Prices Analytical Series

Canadian Consumers Prepare for COVID-19

Archived Content

Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject to the Government of Canada Web Standards and has not been altered or updated since it was archived. Please "contact us" to request a format other than those available.

Skip to text

Text begins

The features of the Canadian consumer environment are shifting rapidly due to the COVID-19 pandemic, shaped by a variety of interconnected and evolving factors. Restrictions on the activities of citizens and businesses and increased pressure on adapting supply chains are influencing the what, where, when and how of Canadian consumption, on an ongoing basis.

As news media provides daily coverage of shortages of non-durable goods across the country, Statistics Canada can help to shed light on the impact of COVID-19 on consumer purchasing patterns.

This study aims to analyze trends in consumer demand and sales, as Canadians stock up on grocery items and practice social distancing for an indefinite period. The information is based on transaction data for grocery products.Note

Sales increase by 38%

On March 11th, 2020 the federal government announced its COVID-19 response fund followed by a coordinated economic relief package. By the end of that same week, grocery sales had increased 38% compared to their average sales in 2019 (Chart 1). This represents 16% higher revenues than those reported in the week leading up to the December holiday, the busiest shopping week of the year. Compared to the same week in the previous year (52-week % change), sales increased by 46%.

Data table for Chart 1

| % change relative to average 2019 |

|

|---|---|

| 2019 | |

| January | |

| Week 1 | -5 |

| Week 2 | -5 |

| Week 3 | -2 |

| Week 4 | -7 |

| February | |

| Week 1 | -2 |

| Week 2 | -6 |

| Week 3 | -3 |

| Week 4 | -4 |

| March | |

| Week 1 | -3 |

| Week 2 | -5 |

| Week 3 | -6 |

| Week 4 | -4 |

| Week 5 | -4 |

| April | |

| Week 1 | -2 |

| Week 2 | -2 |

| Week 3 | 10 |

| Week 4 | -12 |

| May | |

| Week 1 | 0 |

| Week 2 | 3 |

| Week 3 | 5 |

| Week 4 | 0 |

| June | |

| Week 1 | 4 |

| Week 2 | 3 |

| Week 3 | 5 |

| Week 4 | 3 |

| Week 5 | 8 |

| July | |

| Week 1 | 3 |

| Week 2 | 1 |

| Week 3 | 3 |

| Week 4 | 1 |

| August | |

| Week 1 | 6 |

| Week 2 | -2 |

| Week 3 | -1 |

| Week 4 | -1 |

| Week 5 | 3 |

| September | |

| Week 1 | 0 |

| Week 2 | -3 |

| Week 3 | -3 |

| Week 4 | 0 |

| October | |

| Week 1 | 1 |

| Week 2 | 8 |

| Week 3 | -8 |

| Week 4 | -4 |

| November | |

| Week 1 | -1 |

| Week 2 | -2 |

| Week 3 | -4 |

| Week 4 | 0 |

| Week 5 | 2 |

| December | |

| Week 1 | 4 |

| Week 2 | 6 |

| Week 3 | 19 |

| Week 4 | 3 |

| 2020 | |

| January | |

| Week 1 | -2 |

| Week 2 | -1 |

| Week 3 | -6 |

| Week 4 | -3 |

| February | |

| Week 1Data table Note 1 | -1 |

| Week 2 | -5 |

| Week 3 | 0 |

| Week 4Data table Note 2 | -4 |

| Week 5 | 1 |

| March | |

| Week 1Data table Note 3 | 3 |

| Week 2Data table Note 4 | 38 |

Source: Consumer Prices program, special tabulation. |

|

The report highlights percent change compared to the average weekly sales in 2019. Comparisons of weekly sales to the same week in the previous year (52-week % change) are also enlightening, and reveal similar patterns. These are available in the appendix of this study. There are advantages to either approach, but considering there may have been unusual weather events or supply changes in a given week in either year, it was decided to use a yearly average in the comparison to smooth out the impact such events may have made in a short reference period.

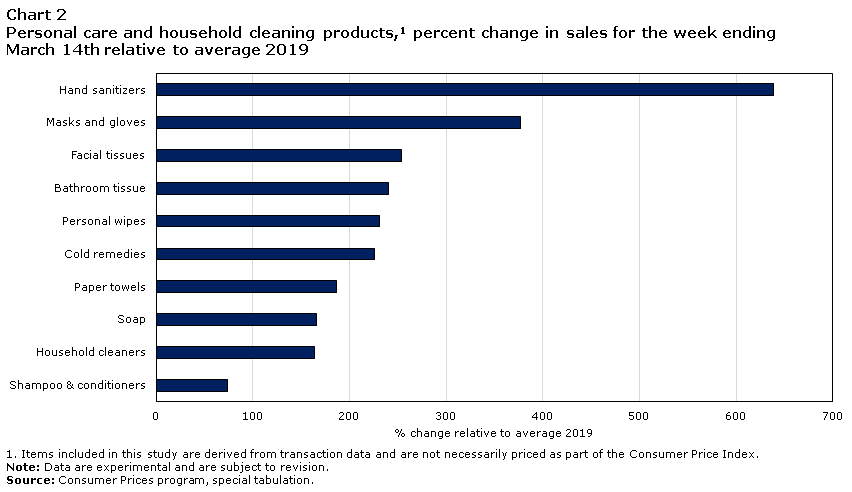

Personal care and household cleaning products sales surge

Data table for Chart 2

| Personal care and household cleaning productsData table Note 1 | % change relative to average 2019 |

|---|---|

| Hand sanitizers | 639 |

| Masks and gloves | 377 |

| Facial tissues | 253 |

| Bathroom tissue | 241 |

| Personal wipes | 231 |

| Cold remedies | 226 |

| Paper towels | 187 |

| Soap | 166 |

| Household cleaners | 164 |

| Shampoo & conditioners | 74 |

Source: Consumer Prices program, special tabulation. |

|

Hand sanitizer, and mask and glove sales provided an early indication of shifting consumer behaviour, increasing 477% and 122% respectively as early as the last week of January, and registering 639% and 377% increases respectively in the week ending March 14th compared to the 2019 average (Chart 2).

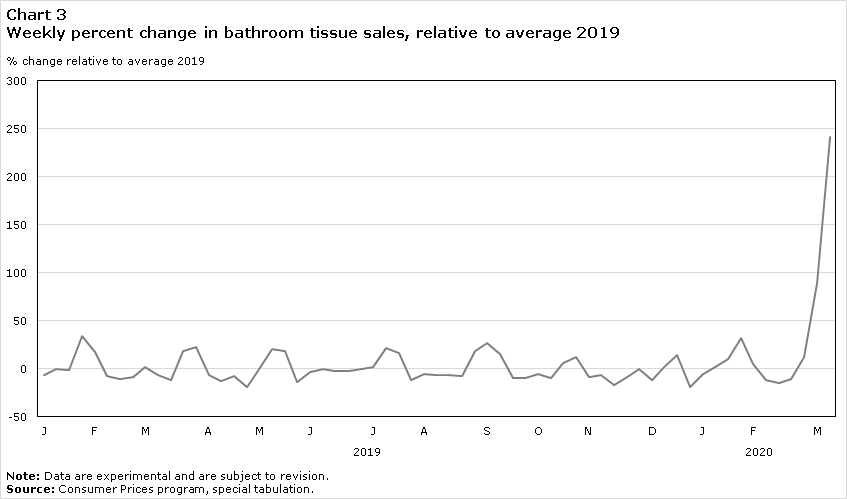

In contrast, bathroom tissue sales (Chart 3), which received extensive media coverage,Note only began to rise significantly in the first week of March shortly after Federal Health Minister Patty Hajdu advised Canadians to be prepared with a week’s worth of supplies.Note

Data table for Chart 3

| % change relative to average 2019 |

|

|---|---|

| 2019 | |

| January | |

| Week 1 | -6 |

| Week 2 | 0 |

| Week 3 | -1 |

| Week 4 | 34 |

| February | |

| Week 1 | 17 |

| Week 2 | -8 |

| Week 3 | -11 |

| Week 4 | -9 |

| March | |

| Week 1 | 2 |

| Week 2 | -6 |

| Week 3 | -12 |

| Week 4 | 19 |

| Week 5 | 23 |

| April | |

| Week 1 | -7 |

| Week 2 | -13 |

| Week 3 | -8 |

| Week 4 | -19 |

| May | |

| Week 1 | 0 |

| Week 2 | 21 |

| Week 3 | 19 |

| Week 4 | -14 |

| June | |

| Week 1 | -3 |

| Week 2 | 0 |

| Week 3 | -2 |

| Week 4 | -2 |

| Week 5 | 0 |

| July | |

| Week 1 | 2 |

| Week 2 | 22 |

| Week 3 | 16 |

| Week 4 | -12 |

| August | |

| Week 1 | -5 |

| Week 2 | -6 |

| Week 3 | -7 |

| Week 4 | -8 |

| Week 5 | 19 |

| September | |

| Week 1 | 27 |

| Week 2 | 15 |

| Week 3 | -10 |

| Week 4 | -10 |

| October | |

| Week 1 | -5 |

| Week 2 | -10 |

| Week 3 | 6 |

| Week 4 | 12 |

| November | |

| Week 1 | -9 |

| Week 2 | -7 |

| Week 3 | -17 |

| Week 4 | -9 |

| Week 5 | 0 |

| December | |

| Week 1 | -12 |

| Week 2 | 3 |

| Week 3 | 14 |

| Week 4 | -19 |

| 2020 | |

| January | |

| Week 1 | -5 |

| Week 2 | 2 |

| Week 3 | 10 |

| Week 4 | 32 |

| February | |

| Week 1 | 5 |

| Week 2 | -12 |

| Week 3 | -15 |

| Week 4 | -11 |

| Week 5 | 12 |

| March | |

| Week 1 | 89 |

| Week 2 | 241 |

|

Note: Data are experimental and are subject to revision. Source: Consumer Prices program, special tabulation. |

|

Bathroom tissue receipts reached a peak increase of 241% relative to the 2019 average in the week ending March 14th despite reassurances from government, retail industry experts and Canada’s largest producer of bathroom tissueNote that supply is plentiful.

Dry goods and shelf-stable foods surpass fresh and frozen foods

Over the past several weeks Canadians have turned to foods they can store, with retailers’ revenues for rice increasing more than 239% compared to the 2019 average in the week ending March 14th.

Data table for Chart 4

| % change relative to average 2019 | |

|---|---|

| Rice | 239 |

| Pasta | 205 |

| Canned vegetables | 180 |

| Flour | 179 |

| Canned fish, meat and seafood | 169 |

| Canned soup | 158 |

| Pasta sauce | 157 |

| Canned fruit | 111 |

| Infant formula | 103 |

| Cereal | 70 |

| Coffee | 52 |

|

Note: Data are experimental and are subject to revision. Source: Consumer Prices program, special tabulation. |

|

Pasta, canned vegetables and flour also featured prominently in Canadian shopping carts alongside canned fish, meat, seafood, soup and pasta sauce (Chart 4). While Canadian staples such as eggs, butter and bread reported increased revenues in the second week of March alongside fresh foods including potatoes and meat, the sales for these perishables increased by a substantially smaller magnitude, suggesting a consumer focus on stockpiling against uncertain conditions (Chart 5).

Data table for Chart 5

| % change relative to average 2019 | |

|---|---|

| Potatoes | 51 |

| Fresh pork | 49 |

| Fresh chicken | 47 |

| Fresh beef | 36 |

| Fresh vegetables | 31 |

| Fresh fish | 20 |

| Fresh fruit | 17 |

| Frozen vegetables | 129 |

| Frozen fruit | 117 |

| Frozen potatoes | 65 |

| Frozen fish | 55 |

| Eggs | 63 |

| Butter and margarine | 46 |

| Bread | 40 |

| Cheese | 34 |

| Milk | 29 |

|

Note: Data are experimental and are subject to revision. Source: Consumer Prices program, special tabulation. |

|

A work in progress

Over the next few weeks this study will be updated to incorporate more products of interest to the Canadian population.

Although concern has been raised about the possibility of price-gouging with new legislation being passed in Ontario on March 28th,Note retailers have made promises to Canadian consumers that they will not engage in predatory practices.Note Statistics Canada’s ongoing work informing Canadians through data products such as this index and the Consumer Price Index will help give context to uncertain economic times, and enable data users to make informed decisions.

Appendix

| Product group | % change relative to average 2019 sales | 52-week % change (same week, previous year) |

|---|---|---|

| All products sold at retailers | 38 | 46 |

| Bathroom tissue | 241 | 288 |

| Bread | 40 | 49 |

| Butter and margarine | 46 | 76 |

| Canned fish, meat and seafood | 169 | 199 |

| Canned fruit | 111 | 97 |

| Canned soup | 158 | 151 |

| Canned vegetables | 180 | 165 |

| Cereal | 70 | 75 |

| Cheese | 34 | 44 |

| Coffee | 52 | 57 |

| Cold remedies | 226 | 204 |

| Eggs | 63 | 67 |

| Facial tissues | 253 | 257 |

| Flour | 179 | 208 |

| Fresh beef | 36 | 55 |

| Fresh chicken | 47 | 50 |

| Fresh fish | 20 | 29 |

| Fresh fruit | 17 | 26 |

| Fresh pork | 49 | 61 |

| Fresh vegetables | 31 | 29 |

| Frozen fish | 55 | 51 |

| Frozen fruits | 117 | 94 |

| Frozen potatoes | 65 | 71 |

| Frozen vegetables | 129 | 120 |

| Hand sanitizers | 639 | 735 |

| Household cleaners | 164 | 180 |

| Infant formula | 103 | 121 |

| Masks and gloves | 377 | 404 |

| Milk | 29 | 31 |

| Paper towels | 187 | 227 |

| Pasta | 205 | 193 |

| Pasta sauces | 157 | 135 |

| Personal wipes | 231 | 268 |

| Potatoes | 51 | 59 |

| Rice | 239 | 284 |

| Shampoo and conditioner | 74 | 82 |

| Soap | 166 | 204 |

|

||

- Date modified: