Prices Analytical Series

An analysis of recent issues faced by the Canadian pork industry

Archived Content

Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject to the Government of Canada Web Standards and has not been altered or updated since it was archived. Please "contact us" to request a format other than those available.

Skip to text

Text begins

Introduction

Pork is a staple in the diet of many Canadians and an important component of Canadian agricultural and industrial activity. In 2018, the animal production (except aquaculture) industry supported 139,375 jobs.Note Since then, the animal production industry as a whole has seen an increase in both the job vacancy rate and the average offered hourly wage. In 2019, there were 7,700 farms reporting hogsNote . Canadian exports of live animals and animal products made up 3.1% of total Canadian exports by value in 2019. Exports of fresh and frozen pork represented 21.6% of these, and approximately 0.6% of total Canadian exports by value.

The Canadian pork market is closely tied to the U.S. pork market, and fluctuations in U.S. prices and supply are generally felt in Canada. Large deviations from U.S. prices in 2019 suggest that the African swine fever (ASF) crisis in China, coupled with mounting trade disputes between Canada and China, had a large impact on the Canadian pork market.

The past year and a half was volatile for the Canadian pork industry. The emergence of ASF in China toward the end of 2018, the imposition of a ban on Canadian pork by China in 2019 and the beginning of the COVID-19 pandemic have had observable effects on Canadian pork prices and the Canadian pork market.

The spread of ASF in China led to an increase in Canadian prices in the spring of 2019 because of an anticipated increase in Chinese imports of Canadian pork. This rise in prices was offset by a drop in the fall of 2019, caused by a sharp decrease in Canadian pork exports to China after a trade dispute led to a Chinese ban on Canadian pork. Currently, the COVID-19 pandemic continues to significantly affect food processing and manufacturing worldwide. Employee safety and physical distancing guidelines have impacted the scale of production, leading to substantial processing backlogs. Ongoing temporary plant closures have further restricted pork processing capacity and market supply.Note Note

This paper follows work published in 2014 by Statistics Canada, which examined the trends in Canadian hog and pork prices between 2012 and 2014 Note , and discusses the issues impacting the Canadian pork industry from 2018 to the present.

Major events impacting the industry

African swine fever

African swine fever (ASF) is a viral disease that originated in Africa. China reported its first case of ASF in August 2018.Note By the end of 2018, more than 1 million hogs had died as a result of the virus.Note The National Bureau of Statistics of China estimates that 2018 hog stocks were down 3% from 2017, and 2019 stocks were down 27.5% compared with 2018 stocks.Note

Reduced domestic supply in China from ASF led to an increase in imports from Canada, the United States and many other countries.Note Between the start of 2019 and the peak of Chinese demand for Canadian pork in March 2019, exports to China increased by 82.9%. Over the same period, total Canadian pork exports increased by 28.5%.

Corresponding with this rise in demand for Canadian pork, the Canadian producer priceNote of fresh and frozen pork increased by 20.8% between February and May 2019 (Chart 1). Canadian consumer prices for fresh and frozen pork show a delayed and moderated response to producer prices. Between April and July 2019, the Canadian consumer price for pork increased by 4.1%.

Data table for Chart 1

| Month | Fresh and Frozen Pork (Can, IPPI) | Hogs (Can, RMPI) | Fresh Frozen Pork (U.S., PPI) | Fresh and Frozen Pork (Can, CPI) |

|---|---|---|---|---|

| Index (2018=100) | ||||

| 2018 | ||||

| January | 100.702403 | 105.392470 | 105.515239 | 97.465519 |

| February | 99.118035 | 110.274410 | 100.798258 | 98.243546 |

| March | 94.808556 | 100.414805 | 100.145138 | 97.960627 |

| April | 96.963295 | 86.151883 | 97.532656 | 100.436166 |

| May | 99.244785 | 101.467773 | 100.798258 | 99.163032 |

| June | 102.983892 | 124.824505 | 100.725689 | 100.860545 |

| July | 105.202007 | 124.345884 | 102.685051 | 102.840976 |

| August | 97.787167 | 88.832163 | 98.548621 | 101.143463 |

| September | 97.597043 | 82.035737 | 98.693759 | 101.850760 |

| October | 103.934513 | 100.031908 | 101.161103 | 101.355652 |

| November | 102.286771 | 92.661136 | 97.677794 | 99.658140 |

| December | 99.371534 | 83.567326 | 95.718433 | 99.021573 |

| 2019 | ||||

| January | 100.639028 | 86.917677 | 97.968070 | 100.648356 |

| February | 98.801162 | 86.151883 | 96.661829 | 97.819168 |

| March | 104.378136 | 91.225271 | 89.550073 | 95.697277 |

| April | 117.179826 | 125.686024 | 99.492017 | 99.516680 |

| May | 119.397940 | 131.716656 | 107.619739 | 100.577626 |

| June | 118.827568 | 124.345884 | 111.320755 | 101.638571 |

| July | 110.398733 | 112.380345 | 105.878084 | 103.619003 |

| August | 121.299181 | 122.144225 | 108.055152 | 100.789815 |

| September | 106.786374 | 93.426930 | 108.417997 | 103.619003 |

| October | 103.934513 | 95.149968 | 107.547170 | 100.648356 |

| November | 103.934513 | 92.469687 | 108.708273 | 100.365437 |

| December | 118.257196 | 92.948309 | 113.280116 | 103.053165 |

| 2020 | ||||

| January | 115.722208 | 93.139757 | 112.554427 | 103.972651 |

| February | 100.385529 | 90.555201 | 105.950653 | 104.892137 |

| March | 101.716398 | 93.235482 | 102.249637 | 102.982435 |

| April | 112.553472 | 90.268028 | 101.741655 | 108.499352 |

| May | 147.789807 | 109.221442 | 121.843251 | 106.731109 |

|

Sources: Statistics Canada. “Consumer Price Index, monthly, not seasonally adjusted”. Table 18-10-0004-01. [Online] Statistics Canada. “Industrial product price index, by product, monthly”. Table 18-10-0030-01. [Online] Bureau of Labor Statistics. WPU02210444, Producer Price Index by Commodity for Processed Foods and Feeds: Pork, Fresh/Frozen, Unprocessed, All Cuts, Except Sausage. [Online] Statistics Canada. “Raw materials price index, monthly”. Table 18-10-0034-01. [Online] |

||||

Canada initially saw an increase in pork exports through the first part of 2019, which was driven by the increased demand from China. However, subsequent trade issues ground Canadian exports to a halt between July and November 2019 (Chart 2).

Data table for Chart 2

| Month | Canadian total | Canadian to China | U.S. total | U.S. to China |

|---|---|---|---|---|

| metric tonnes (1000s) | ||||

| 2018 | ||||

| January | 87.083720 | 21.739209 | 172.233277 | 10.660638 |

| February | 90.557583 | 25.356108 | 173.821660 | 14.757693 |

| March | 96.162303 | 23.543398 | 190.433404 | 14.802440 |

| April | 87.254571 | 23.004611 | 194.173945 | 16.144617 |

| May | 99.660240 | 25.469850 | 182.525559 | 10.324549 |

| June | 91.900929 | 23.128399 | 161.526311 | 8.424601 |

| July | 80.605991 | 15.592590 | 151.564671 | 6.581198 |

| August | 85.422195 | 19.271765 | 154.994278 | 5.724538 |

| September | 86.311227 | 19.745232 | 153.044018 | 6.071804 |

| October | 94.056572 | 24.172038 | 178.043828 | 7.008348 |

| November | 95.734492 | 28.511430 | 181.656943 | 7.372331 |

| December | 89.914826 | 27.794886 | 186.221204 | 10.677605 |

| 2019 | ||||

| January | 86.055060 | 25.518446 | 169.128857 | 8.310395 |

| February | 89.842745 | 31.352959 | 160.134729 | 10.580130 |

| March | 110.592903 | 46.661157 | 182.456014 | 14.980259 |

| April | 91.523149 | 39.245949 | 185.680251 | 17.540639 |

| May | 101.549170 | 8.346212 | 181.048662 | 20.089931 |

| June | 87.278016 | 3.396493 | 176.622430 | 24.420355 |

| July | 76.287977 | 0.654920 | 191.922613 | 38.201452 |

| August | 79.706806 | 0.033204 | 180.039529 | 33.046641 |

| September | 83.147590 | 0.345973 | 164.621996 | 23.921698 |

| October | 93.252950 | 0.310516 | 184.402035 | 33.343341 |

| November | 91.689850 | 4.904656 | 220.632978 | 55.448436 |

| December | 100.621630 | 29.861334 | 241.058424 | 78.590832 |

| 2020 | ||||

| January | 102.243451 | 40.722674 | 234.776694 | 69.881370 |

| February | 140.466841 | 47.409715 | 232.996428 | 68.130486 |

| March | 147.005018 | 58.202451 | 248.360382 | 67.387794 |

| April | 133.055394 | 61.847116 | 227.007810 | 81.597000 |

| May | 156.955892 | 59.387303 | 218.704386 | 89.654394 |

|

Sources: United States Department of Agriculture. “Livestock and Meat International Trade Data: Pork trade, 1,000 metric tons (carcass weight equivalent)”. [Online]. Available: ers.usda.gov/data-products/livestock-and-meat-international-trade-data/livestock-and-meat-international-trade-data/. Statistics Canada. “Canadian International Merchandise Trade Database. Domestic exports - Meat and edible meat offal”. Table 980-0002. [Online] |

||||

Trade issues with China

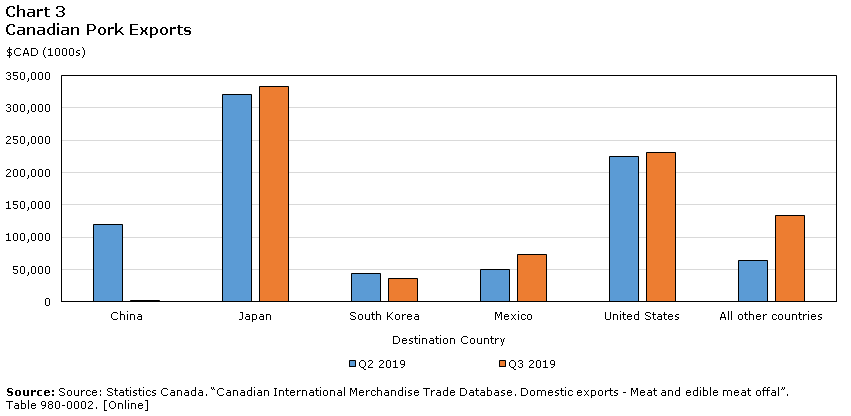

In June 2019, a shipment of Canadian pork to China was reported by Chinese officials to contain the banned feed additive ractopamine. However, the position of the Canadian government is that the export certificate was inauthentic.Note This resulted in a subsequent Chinese ban on all Canadian pork shipments. Between the second and third quarters of 2019, when the ban came into effect, total Canadian exports of fresh and frozen pork dropped by 14.9%, from approximately CAN$980 million to CAN$830 million (Chart 3). This drop in exports was driven by a 98.2% drop in exports to China. As a consequence of the Chinese ban on Canadian pork, Canada had only a 0.55% increase in total Canadian exports between 2018 and 2019. In contrast with the larger increases seen in other major pork exporting countries, this suggests that Canada did not realize gains from the bump in Chinese demand (Table 1).

Data table for Chart 3

| Destination Country | Q2 2019 | Q3 2019 |

|---|---|---|

| $CAD (1000s) | ||

| China | 119,848.863 | 2,153.686 |

| Japan | 320,886.045 | 333,197.568 |

| South Korea | 44,072.919 | 35,893.291 |

| Mexico | 50,548.161 | 72,931.504 |

| United States | 225,586.957 | 231,634.630 |

| All other countries | 63,526.612 | 133,330.754 |

| Source: Statistics Canada. “Canadian International Merchandise Trade Database. Domestic exports - Meat and edible meat offal”. Table 980-0002. [Online] | ||

The distribution of Canadian export partners changed dramatically following the ban on Canadian pork imports into China. Exports to other smaller trading partners rose over 100% between the second and third quarters of 2019, while other major trading partners, such as Japan, Mexico and the United States, all increased their imports of Canadian pork (Chart 3). Canadian pork producers offset some of their lost exports to China with increased exports to other international markets.

| Exports | 2018 | 2019 | Percent Change |

|---|---|---|---|

| European Union | 2,838 | 3,549 | 25.1 |

| United States | 2,666 | 2,867 | 7.5 |

| Canada | 1,277 | 1,284 | 0.5 |

| Brazil | 722 | 861 | 19.3 |

| China | 202 | 135 | -33.2 |

| Mexico | 177 | 234 | 32.2 |

| Japan | 4 | 3 | -25 |

| South Korea | 1 | 1 | 0 |

| Philippines | 1 | 1 | 0 |

| Other countries | 358 | 398 | 11.2 |

| Total | 8,246 | 9,335 | 13.2 |

| Source: United States Department of Agriculture. “Livestock and Poultry: World Markets and Trade”. | |||

The drop in total Canadian pork exports following the Chinese ban corresponded with a 14.3% drop in average Canadian producer pork prices between August and October 2019 (Chart 1).

After a five-month suspension of Canadian pork imports, in November 2019, the Chinese government announced that it would begin accepting Canadian exports. Between November 2019 and January 2020, Canadian pork exports to China rose 730.3%, eventually reaching higher levels than at any point in 2019. Total Canadian pork exports rose by approximately 10,000 metric tonnes, and exports to China rose by approximately 36,000 tonnes, resulting in a drop in Canadian exports to other countries. This reopening of the Chinese market allowed Canada to meet increased Chinese demand for foreign pork following losses in hog stocks as a result of ASF. Following the resurgence in Canadian exports toward the end of 2019, Canadian pork prices rose 11.3% between November 2019 and January 2020, just short of their August 2019 peak. Despite the quick recovery in Canadian pork exports and prices following the Chinese trade issues, prices fell again in February 2020. This is likely a result of the COVID-19 outbreak in China and subsequent worldwide spread.

Price gains in early and late 2019 outpaced mid-year price declines. Despite the 14.3% drop in the third quarter of 2019, pork producer prices remained higher than they were at the same time in 2018. Although farm revenue from hog sales declined between the second and third quarters of 2019, revenue was greater in the second, third and fourth quarters than in the same quarters of 2018. This contributed to an increase in total value per head for hogs in 2019.

Consumer pork prices had an average monthly movement of 0.2% through 2019 and began to rise steadily following the resurgence in the Canadian market. Although consumer prices followed the rise and fall in producer prices, the movements were much less dramatic, and consumers faced relatively small price changes.

The impact of COVID-19 on the Canadian pork industry

There was a 13.3% drop in Canadian producer prices for fresh and frozen pork between January and February 2020. There was a 12.5% drop in prices for pork sold domestically and a 14.5% drop in prices for pork sold internationally. This could have been due to a drop in international demand and subsequent oversupply. Large domestic supplies of pork in the United States would have lessened demand for imports.

Workplace guidelines on physical distancing and health and safety, including the use of personal protective equipment and limitations on worker proximity, created a hurdle for manufacturing facilities. This has likely led to a reduction in production capacity. Outbreaks of COVID-19 among employees led to sporadic closures of some large processing plants in Canada in March and April.

These closures appear to have reduced processing capacity below what was demanded by farmers and led to a supply bottleneck. Closures of processing plants contributed to higher producer pork prices, reflected by a 1.3% increase in the Industrial Product Price Index for fresh and frozen pork in March, a 10.7% increase in April, and a 31.3% increase in May.

The supply shortage of processed pork led to a 5.4% increase in consumer prices between March and April.

Between January and March, there was a 43.8% rise in total Canadian pork exports. This was followed by a 9.5% drop in total pork exports between March and April, driven by a 20.8% drop in pork exports to the United States. This suggests that COVID-19 in Canada and the United States has led to a drop in demand for Canadian pork, or a drop in the volume of pork available for export and secondary processing in the United States. This may be due in part to a drop in demand from restaurants and food services.

Exports to China have increased by 51.9% between January and April 2020, as China looks to substitute for a drop in production from ASF.

Conclusions and looking ahead

The Canadian pork industry faced a volley of issues in 2019 and the first half of 2020. The Canadian government and the pork industry have invested heavily in the protection of herds from ASF. They emerged largely unscathed, and despite a five-month suspension of Chinese imports of Canadian pork, the Canadian industry managed to redirect output. Following these trade issues, the Canadian pork industry made a quick recovery in exports and prices. Despite the variance in prices and exports over the past 18 months, Canadian exports and producer prices were at higher levels in April and May 2019 than at any point in 2018. Although it is difficult to predict how Canadian producer pork prices will move in the future, if Chinese demand remains high, it may continue to have upward pressure on Canadian prices.

The COVID-19 pandemic has hit food processing worldwide. In North America, physical distancing and health and safety measures have caused a shift in working conditions and a reduction in processing capacity across affected meat processing plants. Plant closures because of COVID-19 outbreaks tightened the processing bottleneck and may continue to have an impact on the industry should there be a second wave of closures.

Consumer prices for pork have followed the behaviour of producer prices relatively closely, but have shown more muted movement. Although Canadian consumers have seen some movement in sales prices, they are mostly insulated from the most severe shocks to the Canadian pork market.

Moving forward, it appears that COVID-19 will continue to impact the Canadian pork industry, as domestic and U.S. production is attenuated. It will be interesting to see whether the COVID-19 hotspots in manufacturing facilities continue to impact production and possibly the export of pork by Canada to the United States or elsewhere. Only time will tell whether Canadian pork prices continue their upward movement in the coming months.

- Date modified: