StatCan COVID-19: Data to Insights for a Better Canada Impact of COVID-19 on non-profit organizations in Canada, fourth quarter of 2021

StatCan COVID-19: Data to Insights for a Better Canada Impact of COVID-19 on non-profit organizations in Canada, fourth quarter of 2021

Archived Content

Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject to the Government of Canada Web Standards and has not been altered or updated since it was archived. Please "contact us" to request a format other than those available.

by Stephanie Tam, Shivani Sood, and Chris Johnston

Text begins

Non-profit organizations represent a significant portion of the Canadian economy. In 2020, non-profit organizations represented 8.9% of gross domestic product (GDP) in Canada. Specifically, non-profit organizations serving households or individuals and businesses made up 2.2% of GDPNote and employed approximately 788,000 people,Note representing 4.5% of all jobs in Canada.Note While the COVID-19 pandemic had a significant impact on all aspects of the Canadian economy, non-profit organizations fared better than the economy as a whole. Despite the initial drop (-11.2%) in real GDP in the second quarter of 2020, the GDP of non-profits serving households or individuals and businesses increased 2.5% by the end of 2020.Note However, in the same year, the economy-wide real GDP shrank 5.4%, the steepest annual decline since quarterly data were first recorded in 1961.Note In 2020, employment declined 3.9% in non-profit institutions and 9.3% in non-profits serving households or individuals and businesses, compared with an 8.2% decrease for the economy as a whole. However, in the fourth quarter of 2020, as the economy opened up, employment in non-profit institutions serving households or individuals and businesses rose 3.8%.Note

From the beginning of October to early November 2021, Statistics Canada conducted the Canadian Survey on Business Conditions to collect information on the environment businesses are currently operating in and their expectations moving forward. For the purposes of the Canadian Survey on Business Conditions, non-profit organizations include non-profit institutions that serve households or individuals, and businesses, and exclude government non-profit organizations such as hospitals. Based on the results of the survey, non-profit organizations have a more positive future outlook than other businesses, although they were less likely to be able to take on more debt than their private sector counterparts. With regards to their workforce, non-profits were more likely to implement recruitment, retention and training plans, increase wages and see their workforce adopt a hybrid work environment (i.e. telework or on-site) than other organizations. This article provides insights on the expectations of non-profit organizations as well as the specific realities faced by these organizations in comparison to private sector businesses.

Non-profit organizations plan for recruitment, retention and training to address labour-related challenges

Nearly three-quarters (73.4%) of non-profit organizations indicated having specific plans over the next 12 months related to recruitment, retention and training, compared with just under three-fifths (59.4%) of private sector businesses. In particular, non-profit organizations were more likely to increase wages offered to existing (57.6%) and new (31.3%) employees, compared with private sector businesses (47.8% and 24.8% respectively). In addition, non-profit organizations were slightly more likely to plan to increase benefits offered to existing (17.8%) and new (11.2%) employees, compared with private sector businesses (15.6% and 10.5% respectively).

In terms of training, two-fifths (40.0%) of non-profit organizations plan to provide employees with paid time to engage in learning and development programs, in comparison with 14.3% of private sector businesses. Additionally, over one-third (34.2%) of non-profit organizations plan to encourage employees to participate in on-the-job training, compared with 26.6% of private sector businesses.

Data table for Chart 1

| Non-profit organizations | Private sector businesses | |

|---|---|---|

| percent | ||

| Increase wages offered to existing employees | 57.6 | 47.8 |

| Increase wages offered to new employees | 31.3 | 24.8 |

| Increase benefits offered to existing employees | 17.8 | 15.6 |

| Increase benefits offered to new employees | 11.2 | 10.5 |

| Provide employees with paid time to engage in learning and development programs | 40.0 | 14.3 |

| Encourage employees to participate in on-the-job training | 34.2 | 26.6 |

|

Note: Respondents were asked if the business or organization had various recruitment, retention and training plans in the next 12 months. Source: Canadian Survey on Business Conditions, fourth quarter of 2021 (Table 33-10-0416-01). |

||

Nearly one in six (15.4%) non-profit organizations expect their number of employees to increase over the next three months,Note while 12.8% of private sector businesses expected the same. Additionally, 21.9% of non-profit organizations expect training expenditures to increase, compared with 15.7% of private sector businesses.

| Increase | Stay about the same | Decrease | |

|---|---|---|---|

| % of businesses | |||

| Non-profit organizations | 15.4 | 76.9 | 7.7 |

| Private sector businesses | 12.8 | 77.4 | 9.8 |

|

Note: Respondents were asked from October 1 to November 5, 2021 how their number of employees and training expenditures were expected to change over the next three months. Therefore, the three month period could range from October 1, 2021 to February 5, 2022 depending on when the business or organization responded. Source: Canadian Survey on Business Conditions, fourth quarter of 2021 (Table 33-10-0399-01). |

|||

| Increase | Stay about the same | Decrease | Not applicable | |

|---|---|---|---|---|

| % of businesses | ||||

| Non-profit organizations | 21.9 | 51.1 | 4.0 | 22.9 |

| Private sector businesses | 15.7 | 50.6 | 5.2 | 28.5 |

|

Note: Respondents were asked from October 1 to November 5, 2021 how their number of employees and training expenditures were expected to change over the next three months. Therefore, the three month period could range from October 1, 2021 to February 5, 2022 depending on when the business or organization responded. Source: Canadian Survey on Business Conditions, fourth quarter of 2021 (Table 33-10-0399-01). |

||||

However, non-profit organizations were more likely to expect labour-related obstacles over the next three months. Almost two-fifths of non-profit organizations expect recruiting skilled employees (37.6%) to be an obstacle, while about than one-third expect retaining skilled employees (32.6%) to be an obstacle over the next three months. In comparison, private sector businesses were less likely to expect the same obstacles in the same time period (35.2% and 25.6% respectively).

Data table for Chart 2

| Non-profit organizations | Private sector businesses | |

|---|---|---|

| percent | ||

| Recruiting skilled employees | 37.6 | 35.2 |

| Retaining skilled employees | 32.6 | 25.6 |

|

Note: Respondents were asked if the business or organization expected various obstacles over the next three months. Source: Canadian Survey on Business Conditions, fourth quarter of 2021 (Table 33-10-0400-01). |

||

Non-profit organizations have a more positive outlook than private sector businesses in spite of a lower ability to take on more debt

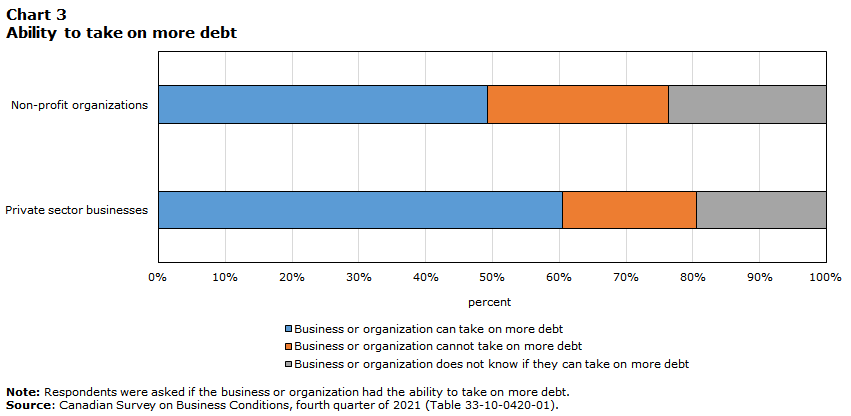

As COVID-19 restrictions were put in place, many businesses and organizations sought external financing in order to survive. As a result, some have now reached a point where they do not have the ability to take on more debt. Non-profit organizations were more likely to report this being the case.

Almost one-third (29.1%) of non-profit organizations reported that they did not have the ability to take on more debt. In contrast, less than one-fifth (18.6%) of private sector businesses reported not being able to take on more debt.

Data table for Chart 3

| Business or organization can take on more debt | Business or organization cannot take on more debt | Business or organization does not know if they can take on more debt | |

|---|---|---|---|

| percent | |||

| Non-profit organizations | 52.8 | 29.1 | 25.3 |

| Private sector businesses | 56.1 | 18.6 | 18.1 |

|

Note: Respondents were asked if the business or organization had the ability to take on more debt. Source: Canadian Survey on Business Conditions, fourth quarter of 2021 (Table 33-10-0420-01). |

|||

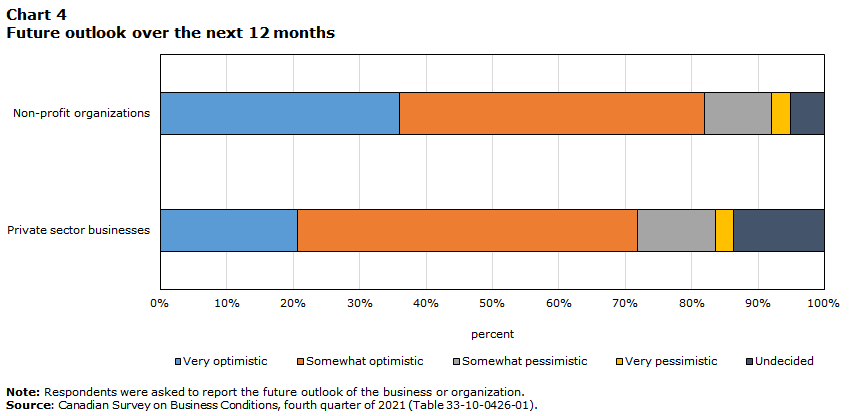

Although non-profit organizations were more likely to be unable to take on more debt, they were more likely to have an optimistic outlook in the long term, and were less likely to be uncertain of their future outlook. Over four-fifths (82.0%) of non-profit organizations reported an optimistic future outlook over the next 12 months, compared with less than three-quarters (71.8%) of private sector businesses that had the same outlook. In particular, over one-third (36.0%) of non-profit organizations had a very optimistic future outlook in comparison to one-fifth (20.7%) of private sector businesses. Meanwhile, 5.1% of non-profit organizations were uncertain of their future outlook, compared with 13.7% of private sector businesses.

Data table for Chart 4

| Very optimistic | Somewhat optimistic | Somewhat pessimistic | Very pessimistic | Undecided | |

|---|---|---|---|---|---|

| percent | |||||

| Non-profit organizations | 36.0 | 46.0 | 10.0 | 2.9 | 5.1 |

| Private sector businesses | 20.7 | 51.1 | 11.8 | 2.7 | 13.7 |

|

Note: Respondents were asked to report the future outlook of the business or organization. Source: Canadian Survey on Business Conditions, fourth quarter of 2021 (Table 33-10-0426-01). |

|||||

Non-profit organizations more likely to support hybrid work arrangements

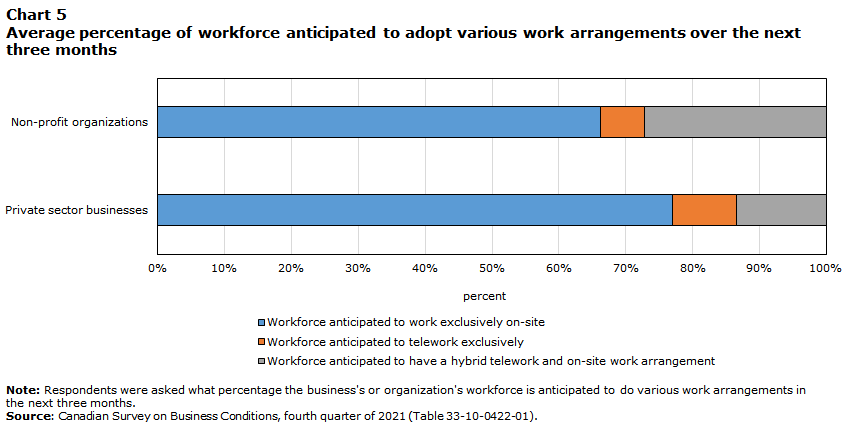

Businesses and organizations have started to rethink traditional working arrangements. From April 2020 to June 2021, 30% of employees that responded to the Labour Force Survey had performed most of their hours from home.Note When considering new teleworkers, 90% reported being at least as productive at home as they did previously in their usual place of work,Note and 80% would like to work at least half of their hours from home once the pandemic is over.Note As such, some businesses and organizations are considering the use of teleworking in the future. Non-profit organizations were more likely to anticipate having their workforce adopt a hybrid telework and on-site work arrangement in the near future.

On average, non-profit organizations anticipated that over one-quarter (27.2%) of their workforce will have a hybrid telework and on-site work arrangement over the next three months. Comparatively, private sector businesses anticipated that on average, this type of work arrangement will be about half as common (13.4%).

On the other hand, a significant number of businesses and organizations anticipate their employees to either work exclusively on-site or exclusively telework over the next three months. On average, nearly two-thirds (66.2%) of the workforce in non-profit organizations and over three-quarters (77.0%) of the workforce in private sector businesses are anticipated to work exclusively on-site in the next three months. Alternatively, on average, 6.6% of the workforce in non-profit organizations and 9.6% of the workforce in private sector businesses are anticipated to telework exclusively in the next three months.

Data table for Chart 5

| Workforce anticipated to work exclusively on-site | Workforce anticipated to telework exclusively | Workforce anticipated to have a hybrid telework and on-site work arrangement | |

|---|---|---|---|

| percent | |||

| Non-profit organizations | 66.2 | 6.6 | 27.2 |

| Private sector businesses | 77.0 | 9.6 | 13.4 |

|

Note: Respondents were asked what percentage the business's or organization's workforce is anticipated to do various work arrangements in the next three months. Source: Canadian Survey on Business Conditions, fourth quarter of 2021 (Table 33-10-0422-01). |

|||

Of those that reported that at least some of their employees were anticipated to telework exclusively over the next three months, on average, 7.1% of the workforce in non-profit organizations are anticipated to be based in a different province or territory, compared with 10.0% of the workforce in private sector businesses.

Methodology

From October 1 to November 5, 2021, representatives from businesses across Canada were invited to take part in an online questionnaire about business conditions and business expectations moving forward. The Canadian Survey on Business Conditions uses a stratified random sample of business establishments with employees classified by geography, industry sector, and size. An estimation of proportions is done using calibrated weights to calculate the population totals in the domains of interest. The total sample size for this iteration of the survey is 36,140 and results are based on responses from a total of 16,528 businesses or organizations, 1,690 of which were in non-profit organizations. Respondents self-identified as being non-profit organizations serving either households or individuals, or businesses.

References

Statistics Canada. (2021). Canadian Survey on Business Conditions, fourth quarter of 2021.

- Date modified: