StatCan COVID-19: Data to Insights for a Better CanadaPrice trends and outlook in key Canadian housing markets

StatCan COVID-19: Data to Insights for a Better CanadaPrice trends and outlook in key Canadian housing markets

Archived Content

Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject to the Government of Canada Web Standards and has not been altered or updated since it was archived. Please "contact us" to request a format other than those available.

Correction notice

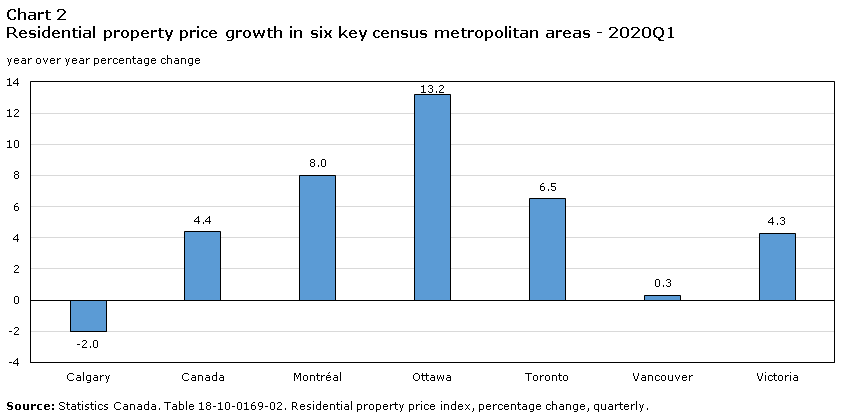

In chart 2, Calgary’s year over year percentage change was corrected from 2.0% to -2.0%.

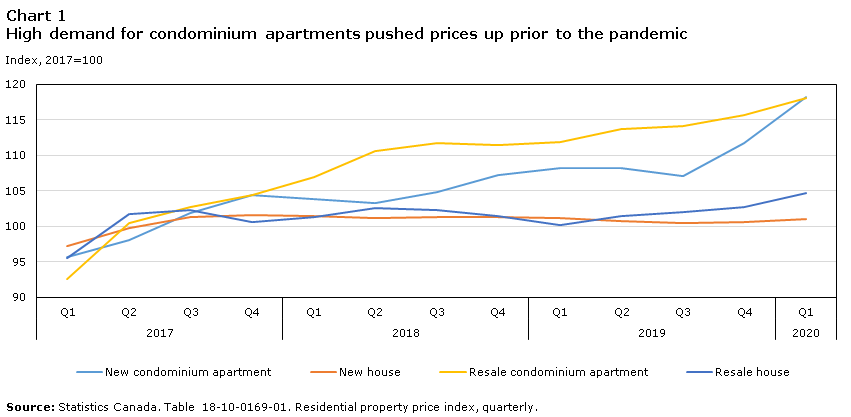

Prior to COVID-19 – More demand for high rise compared to low rise buildings

Before the pandemic, housing in most of the key markets in Canada were operating with shrinking inventories as growth in demand was outpacing supply supported by economic growth, low unemployment rate and population growth (largely due to immigration).Note

COVID-19 was declared a pandemic on March 11th and physical distancing measures were put in place on March 16th. The first quarter of data for new houses/condominiums was captured by March 14th. Since resale data are based on closing dates of a property, the resale data for 2020Q1 reflect transactions that were prior to COVID-19.

Prices for residential properties in Montréal, Ottawa, Toronto, Calgary, Vancouver, and Victoria increased by 4.4% year over year in the first quarter of 2020. Prices rose the most for the new (+9.2%) and resale (+5.5%) condominiums, with resale houses seeing a smaller increase in price (+4.6%), and prices for new houses decreasing (-0.2%).

Data table for Chart 1

| New condominium apartment | New house | Resale condominium apartment | Resale house | |

|---|---|---|---|---|

| Index, 2017=100 | ||||

| 2017 | ||||

| Q1 | 95.7 | 97.3 | 92.6 | 95.5 |

| Q2 | 98.1 | 99.7 | 100.5 | 101.7 |

| Q3 | 101.8 | 101.3 | 102.7 | 102.3 |

| Q4 | 104.4 | 101.7 | 104.4 | 100.6 |

| 2018 | ||||

| Q1 | 103.8 | 101.5 | 107.0 | 101.3 |

| Q2 | 103.4 | 101.2 | 110.7 | 102.7 |

| Q3 | 104.9 | 101.4 | 111.8 | 102.4 |

| Q4 | 107.3 | 101.4 | 111.5 | 101.4 |

| 2019 | ||||

| Q1 | 108.2 | 101.2 | 112.0 | 100.2 |

| Q2 | 108.2 | 100.8 | 113.7 | 101.4 |

| Q3 | 107.1 | 100.5 | 114.1 | 102.1 |

| Q4 | 111.7 | 100.6 | 115.7 | 102.8 |

| 2020 | ||||

| Q1 | 118.2 | 101.0 | 118.1 | 104.7 |

| Source: Statistics Canada. Table 18-10-0169-01. Residential property price index, quarterly. | ||||

Ottawa outpaced other key housing markets in Canada

Housing prices increased the most in Ottawa (+13.2%) compared to the same period last year. Although prices for both houses and condominiums increased over this period, prices for new condominiums showed the largest growth (+22.6%), followed by resale condominiums (+15.0%). This added further growth to an already hot market which took off after the foreign buyer’s tax was introduced in April 2017 in the Greater Golden Horseshoe Region (GGH).Note

Ottawa experienced an increase in population over the last year echoing a Canada-wide growth in population, mainly driven by international migration with 3.1% of recent immigrants choosing to settle in the Ottawa-Gatineau census metropolitan area between 2011 and 2016.Note

In addition to that, employment growth in both the information and technology sector as well as in the government sector have secured enough demand for housing in this rapidly growing city, putting further pressure on the housing prices as the inventory of properties has not been able to keep up with the demand.Note

Data table for Chart 2

| year over year percentage change | |

|---|---|

| Calgary | -2.0 |

| Canada | 4.4 |

| Montréal | 8.0 |

| Ottawa | 13.2 |

| Toronto | 6.5 |

| Vancouver | 0.3 |

| Victoria | 4.3 |

| Source: Statistics Canada. Table 18-10-0169-02. Residential property price index, percentage change, quarterly. | |

Prices increased the most for new and resale condominiums in Montréal, Toronto and Victoria

Residential property prices increased in Montréal, Toronto, and Victoria between 2019Q1 and 2020Q1, driven largely by increasing prices for both new and resale condominiums. All three census metropolitan areas had low vacancy rates, as well as increasing demand for condominiums from both home buyers and investors looking for rental properties.

Data table for Chart 3

| Montréal | Toronto | Victoria | |

|---|---|---|---|

| year over year percentage change | |||

| New build - houses | 7.5 | -0.5 | -0.2 |

| Resale houses | 6.8 | 5.9 | 3.5 |

| New build - condominium apartments | 8.2 | 14.6 | 13.8 |

| Resale condominium apartments | 9.8 | 8.5 | 5.7 |

| Source: Statistics Canada. Table 18-10-0169-02 . Residential property price index, percentage change, quarterly. | |||

The increase of potential buyers looking for investments outside the GGH region as well as favorable employment outlook (especially the recent growth in Montréal’s information and technology sector), allowed the city to attract more potential buyers into its housing market.

Montréal was up (+8.0%) in 2020Q1 on a year over year basis with all housing sectors showing positive year over year price increases. The largest growth occurred in the resale condominium market (+9.8%), followed by the new condominium market (+8.2%). The prices of new houses (+7.5%) and resale houses (+6.8%) all rose as well.

As one of the fastest growing cities in North America, according to the 2019 population estimates, Toronto has been seeing its demand for real estate growing for the past few years.Note In 2020Q1, Toronto continued to have a shortage of rental units which was partially addressed through secondary condo market offerings. The lack of affordable housing shifted large demographic segments to permanent rental status fueling further demand for rental units. In turn, this caused an increase in rent prices thus making new and resale condominiums very attractive for potential investors.

Toronto saw its residential prices climb (+6.5%) in 2020Q1 on a year over year basis with new condominiums rising the most (+14.6%), followed by resale condominiums (+8.5%) and resale houses (+5.9%). New house prices on the other hand actually declined (-0.5%).

Victoria’s residential prices grew (+4.3%) on an annual basis in 2020Q1 with new condominium prices rising the most (+13.8%) followed by resale condominiums (+5.7%). Victoria’s vacancy rate was on par with other high demand areas like Toronto and Montréal. The low vacancy rate has been reflected in the growth of the prices of rental units. This, combined with relatively high house prices, has resulted in condominiums apartments attracting more demand over the last few quarters.Note

Vancouver housing prices still impacted by policy measures

Vancouver saw little movement in housing prices (+0.3%) overall on a year over year basis in 2020Q1, with increasing prices for resale houses (+2.3%) and decreasing prices for new houses (-1.8%), resale condominiums (-1.4%), and new condominiums (-0.7%).

The implementation of the new mortgage lending rules in 2018, coupled with hikes in interest rates, had the effect of cooling down the housing prices in this city which was ranked as the second least affordable in the world.Note

Data table for Chart 4

| Q1 2019 | Q2 2019 | Q3 2019 | Q4 2019 | Q1 2020 | |

|---|---|---|---|---|---|

| year over year percentage change | |||||

| New build - houses | -0.5 | -1.0 | -1.6 | -2.5 | -1.8 |

| Resale houses | -6.0 | -6.4 | -7.5 | -4.4 | 2.3 |

| New build - condominium apartments | 5.0 | 5.4 | 0.4 | -1.6 | -0.7 |

| Resale condominium apartments | 0.4 | -4.3 | -5.9 | -2.2 | -1.4 |

| Source: Statistics Canada. Table 18-10-0169-02. Residential property price index, percentage change, quarterly. | |||||

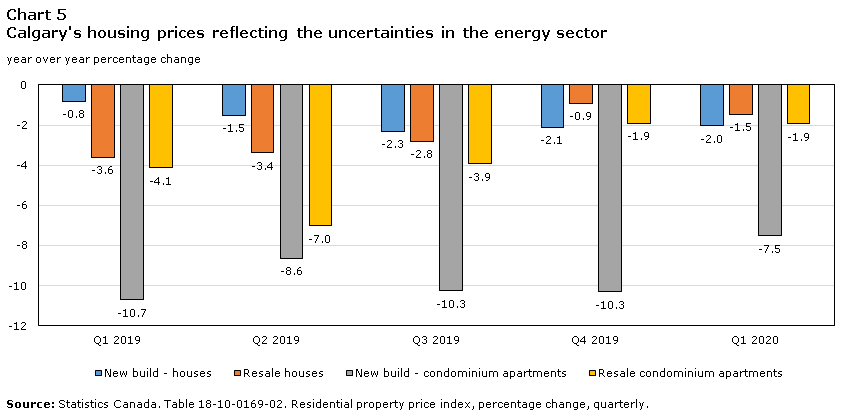

Compared to the previous year, housing prices decreased 2.0% in Calgary in 2020Q1, with prices for new condominiums declining the most (-7.5%), followed by new houses (-2.0%), resale condominiums (-1.9%) and resale houses (-1.5%). This continued the trend which began following the crash in oil prices in 2014, and reflects resulting uncertainty in the energy sector.

Data table for Chart 5

| Q1 2019 | Q2 2019 | Q3 2019 | Q4 2019 | Q1 2020 | |

|---|---|---|---|---|---|

| year over year percentage change | |||||

| New build - houses | -0.8 | -1.5 | -2.3 | -2.1 | -2.0 |

| Resale houses | -3.6 | -3.4 | -2.8 | -0.9 | -1.5 |

| New build - condominium apartments | -10.7 | -8.6 | -10.3 | -10.3 | -7.5 |

| Resale condominium apartments | -4.1 | -7.0 | -3.9 | -1.9 | -1.9 |

| Source: Statistics Canada. Table 18-10-0169-02. Residential property price index, percentage change, quarterly. | |||||

The impact of COVID-19 on the housing market after 2020Q1

In response to the pandemic, all provinces began to implement physical distancing measures in the second half of March causing most economic activity to plummet. The decline continued further into April with May seeing a glimpse of a potential but slow recovery as provinces began to open up their economies.

From late March to April, sales activities dropped by 70% on average a on year over year basis in all major real estate markets as the real estate industry adjusted to new operating conditions.Note One drastic change made by the industry was to move away from open houses to individual and virtual tours. Similarly, real estate developers provided potential buyers with the ability to have virtual tours of the properties they might be interested in. Additionally, strains on supply chains caused delays to ongoing constructions projects. Most provinces also put some new constructions projects on hold while only allowing existing projects to continue.

The demand side was affected as well but to a lesser extent. According to the Labour Force Survey, the majority of the job losses due to COVID-19 were either for part-time employment or for individuals in the younger cohort; two labour segments which are less likely to purchase real estate. Note

Physical distancing measures and travel restrictions also brought along additional negative impacts. Prior to the pandemic, there was a rise of short term rentals as an influx of investors were purchasing properties to rent on short-term rental platforms. Note However, with travel restrictions in place, many short term rental owners are now having a harder time finding clients. There is already evidence of this happening in Toronto, where the average rental prices have already began decreasing as new landlords are trying to attract clients from a diminished pool of potential renters. This has potential to further translate into falling prices for condominiums in the largest Canadian cities such as Toronto, Vancouver and Montréal.

Another impact of the COVID-19 is that commuting is going to have less impact in the choice of the location when purchasing a residential property as working from home will become more prevalent in many sectors. This may lead to potential buyers possibly spreading their search further away from pricier cities like Toronto and Vancouver to be able to afford larger houses in the suburbs. Additional space for a home office might also become an important feature of future houses, which would make larger houses a more sought after commodity.

Outlook for the six key housing markets

Given that Montréal is a major immigration hub, it is seen as having enough housing demand to sustain positive price movements for the foreseeable future. While the city’s tourism sector will undoubtedly take some time to recover, the city’s diverse economy will help dampen this negative effect.Note In addition, the Québec government enacted a full shutdown of all construction sites in April which further decreased available housing in the city. In the short term, we expect that the single home market will likely fare much better in terms of price performance. The impact may be more important on the condominium market as some investors may decide to sell their condominium units previously used as short term rentals, thus possibly pushing down the prices of this type of housing.

While economic activity was declining in most of the country, Ottawa saw a relatively low impact of COVID-19 on its employment level as the majority of the workforce are public servants, health care professionals, education as well as information and technology sector employees. This is well reflected in the new housing price movements, as Ottawa saw month-over-month increases in both May and April. Ottawa’s employment level fell by 6 percentage points in May compared to February of this year, while the rest of Canada saw a decline of 7.3 percentage points on average over the same period. Note

Given the economic stability of Ottawa, and that it has one of the highest population growth rates in the country, house prices will likely continue to rise for the foreseeable future. While it is possible to see a movement out of the city core towards suburbs as work from home becomes a new norm, tight supply will tend to keep prices growing further throughout the region.

In Toronto, the new housing price index was unchanged in April and May. Given the economic downturn, it would be likely to expect stagnation or even a decline in the Toronto housing market for higher priced properties.

Similarly to Montréal, there might be an increase in the supply of condominiums in the market given how short term rentals have lost their main sources of income when travel restrictions were put in place. Developers are also starting to focus on rental buildings, which will certainly create additional competition for individual landlords in the city.Note

Prior to the pandemic, Toronto was experiencing an exodus of middle class families to surrounding cities. This population outflow was previously overshadowed by immigration which has now decreased due to the impacts of the pandemic.Note This will likely also drive down the price of condominiums in the medium to long term.

Housing prices in Calgary continued their downward trajectory in May as the province was hit by a combination of falling oil prices and physical distancing measures. Inventory levels for both houses and condominium apartments continued to climb as sales fell more than new listings. The prices of new houses were slightly lower in May compared to March.

Calgary’s real estate market will continue to deteriorate in an environment where the inventory of homes continues to exceed the demand, due in part by overbuilding during the oil boom. As of May 2020, the employment level in Calgary declined by 7.5 percentage pointsNote compared to February 2020. The majority of the job losses occurred in the natural resources sector as well as in the manufacturing and utilities sectors. While this is less than Toronto’s decline (-8.7 percentage points), Calgary does not have the economic diversification that Toronto or Montréal have and will continue to suffer from bleak economic prospects for the foreseeable future. This will definitely contribute to the negative pressure on real estate prices.

Being a major trading hub, as well as home to many regional businesses, Vancouver is exposed to the impacts of the global economic slowdown. In April, Vancouver’s employment rate decreased by 9.4 percentage points compared to February 2020. Similarly to Toronto, Vancouver has a potential of short term rentals flooding the market and thus causing a decline in condominium prices in the short to medium term.

With the existing high cost of living in the city and the unaffordability of houses and condominium apartments, we may see a shift of preference from future home buyers who may privy properties in neighboring cities as working from home becomes more prevalent.

Victoria’s employment rate decreased by 7.1 percentage points compared to February 2020, which is almost on par with the Ottawa employment drop (-6 percentage points). Victoria’s demand for housing has been outpacing supply, especially for multifamily dwellings. Developers are building development projects in adjacent cities due to Victoria’s affordability restrictions which states that any large development has to provide 20% of units as ‘affordable’.Note Pent up demand for housing and relatively low amounts of housing inventory will likely keep prices rising in Victoria for the short term.

- Date modified: