StatCan COVID-19: Data to Insights for a Better Canada COVID-19 and the Beef Supply Chain: An Overview

StatCan COVID-19: Data to Insights for a Better Canada COVID-19 and the Beef Supply Chain: An Overview

Archived Content

Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject to the Government of Canada Web Standards and has not been altered or updated since it was archived. Please "contact us" to request a format other than those available.

by Tyler Patrice and Damigou Lamboni

Text begins

Correction notice

The per capita availability of beef for consumption was corrected from 18.2 kg/person to 18.1 kg/person to account for a data revision prior to publishing.

1. Synopsis

COVID-19 rattled the Canadian beef supply-chain by forcing a shutdown in many slaughterhouses and meat processing plants, pushing consumers to panic-buy beef in fear of a shortage. Consumers saw atypical increases in the prices of beef, while ranchers received lower prices for cattle sold.

The outright closure or reduced capacity at many Canadian food service establishments to comply with social distancing regulations added further stress to the already-disrupted consumption patterns. Nevertheless, the beef supply chain was able to weather the storm, but changes made during the pandemic will likely mean that businesses may not return to their pre-COVID-19 normal and that further changes are on the horizon.

2. Overview

Beef has an important place in the grocery carts of Canadians.

In 2019, beef was the type of red meat with the largest amount available for consumption per capita (18.1 kg/person).Note Note With news-media reporting on potential food shortages and of a lockdown for an unknown timespan, some consumers prepared by stockpiling food in mid-March. According to the Consumer Price Index (CPI), overall Canadian grocery retail sales rose by over one-third (+38.0%) in the second week of March compared with the average value of sales in 2019.Note To put this into perspective, this represented a 16.0% increase in grocery store revenues compared with those reported for the busiest week of the year in 2019, the week before Christmas. Fresh beef sales were up by just over one-third (+36.0%) in March compared with their average 2019 sales.Note

Canada’s slaughterhouses and meat processing plants are concentrated among a few large facilities —three of which account for over four-fifths (85.0%) of Canada’s processing capacity.Note Facilities in Canada and the United States (our main beef trading partner) were pandemic hotspots during the first partial-lockdown this spring. This led to facilities reducing their capacity in April, when one-quarter of Alberta’s coronavirus cases could be traced back to a single meat-packing plant.Note Beef exports to the United States also collapsed in April, reducing the net beef trade balance (the difference between the value of exports and imports) to just under one-quarter of what it was in April 2019. Note

This brief analysis will examine the Canadian cattle and beef supply chain (figure 1) during the early stages of the Canadian partial-lockdown period (March to June 2020), and how wholesalers’ responses to these changes influenced consumer prices.

Figure 1. Canadian beef supply chain (imports not pictured)

Description for Figure 1

This figure displays the beef supply chain step-by-step; it does not include imports. First, cattle are raised in ranches then usually sent to feedlots to gain mass, once they reach the desired size they are sent to slaughterhouses and meat processing plants. From the meat processing plants, carcasses are then either sent to merchant wholesalers, food manufacturers, or a combination of both. The resulting products are finally sold to the food-service industry, exported, or sold to retailers for consumer consumption.

Sources: Statistics Canada, Wholesale Price Report (survey number 5106), internal special tabulation.

Table 18-10-0004-01: Consumer Price Index.

Table 18-10-0034-01: Raw Materials Price Index.

Agriculture and Agri-Food Canada, Weekly red meat slaughter.

3. Supply

3.1 Ranches, feedlots, slaughterhouses and meat processing plants

The beef supply chain’s strength was tested in March when COVID-19 outbreaks shuttered two plants in Alberta, effectively halting just over two-thirds (70.0%) of Canadian beef processing and creating a backlog of livestock bound for slaughterNote With nowhere to send their cattle, animals stayed on feedlots for longer than usual, corresponding to a month-over-month live cattle and calf price decrease of 6.0% in April.Note

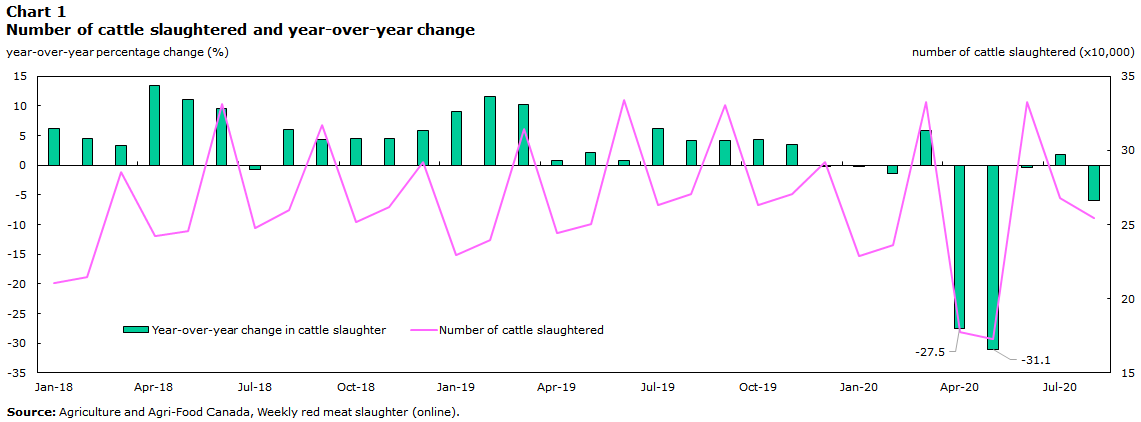

Slaughter rates were down sharply in April (-27.5%) and May (-31.1%) year over year, as shown in chart 1Note . This marked a substantial shift in the year-over-year movement for slaughter rates, which had been trending upward since January 2018. A June month-over-month spike (+92.8%) in slaughter numbers was the industry’s response to the cattle backlog. Slaughterhouses increased capacity for back to pre-pandemic levels, for the typically slower summer season, in an effort to clear the over 120,000 animal backlog estimated by the industry at that time.Note Note

Data table for Chart 1

| Period | Number of cattle slaughtered | Year-over-year change in cattle slaughter |

|---|---|---|

| x10,000 | percent | |

| 2018 | ||

| January | 21.04 | 6.2 |

| February | 21.49 | 4.5 |

| March | 28.55 | 3.2 |

| April | 24.26 | 13.4 |

| May | 24.55 | 11.1 |

| June | 33.15 | 9.6 |

| July | 24.79 | -0.8 |

| August | 25.98 | 6.0 |

| September | 31.75 | 4.4 |

| October | 25.20 | 4.5 |

| November | 26.15 | 4.6 |

| December | 29.24 | 5.9 |

| 2019 | ||

| January | 22.94 | 9.0 |

| February | 23.98 | 11.6 |

| March | 31.46 | 10.2 |

| April | 24.45 | 0.8 |

| May | 25.07 | 2.1 |

| June | 33.42 | 0.8 |

| July | 26.31 | 6.1 |

| August | 27.07 | 4.2 |

| September | 33.07 | 4.2 |

| October | 26.30 | 4.4 |

| November | 27.06 | 3.5 |

| December | 29.19 | -0.2 |

| 2020 | ||

| January | 22.89 | -0.2 |

| February | 23.65 | -1.4 |

| March | 33.28 | 5.8 |

| April | 17.73 | -27.5 |

| May | 17.27 | -31.1 |

| June | 33.28 | -0.4 |

| July | 26.78 | 1.8 |

| August | 25.45 | -6.0 |

| Source: Agriculture and Agri-Food Canada, Weekly red meat slaughter (online). | ||

3.2 Domestic supply and production

Over four-fifths (85.6%) of Canada’s total beef supply was produced domestically in 2019, while 11.8% was imported (chart 2).Note Canadian retailers are therefore mostly reliant on domestic beef supply, suggesting that the supply shortage at the start of the lockdown was mainly due to disruptions in domestic facilities.

Data table for Chart 2

| Total supply | |

|---|---|

| percent | |

| Production | 85.6 |

| Imports | 11.8 |

| Inventory | 2.7 |

| Source: Statistics Canada, Table 32-10-0053-01 : Supply and disposition of food in Canada. | |

Although most Canadian beef production serves the domestic market, suppliers had difficulty supplying the retail and food-service industries during the lockdown. As a result, certain retailers introduced per-customer limits on beef products, while some chain restaurants temporarily eliminated beef menu items.Note

3.3 Beef product wholesalers

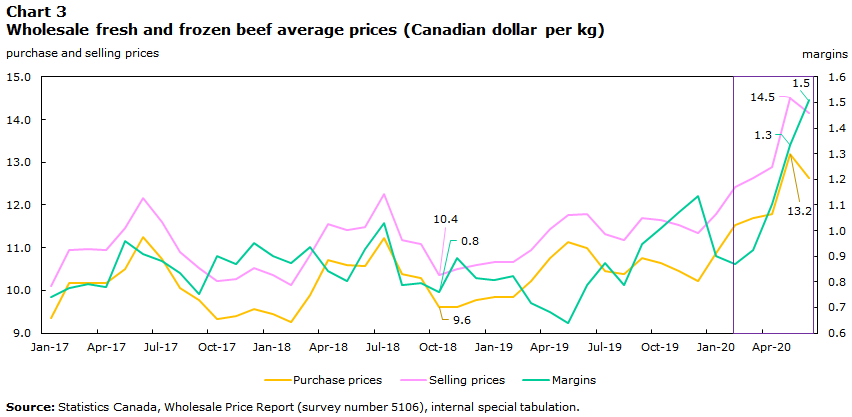

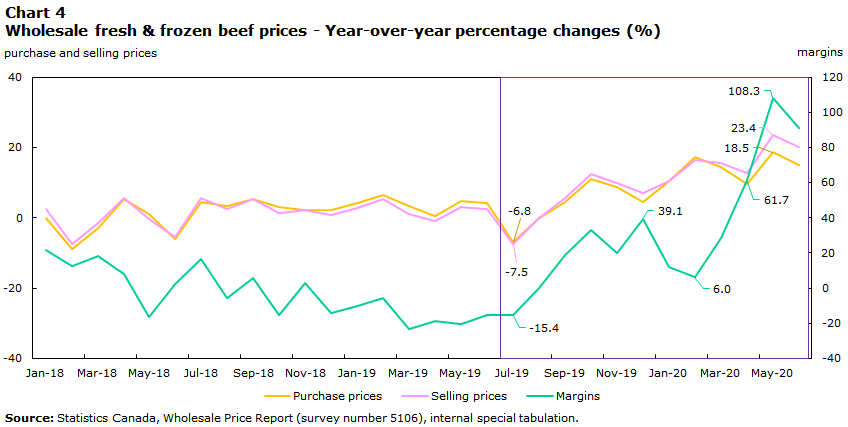

As intermediaries between the beef suppliers and retailers, wholesalers influence consumer prices. Charts 3 and 4 show average wholesale purchase, selling and margin prices (the difference between purchase and selling prices) and the year-over-year percentage changes from January 2017 to June 2020 for fresh and frozen beef products.Note Note Note

Data table for Chart 3

| Purchase prices | Selling prices | Margins | |

|---|---|---|---|

| Canadian dollar per kg | |||

| 2017 | |||

| January | 9.4 | 10.1 | 0.7 |

| February | 10.2 | 11.0 | 0.8 |

| March | 10.2 | 11.0 | 0.8 |

| April | 10.2 | 10.9 | 0.8 |

| May | 10.5 | 11.5 | 1.0 |

| June | 11.2 | 12.2 | 0.9 |

| July | 10.7 | 11.6 | 0.9 |

| August | 10.1 | 10.9 | 0.8 |

| September | 9.8 | 10.5 | 0.8 |

| October | 9.3 | 10.2 | 0.9 |

| November | 9.4 | 10.3 | 0.9 |

| December | 9.6 | 10.5 | 1.0 |

| 2018 | |||

| January | 9.5 | 10.4 | 0.9 |

| February | 9.3 | 10.1 | 0.9 |

| March | 9.9 | 10.8 | 0.9 |

| April | 10.7 | 11.5 | 0.8 |

| May | 10.6 | 11.4 | 0.8 |

| June | 10.6 | 11.5 | 0.9 |

| July | 11.2 | 12.3 | 1.0 |

| August | 10.4 | 11.2 | 0.8 |

| September | 10.3 | 11.1 | 0.8 |

| October | 9.6 | 10.4 | 0.8 |

| November | 9.6 | 10.5 | 0.9 |

| December | 9.8 | 10.6 | 0.8 |

| 2019 | |||

| January | 9.8 | 10.7 | 0.8 |

| February | 9.8 | 10.7 | 0.8 |

| March | 10.2 | 10.9 | 0.7 |

| April | 10.8 | 11.4 | 0.7 |

| May | 11.1 | 11.8 | 0.6 |

| June | 11.0 | 11.8 | 0.8 |

| July | 10.5 | 11.3 | 0.9 |

| August | 10.4 | 11.2 | 0.8 |

| September | 10.8 | 11.7 | 0.9 |

| October | 10.6 | 11.7 | 1.0 |

| November | 10.4 | 11.5 | 1.1 |

| December | 10.2 | 11.4 | 1.1 |

| 2020 | |||

| January | 10.9 | 11.8 | 0.9 |

| February | 11.5 | 12.4 | 0.9 |

| March | 11.7 | 12.6 | 0.9 |

| April | 11.8 | 12.9 | 1.1 |

| May | 13.2 | 14.5 | 1.3 |

| June | 12.6 | 14.1 | 1.5 |

| Source: Statistics Canada, Wholesale Price Report (survey number 5106), internal special tabulation. | |||

Data table for Chart 4

| Purchase prices | Selling prices | Margins | |

|---|---|---|---|

| year-over-year percentage change (percent) | |||

| 2018 | |||

| January | 0.0 | 2.6 | 21.8 |

| February | -9.0 | -7.5 | 12.3 |

| March | -2.9 | -1.4 | 18.0 |

| April | 5.3 | 5.5 | 8.1 |

| May | 1.0 | -0.4 | -16.3 |

| June | -6.1 | -5.5 | 2.2 |

| July | 4.6 | 5.5 | 16.7 |

| August | 3.2 | 2.6 | -5.6 |

| September | 5.3 | 5.3 | 5.8 |

| October | 2.9 | 1.3 | -15.6 |

| November | 2.3 | 2.3 | 2.8 |

| December | 2.2 | 0.7 | -14.5 |

| 2019 | |||

| January | 4.1 | 2.9 | -10.4 |

| February | 6.3 | 5.3 | -5.9 |

| March | 3.4 | 1.1 | -23.3 |

| April | 0.5 | -0.9 | -19.0 |

| May | 4.9 | 3.1 | -20.3 |

| June | 4.0 | 2.5 | -15.1 |

| July | -6.8 | -7.5 | -15.4 |

| August | -0.1 | -0.1 | 0.0 |

| September | 4.6 | 5.6 | 19.0 |

| October | 10.9 | 12.5 | 32.9 |

| November | 8.8 | 9.8 | 20.0 |

| December | 4.5 | 7.1 | 39.1 |

| 2020 | |||

| January | 10.5 | 10.6 | 11.7 |

| February | 17.2 | 16.3 | 6.0 |

| March | 14.5 | 15.4 | 28.5 |

| April | 9.5 | 12.6 | 61.7 |

| May | 18.5 | 23.4 | 108.3 |

| June | 15.0 | 20.1 | 91.0 |

| Source: Statistics Canada, Wholesale Price Report (survey number 5106), internal special tabulation. | |||

The drop in slaughterhouse output in April corresponded with higher purchase prices for wholesalers, who adjusted their selling prices to maintain margins. Year over year, margins over doubled (+103.8%) to reach an average price of $1.3/kg in May (Charts 3 and 4).Note Margins grew because selling prices (+23.4% to $14.5/kg) rose at a faster pace than purchase prices (+18.5% to $13.2/kg). The ability to maintain and increase margins attests to the sustained demand from retailers and food service establishments.Note

4. Demand

Due to social distancing measures, consumer spending shifted sharply away from food service towards spending on groceries for home cooking.Note This shift may explain why the Canadian agricultural sector’s shipments for processed food and its labour market activity largely outperformed most other sectors of the economy.Note

4.1 Beef product retail and consumer prices

4.1.1 Monthly beef consumer prices

CPI data show that prices for fresh and frozen beef products rose 13.7% in May–amid the supply shortage.Note This increase was followed by a second, larger month-over-month increase (+21.6%) in June.Note This was the largest month-over-month price gain in five years—likely signifying that the pandemic was the main driver for this change.Note

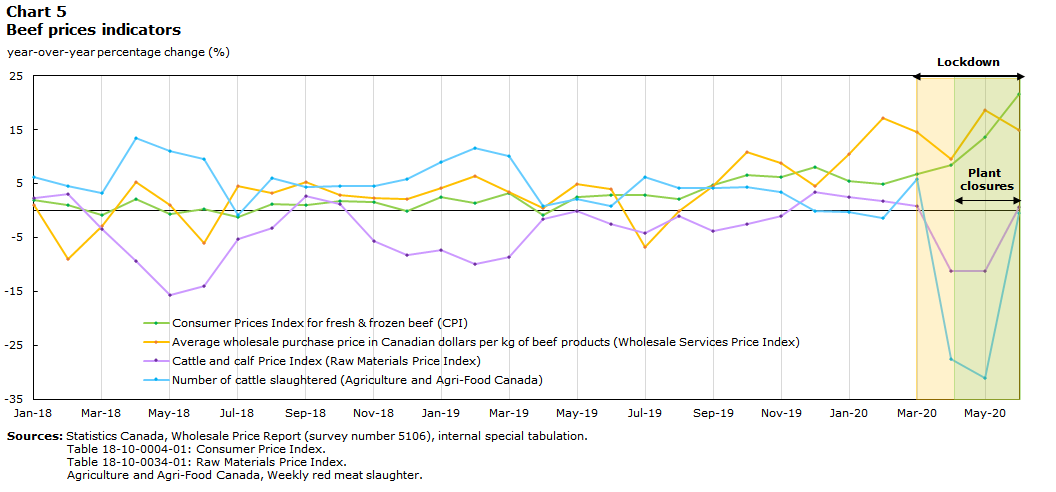

4.1.2 Beef supply chain indicators compared

Data table for Chart 5

| Date | Consumer Prices Index for fresh & frozen beef (CPI) | Average wholesale purchase price in Canadian dollars per kg of beef products (Wholesale Services Price Index) | Cattle and calf Price Index (Raw Materials Price Index) | Number of cattle slaughtered (Agriculture and Agri-Food Canada) |

|---|---|---|---|---|

| year-over-year percentage change (%) | ||||

| 2018 | ||||

| January | 2.03 | 1.06 | 2.28 | 6.16 |

| February | 0.98 | -9.03 | 3.12 | 4.45 |

| March | -0.91 | -2.90 | -3.39 | 3.24 |

| April | 2.04 | 5.34 | -9.36 | 13.37 |

| May | -0.61 | 1.01 | -15.64 | 11.09 |

| June | 0.34 | -6.07 | -14.03 | 9.62 |

| July | -1.17 | 4.59 | -5.30 | -0.77 |

| August | 1.29 | 3.25 | -3.29 | 5.96 |

| September | 1.07 | 5.27 | 2.76 | 4.39 |

| October | 1.78 | 2.95 | 1.13 | 4.48 |

| November | 1.53 | 2.26 | -5.65 | 4.55 |

| December | -0.11 | 2.16 | -8.21 | 5.88 |

| 2019 | ||||

| January | 2.50 | 4.14 | -7.27 | 9.00 |

| February | 1.36 | 6.34 | -9.97 | 11.57 |

| March | 3.26 | 3.37 | -8.69 | 10.18 |

| April | -0.78 | 0.54 | -1.59 | 0.81 |

| May | 2.53 | 4.88 | -0.13 | 2.11 |

| June | 2.90 | 4.04 | -2.46 | 0.80 |

| July | 2.87 | -6.83 | -4.25 | 6.13 |

| August | 2.04 | -0.06 | -1.02 | 4.22 |

| September | 4.73 | 4.59 | -3.84 | 4.19 |

| October | 6.62 | 10.88 | -2.52 | 4.38 |

| November | 6.25 | 8.81 | -0.96 | 3.47 |

| December | 8.07 | 4.48 | 3.47 | -0.16 |

| 2020 | ||||

| January | 5.50 | 10.48 | 2.51 | -0.22 |

| February | 4.99 | 17.19 | 1.69 | -1.36 |

| March | 6.81 | 14.53 | 0.85 | 5.80 |

| April | 8.49 | 9.45 | -11.21 | -27.49 |

| May | 13.71 | 18.55 | -11.24 | -31.12 |

| June | 21.60 | 14.99 | 0.66 | -0.42 |

|

Sources: Statistics Canada, Wholesale Price Report (survey number 5106), internal special tabulation. Table 18-10-0004-01: Consumer Price Index. Table 18-10-0034-01: Raw Materials Price Index. Agriculture and Agri-Food Canada, Weekly red meat slaughter. |

||||

The trends for cattle prices and beef supply typically influence consumer beef prices after a slight delay. The delay is due to current beef supplies being restocked with beef sourced from animals of different prices per-head and at different wholesale prices. Chart 5 highlights the potential interrelationship of the movement of cattle and beef throughout the supply chain—slaughter rates (supply) affected average cattle and calf prices, which in turn influenced wholesale purchase prices for fresh and frozen beef products. These impacted the prices that Canadians paid for beef.

The temporary shutdowns of meat processing plants in April coincided with slaughter rates dropping by over one-quarter (+27.5%) on a year-over-year basis (chart 5).Note The average price of cattle and calves (-11.2%) also declined year over year—as the ranchers that were able to sell their animals sold at a loss. This avoided raising cattle past their prime, cut losses and prevented culling, as well as created space to raise new calves.Note

Meat processing plants’ capacity reductions meant that the supply of beef decreased. This decline could partially explain why wholesalers’ purchase prices (+9.4% year over year) and consumer prices (+8.5% year over year) increased that month.Note Beef products prices were adjusted upwards with the declining stocks.

The delayed influenced of the reduced slaughter rates in April on year-over-year wholesale purchase prices (+18.5%) and consumer prices (+13.7% month over month) are seen in May, as both month-over-month and year-over-year prices increased (chart 5).Note This matches the Canadian Cattlemen’s Association assessment of beef price increases for 2020, as they noted a large price increase in May—particularly by wholesalers.Note

Beef supply decreased in May due to further drops in slaughter rates (-31.1%), which pressured animal prices downward (-11.2%).Note Note May’s drop in beef supply (which would have been sold by wholesalers and retailers the following month) could explain higher wholesale selling prices (+15.0%) and consumer prices (+21.6%) in June on a year-over-year basis.Note These price increases took place despite a recovery in slaughter rates (-0.4% year over year; +92.8% month over month) and of live cattle prices (+0.7% year over year; +6.3% month over month) that month.Note Note Since May’s beef supply is sold in June, and June’s beef supply is sold in July, the influence of June’s supply increases was not visible on that month’s wholesale and consumer prices and will likely be visible in July.

4.2 Other factors that affected beef prices during the lockdown

Some factors may have exerted upward pressure on meat prices even before the pandemic. In December 2019, food researchers at Dalhousie University and the University of Guelph suggested that climate change could increase retail prices of meat by a maximum of 6.0% in 2020, due to increases in natural disasters and erratic weather patterns.Note

The drop in the Canadian dollar at the beginning of 2020 also contributed to higher prices for meat and most other food items imported from the United States.Note When taking COVID-19 into account, this suggests that certain cuts of meat normally sold to the food service industry were being sold by retailers at a premium, and that this situation may explain why meat prices at the local level have risen 10% to 15%.Note

4.3 Beef exports

During the lockdown, cattle prices were affected by fewer exports to the United States, which receives the largest share of Canadian cattle. This was due to the increase in the number of facility shutdowns and fatal and non-fatal employee COVID-19 infections in the United States, which reduced American demand for Canadian cattle. Fewer Canadian cattle and beef exports, mainly to the United States, may also contextualize the drop in domestic cattle prices as both Canada and the United States have a highly integrated marketplace.Note

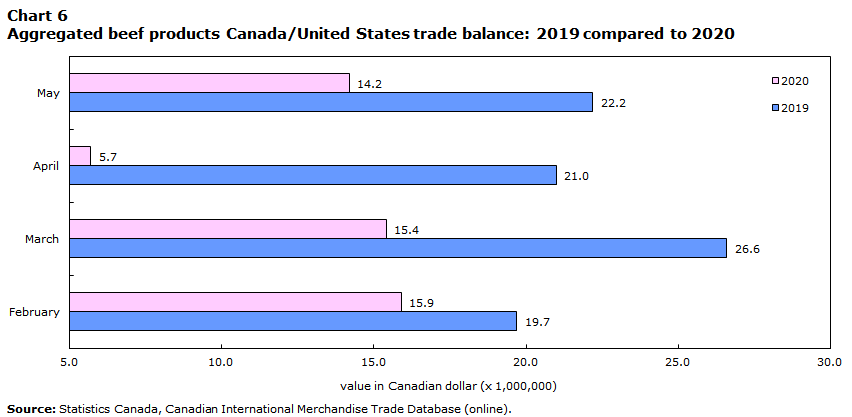

Amid a capacity-related supply shortage and lower demand, Canada’s net trade balance of beef products with the United States fell sharply in April (-63.0% month over month and -72.9% year over year) (chart 6).Note The scale of the drop was profound, in April the trade balance was 5.7 million dollars of meat products, down from 15.4 million in March and 21 million in April 2019.Note

Data table for Chart 6

| 2019 | 2020 | |

|---|---|---|

| value in Canadian dollar (x 1,000,000) | ||

| February | 19.7 | 15.9 |

| March | 26.6 | 15.4 |

| April | 21.0 | 5.7 |

| May | 22.2 | 14.2 |

| Source: Statistics Canada, Canadian International Merchandise Trade Database (online). | ||

5. 2020 and beyond

To restart their operations, meat processors had to provide personal protective equipment (PPE), retrofit their plants with equipment that allows social distancing and increase cleaning and safety measures.Note This new normal, which resulted in higher production costs, will continue into the near future.

Although Canadian slaughter facilities were near their pre-shutdown capacity in June, over 120,000 cattle were estimated to remain in backlog in Alberta alone, according to the Canadian Cattlemen’s Association.Note Note The backlog could potentially be resolved by the end of 2020.Note The increase in slaughter capacity to clear the backlog may create an oversupply and result in lower beef prices for the rest of this year. Furthermore, beef prices could also decrease due to the lower meat grade quality of the backlogged cattle, as a result of them growing too large for processing.Note

The second wave of COVID-19 in September, as well as the imposition of stricter public-health measures and the possibility of further mass-infections could further disrupt the supply chain. The beef industry may once again find itself in a period of volatility, as it did during the initial lockdown this spring.

- Date modified: