 | 3.9 | 6.0 |

| Information and cultural industries | 1.1 | 1.5 | 1.0 | 1.5 |

| Finance and insurance | 1.0 | 1.1 | 14.6 | 9.4 |

| Real estate and rental and leasing | 27.8 | 22.0 | 14.6 | 9.9 |

| Professional, scientific and technical services | 10.4 | 13.6 | 12.6 | 16.1 |

| Management of companies and enterprises | 0.1 | 0.1 | 1.9 | 1.7 |

| Administrative and support, waste management and remediation services | 4.1 | 5.3 | 3.7 | 4.1 |

| Educational services | 0.7 | 1.1 | 0.8 | 0.9 |

| Health care and social assistance | 2.5 | 3.8 | 5.3 | 6.8 |

| Arts, entertainment and recreation | 1.8 | 2.7 | 0.9 | 1.1 |

| Accommodation and food services | 1.4 | 1.5 | 3.5 | 4.4 |

| Other services (except public administration) | 4.3 | 6.6 | 3.7 | 4.4 |

|

Note: DTC = disability tax credit. Source: Statistics Canada, Canadian Employer–Employee Dynamics Database. |

||||

In general, financial measures such as revenue and net income tend to be higher for businesses owned by persons without disabilities

It is also possible to examine differences in financial characteristics of DTC claimant- and non-DTC-claimant-owned incorporated businesses, including revenue, assets, R&D expenditures and exports. In general, financial measures tend to be higher for non-DTC-claimant-owned businesses than for DTC claimant-owned businesses. Average net income, total assets and R&D spending are all higher for non-DTC-claimant-owned businesses, and the difference is statistically significant (Table 7). Average revenue is also higher for non-DTC-claimant-owned businesses than DTC claimant-owned businesses, but the difference is not statistically significant. Average capital cost allowance, which is a proxy for investment, is very similar between both types of businesses.

In terms of exports, DTC claimant-owned businesses are as likely as non-DTC-claimant-owned businesses to be exporters. The average value of exports is slightly higher for non-DTC-claimant-owned businesses.

| Incorporated | p-value | ||

|---|---|---|---|

| DTC claimant | Non-DTC claimant | ||

| dollars | |||

| Measure | |||

| Average revenue | 869,378 | 1,076,641 | 0.000Table 7 Note ‡ |

| Average net income | 108,971 | 161,160 | 0.000Table 7 Note ‡ |

| Average total assets | 2,103,988 | 2,298,397 | 0.777 |

| Average capital cost allowance (investment) | 26,647 | 26,945 | 0.917 |

| Average research and development spending | 1,239 | 1,926 | 0.000Table 7 Note ‡ |

| Exports | |||

| Average exports | 57,015 | 59,153 | 0.9122 |

| Number of exporters (number) | 546 | 28,730 | Note ...: not applicable |

| Share that are exporters (percent) | 1.7 | 1.5 | Note ...: not applicable |

... not applicable

Source: Statistics Canada, Canadian Employer–Employee Dynamics Database. |

|||

Conclusion

The literature describes how persons with disabilities face barriers when it comes to the labour market and business ownership. In Canada, the lack of frequent and comprehensive data on business ownership among persons with disabilities presents challenges in providing a full picture of this group, which in turn is needed to design policies to address barriers to business ownership. Using the CEEDD, this study attempts to fill this gap by examining the sociodemographic characteristics of business owners with disabilities, as well as the firm-level attributes of the businesses they own.

In terms of business ownership among persons with disabilities, this study finds that 1.3% of individuals who claim the DTC are shareholders of unincorporated businesses and 1.2% are shareholders of incorporated businesses. These business owners tend to be older than business owners who do not claim the DTC, and a slightly higher share tend to be women compared with those who do not claim the DTC, although business ownership remains male-dominated. A small proportion of business owners with disabilities are immigrants.

While the data appear robust compared with other data sources, this paper finds that about half of business owners with disabilities are aged 65 and older. As this study uses the DTC, which is more likely to be claimed by persons aged 65 and older, to identify persons with disabilities, it may be underrepresenting younger business owners with disabilities. Future work will use the Census of Population, and specifically the CSD, to capture a broader sample of the population with disabilities. Nevertheless, this study is a first step in using administrative data to provide a picture of business owners with disabilities.

Finally, this study provided a snapshot of the sociodemographics of business owners with disabilities and the firm-level characteristics of the businesses they own. It finds similarities in terms of firm size and financial characteristics compared with businesses owned by persons without disabilities, but differences in industry distribution. Future work could explore changes over time, including business growth and dynamics, and stability of business ownership among business owners with disabilities, and explore outcomes of businesses broken down further by gender and immigrant status.

Appendix

Ownership share by different subgroups

The firm-level ownership share was generated for gender and immigrant status variables where one shareholder has a disability and is aged 25 or older. As is evident from the previous demographic summaries, men have the majority ownership in unincorporated and incorporated businesses with no distinction between firms owned by individuals with and without disabilities. What is notable is that there is a greater share of enterprises with equal ownership for businesses owned by individuals with disabilities (Appendix Table A.1).

| DTC claimant | Non-DTC claimant | |||

|---|---|---|---|---|

| number | percent | number | percent | |

| Unincorporated | ||||

| Ownership type | ||||

| Equal ownership | 3,274 | 18.80 | 108,762 | 0.10 |

| Majority-owned by male | 9,238 | 53.10 | 694,994 | 0.62 |

| Majority-owned by female | 4,243 | 24.40 | 321,402 | 0.29 |

| Unclassified | 630 | 3.60 | 3,984 | 0.00 |

| Total | 17,385 | 100.00 | 1,129,142 | 1.00 |

| Incorporated | ||||

| Ownership type | ||||

| Equal ownership | 5,874 | 18.80 | 262,105 | 14.50 |

| Majority-owned by male | 15,484 | 49.50 | 1,065,664 | 59.00 |

| Majority-owned by female | 5,516 | 17.60 | 295,392 | 16.30 |

| Unclassified | 4,434 | 14.20 | 184,500 | 10.20 |

| Total | 31,308 | 100.00 | 1,807,661 | 100.00 |

| Source: Statistics Canada, Canadian Employer–Employee Dynamics Database. | ||||

Businesses with a majority of non-immigrant shareholders capture almost the entire number of enterprises that have business owners with disabilities (Appendix Table A.2). Although a similar observation can be made for businesses owned by individuals without disabilities, the difference is not as pronounced. Across all dimensions, equal ownership has the fewest businesses.

| DTC claimant | Non-DTC claimant | |||

|---|---|---|---|---|

| number | percent | number | percent | |

| Unincorporated | ||||

| Ownership type | ||||

| Equal ownership | 150 | 0.90 | 9,365 | 0.80 |

| Majority-owned by immigrants | 1,220 | 7.00 | 244,744 | 21.70 |

| Majority-owned by non-immigrants | 16,007 | 92.10 | 874,785 | 77.50 |

| Unclassified | 8 | 0.00 | 248 | 0.00 |

| Total | 17,385 | 100.00 | 1,129,142 | 100.00 |

| Incorporated | ||||

| Ownership type | ||||

| Equal ownership | 370 | 1.20 | 28,238 | 1.60 |

| Majority-owned by immigrants | 1,942 | 6.20 | 345,841 | 19.10 |

| Majority-owned by non-immigrants | 26,863 | 85.80 | 1,290,493 | 71.40 |

| Unclassified | 2,133 | 6.80 | 143,089 | 7.90 |

| Total | 31,308 | 100.00 | 1,807,661 | 100.00 |

|

Note: DTC = disability tax credit. Source: Statistics Canada, Canadian Employer–Employee Dynamics Database. |

||||

Businesses majority-owned by women immigrants represent 1.6% of all unincorporated businesses owned by persons with disabilities and 1.1% of all incorporated businesses owned by persons with disabilities (Appendix Table A.3).

| DTC claimant | Non-DTC claimant | |

|---|---|---|

| Unincorporated | ||

| Female | 277 | 63,322 |

| Male | 688 | 161,404 |

| Incorporated | ||

| Female | 351 | 68,042 |

| Male | 1,112 | 222,915 |

|

Note: DTC = disability tax credit. Source: Statistics Canada, Canadian Employer–Employee Dynamics Database. |

||

References

Arim, R. 2015. A Profile of Persons with Disabilities Among Canadians Aged 15 Years or Older, 2012. Canadian Survey on Disability. Statistics Canada Catalogue no. 89-654-X. Ottawa: Statistics Canada.

Boylan, A., and T. Burchardt. 2002. Barriers to Self-Employment for Disabled People. Report prepared for the Small Business Service. London: Small Business Service.

Chan, P.C.W., H. Liu, and R. Morissette. 2018. Canadian Employer-Employee Dynamics Database (CEEDD) User Guide – Overview. Ottawa: Statistics Canada.

Duclos, É., and R. Langlois. 2003. Disability Supports in Canada, 2001. Participation and Activity Limitation Survey. Statistics Canada Catalogue no. 89-580-X. Ottawa: Statistics Canada.

Dunstan, T. 2003. Lower Rates of Self-Reported Disability in Quebec than the Rest of Canada: An Investigation Into Some of the Factors. PALS Data Interpretation Workshop. Ottawa: Statistics Canada.

Grekou, D., W. Gu, and B. Yan. 2020. Decomposing the Between-firm Employment Earnings Dispersion in the Canadian Business Sector: The Role of Firm Characteristics. Analytical Studies Branch Research Paper Series, no. 443. Statistics Canada Catalogue no. 11F0019M. Ottawa: Statistics Canada.

Grekou, D., J. Li, and H. Liu. 2018. The Measurement of Business Ownership by Gender in the Canadian Employer-Employee Dynamics Database. Analytical Studies: Methods and References, no. 017. Statistics Canada Catalogue no. 11-633-X. Ottawa: Statistics Canada.

Huang, L. 2020. SME Profile Ownership Demographics Statistics. Innovation, Science and Economic Development Canada Catalogue no. u188-113. Ottawa: Innovation, Science and Economic Development Canada.

Jones, M. 2011. “Disability, employment and earnings: an examination of heterogeneity.” Applied Economics, 43(4), 1001-1017.

Jones, M., and P. Latreille. 2011. “Disability and self-employment: Evidence for the UK.” Applied Economics 43 (27): 4161–4178.

Kitching, J. 2014. Entrepreneurship and Self-employment by People with Disabilities. Background paper for the Organisation for Economic Co-operation and Development (OECD) Project on Inclusive Entrepreneurship. Paris: OECD Publishing.

Lechner, M., and R. Vazquez-Alvarez. 2003. The Effect of Disability on Labour Market Outcomes in Germany: Evidence from Matching. IZA Discussion Paper no. 967. Bonn: IZA Institute of Labor Economics.

Mackenzie, A. 2013. Divergent Disability Rates in Canada: Analysis of the Social Determinants of Disability. Doctoral thesis. Ottawa: Carleton University.

Morris, S., G. Fawcett, L. Brisebois, and J. Hughes. 2018. A Demographic, Employment and Income Profile of Canadian with Disabilities Aged 15 Years and Over, 2017. Statistics Canada Catalogue no. 89-654-X. Ottawa: Statistics Canada.

Renko, M., S.P. Harris, and K. Caldwell. 2015. “Entrepreneurial entry by people with disabilities.” International Small Business Journal 34 (5): 555–578.

Statistics Canada. 2020. Canadian Survey on Disability, 2017. (accessed October 26, 2021).

Wall, K. 2017. Low Income Among Persons with a Disability in Canada. Insights on Canadian Society. Statistics Canada Catalogue no. 75-006-X. Ottawa: Statistics Canada.

- Date modified: