Economic and Social Reports

The early learning and child care industry in Canada: An update to the 2021 report

DOI: https://doi.org/10.25318/36280001202600600001-eng

Text begins

Abstract

This study provides an update to a 2021 report that produced novel estimates of the business characteristics, gross domestic product (GDP) and business dynamics of child care businesses in Canada through 2016. Administrative data on all tax-filing business in Canada are used to identify incorporated businesses, typically representing child care centres, and unincorporated businesses, typically representing home-based child care businesses without employees. Because provinces and territories provide different levels of subsidies to child care businesses and only some regions have junior kindergarten, estimates derived from these data are not comparable across provinces and territories. Therefore, the study uses government ledger files to derive government subsidies and combines various data sources to estimate GDP associated with junior kindergarten and kindergarten for children aged 5 years and younger. The results show that since the 2021 report, the GDP of the child care industry grew rapidly despite a decrease in the number of child care businesses, reflecting a consolidation of the industry into larger businesses. Industry growth accelerated following the introduction of the Canada-wide Early Learning and Child Care (CWELCC) system in 2021. The introduction of this system was also associated with an increase in entry rates and a decrease in exit rates for child care businesses with employees. These findings highlight significant changes in the child care industry since the 2021 report, particularly since the implementation of the CWELCC system.

Keywords: business dynamics, child care, early learning, gross domestic product

Authors

Jenny Watt is with the Economic and Social Analysis and Modelling Division at Statistics Canada. Xingchun (Cathy) Cheng and Hong Nei (Connie) Yam are with the Public Sector Statistics Division at Statistics Canada.

Acknowledgements

This study was supported by Employment and Social Development Canada.

What is already known on this subject?

- The child care industry is comprised predominantly of small, female-owned unincorporated businesses in terms of the number of businesses, but most revenue and gross domestic product (GDP) is generated by larger, incorporated businesses—typically child care centres.

- The child care industry exhibits a high degree of turnover, with high entry and exit rates among child care businesses.

What does this study add?

- This study shows a rapid expansion in the early learning and child care industry between 2013 and 2022, but particularly after the introduction of the Canada-wide Early Learning and Child Care system in 2021.

- The child care industry has been consolidating into fewer larger businesses, reflected by a drop in the number of unincorporated businesses and an increase in the percentage of GDP generated by incorporated businesses.

- When considering only child care businesses with employees, exit rates are higher than in the business sector, and this is driven by firms with five or fewer employees.

Introduction

Despite the importance of early learning and child care (ELCC) to many Canadian families, historically little information has been available on the economic activity in the industry. Archer et al. (2021) provided novel estimates of revenue and gross domestic product (GDP) associated with the Canadian ELCC industry through 2016, and this paper provides an update of GDP through

This paper begins by using administrative business data to identify incorporated and unincorporated child care businesses, which can be used to estimate business characteristics, GDP, and firm entry and exit. However, because provinces and territories provide different levels of subsidies to child care businesses and only some regions offer junior kindergarten, GDP generated within child care businesses does not provide a complete picture of child care activity across the provinces. Therefore, this paper adds information on ELCC government transfers and expenditures using government ledger files and provides information on GDP associated with junior kindergarten and kindergarten by combining various data sources, described in the Methodology section. These additions enable the production of industry GDP estimates that are comparable across provinces. Specifically, GDP is measured at basic prices and includes child care subsidies and other direct spending on ELCC by provincial and territorial governments.

As in the 2021 report (Archer et al., 2021),the results show that the child care industry is comprised predominantly of small, female-owned unincorporated businesses. However, the number of these businesses has been in decline since 2016, while the number of incorporated businesses—typically associated with licensed child care centres—has increased year over year. While these incorporated businesses made up around 13.6% of child care businesses in 2022, they generated far more GDP than unincorporated businesses, mostly through compensation to employees. Although the data do not allow estimation of the number of child care spaces provided by each type of business, these numbers are consistent with a scenario where child care centres provided the majority of child care spaces in Canada, despite being outnumbered by home-based child care businesses. Overall, the GDP of child care businesses and child care in the education system was $23.2 billion in 2022, up from $15.2 billion in 2016.

Finally, this report departs from the 2021 report in its calculation of entry and exit rates, which are now based on businesses with employees only, consistent with Statistic Canada’s official estimates. When calculated using this approach, ELCC businesses have entry rates similar to those of all private sector businesses, but higher exit rates. The exit rate was much lower for larger businesses, those with six or more employees, than for smaller businesses, those with one to five employees.

The next section of this paper describes the data sources and how ELCC is measured. The penultimate section presents the results, followed by a final section that summarizes and discusses the strengths and weaknesses of the data.

Data and methods

Statistics Canada’s Business Register and its Canadian Employer–Employee Dynamics Database (CEEDD) are used to identify child care businesses classified under the North American Industry Classification System’s (NAICS) child day-care services industry (NAICS 624410) (Statistics Canada, 2010; Statistics Canada, 2024; Statistics Canada, 2025a). This NAICS industry includes child care centres and home child care businesses, but excludes nannies, baby-sitting services, and preschool and kindergarten programs provided through the school system. Financial variables and variables related to employees are based on tax filings. For incorporated businesses, gross operating surplus comes from the T2 Corporation Income Tax Return (T2 return), and for unincorporated businesses, mixed income come from the T1 Income Tax and Benefit Return (T1 return). Employee compensation is based on T4 Statement of Renumeration Paid (T4 slip). It is possible for unincorporated businesses to issue T4 slips, but this is very rare, and almost all compensation of employees is from incorporated businesses.

Some businesses in the CEEDD include a child care component, but their primary activity is not child care. For example, a large manufacturing plant may own and operate an on-site child care facility staffed by its employees. In such cases, financial variables such as employment and profit cannot be determined specifically for the child care component because values reported on tax forms reflect the entire business. To address this, the value the on-site child care facility (e.g., compensation to employees) is

To enable comparisons across provinces and territories, public spending on ELCC for children aged 0 to 5 years was included. In Canada, provinces and territories provide kindergarten through the public school system, but jurisdictions differ in whether care is full time or part time, and in the age at which children enter formal

The first type of public spending is government spending on ELCC before children start formal schooling. These estimates are derived from government ledger files available at Statistics Canada and include subsidies transferred to child care businesses and direct spending by provincial and territorial governments on ELCC. A challenge with these data is that provinces and territories do not report their expenses in a systematically comparable way, so the estimates must be constructed by manually reviewing spending descriptions in each provincial and territorial ledger. While every effort was made to extract government spending related to ELCC for children aged 0 to 5, some programs included serve children up to age 12, and some ELCC expenditures may be grouped with other programs and therefore not captured. Finally, the amounts include overhead costs, such as administrative costs associated with running government departments and delivering programs.

The second type of public spending is spending on junior kindergarten and kindergarten, derived from publicly available information. GDP related to schooling comes from Statistic Canada’s provincial and territorial economic accounts (Statistics Canada, 2025c). Because these GDP estimates provide the total amount for all grades of elementary and secondary school, values for children aged 5 and younger are imputed. The imputation is performed at the provincial and territorial level by multiplying the GDP totals by the proportion of children in the education system who are 5 years or younger then multiplying the result by the proportion of children in full-time schooling. These proportions are derived from publicly available annual reports from the ministries responsible for education in each province and territory.

Results

Results are presented in three sections. The first section covers business characteristics, the second presents GDP estimates and the third reports business dynamics measures (entry and exit).

Unincorporated and incorporated businesses are included in these results. Incorporated businesses comprise for-profit institutions, not-for-profit institutions and charities. Not-for-profit institutions are incorporated businesses that follow specific rules for managing their earnings and reporting to the Canada Revenue Agency (CRA) (Department of Justice Canada, 2025), but they provide similar information as for-profit businesses and are well reflected in the data. Charities operate exclusively for charitable purposes, and registration as a charity must be approved by the CRA. Although most charities do not complete the same tax forms as for-profit businesses and not-for-profit institutions, and thus financial variables such as revenue and gross operating surplus are largely missing, they are included in the CEEDD. Consequently, charities are accurately reflected in business counts and in compensation to employees, which is based on the T4 slips issued by the charities.

This limitation is behind the decision to no longer produce revenue estimates, which were included in the 2021 report. Following 2016—the last year of data in the 2021 report—a small number of large child care businesses obtained charitable status. This change resulted in a drop in estimated revenues but had a minimal effect on GDP estimates, which are mostly driven by employee compensation. Therefore, the current report produces only GDP and not revenue.

Business characteristics

The overall number of child care businesses steadily decreased from 114,254 to 78,465, largely because of a decrease in the number of unincorporated businesses (Table 1). This decline in unincorporated businesses accelerated in 2020, coinciding with the first year of the COVID-19 pandemic (Wise, 2023). During the pandemic, the child care sector experienced frequent closures because of outbreaks, and some parents withdrew their children from care (Hacioglu et al., 2024). However, the number of incorporated businesses did not decline during the pandemic period (2020 and 2021), suggesting that unincorporated businesses, which mostly correspond to home-based child care businesses, were less able to weather the disruptions caused by the COVID-19 pandemic.

In terms of other business characteristics, results are similar to those in the 2021 report: the industry was composed mostly of women-owned businesses with no employees (Table 1). However, the number of these businesses decreased over the study period, while larger, incorporated businesses increased. Specifically, incorporated businesses accounted for 7.5% of businesses in 2013 and 13.6% in 2022. The number of businesses with no employees or 1 to 5 employees declined, while those with 6 to 20 or more than 20 employees increased. The proportion of businesses with at least 76% women employees remained steady at around 90% over the study period. The decline occurred across all provinces and territories.

| 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | |

|---|---|---|---|---|---|---|---|---|---|---|

| number of businesses | ||||||||||

|

||||||||||

| Total | 114,254 | 113,328 | 110,309 | 104,046 | 98,840 | 94,565 | 95,807 | 85,926 | 77,774 | 78,465 |

| Gender | ||||||||||

| Men owned | 16,555 | 16,204 | 15,506 | 14,305 | 13,297 | 13,140 | 13,629 | 12,265 | 11,875 | 12,788 |

| Women owned | 95,714 | 95,154 | 92,827 | 87,889 | 83,645 | 79,498 | 80,161 | 71,781 | 64,080 | 63,746 |

| Equal ownership | 1,675 | 1,643 | 1,636 | 1,491 | 1,498 | 1,474 | 1,520 | 1,386 | 1,321 | 1,386 |

| Unable to assign | 310 | 327 | 340 | 361 | 400 | 453 | 497 | 494 | 498 | 545 |

| Legal status | ||||||||||

| Incorporated | 8,613 | 8,838 | 8,997 | 9,251 | 9,386 | 9,884 | 10,060 | 10,064 | 10,243 | 10,665 |

| Unincorporated | 105,641 | 104,490 | 101,312 | 94,795 | 89,454 | 84,681 | 85,747 | 75,862 | 67,531 | 67,800 |

| Size (employment) | 114,254 | 113,328 | 110,309 | 104,046 | 98,840 | 94,565 | 95,807 | 85,926 | 77,774 | 78,465 |

| 0 or undetermined | 104,091 | 103,141 | 100,119 | 93,882 | 88,626 | 84,149 | 85,484 | 75,889 | 67,613 | 67,904 |

| 1 to 5 | 4,770 | 4,611 | 4,475 | 4,273 | 4,176 | 4,156 | 3,878 | 3,587 | 3,436 | 3,397 |

| 6 to 20 | 3,528 | 3,696 | 3,774 | 3,888 | 3,971 | 3,932 | 4,158 | 4,235 | 4,282 | 4,386 |

| More than 20 | 1,865 | 1,880 | 1,941 | 2,003 | 2,067 | 2,328 | 2,287 | 2,215 | 2,443 | 2,778 |

| Labour composition Table 1 Note 1 | ||||||||||

| 0% to 25% women | 10,120 | 9,674 | 8,940 | 7,611 | 6,617 | 6,212 | 6,613 | 5,321 | 4,818 | 5,458 |

| 26% to 50% women | 1,512 | 1,474 | 1,454 | 1,283 | 1,266 | 1,187 | 1,239 | 1,134 | 1,074 | 1,127 |

| 51% to 75% women | 527 | 524 | 497 | 479 | 450 | 476 | 457 | 450 | 429 | 459 |

| 76% to 100% women | 101,392 | 100,980 | 98,743 | 93,951 | 89,839 | 85,916 | 86,607 | 78,091 | 70,640 | 70,630 |

| Geography Table 1 Note 2 | ||||||||||

| Newfoundland and Labrador | 947 | 962 | 971 | 965 | 897 | 842 | 807 | 746 | 653 | 588 |

| Prince Edward Island | 346 | 357 | 342 | 351 | 335 | 334 | 298 | 285 | 251 | 219 |

| Nova Scotia | 1,818 | 1,770 | 1,759 | 1,744 | 1,671 | 1,613 | 1,639 | 1,479 | 1,304 | 1,251 |

| New Brunswick | 1,843 | 1,849 | 1,778 | 1,681 | 1,630 | 1,543 | 1,443 | 1,336 | 1,207 | 1,155 |

| Quebec | 36,809 | 36,933 | 36,293 | 34,985 | 33,547 | 32,264 | 30,409 | 27,258 | 25,427 | 25,113 |

| Ontario | 43,314 | 42,098 | 39,914 | 35,933 | 32,931 | 31,007 | 33,851 | 29,767 | 26,208 | 27,514 |

| Manitoba | 2,799 | 2,762 | 2,726 | 2,640 | 2,649 | 2,636 | 2,539 | 2,292 | 2,135 | 2,149 |

| Saskatchewan | 3,302 | 3,277 | 3,216 | 3,267 | 3,252 | 3,073 | 3,021 | 2,863 | 2,668 | 2,542 |

| Alberta | 11,023 | 11,473 | 11,783 | 11,667 | 11,691 | 11,488 | 11,748 | 11,048 | 10,075 | 9,930 |

| British Columbia | 11,829 | 11,619 | 11,301 | 10,613 | 10,032 | 9,561 | 9,848 | 8,635 | 7,644 | 7,827 |

| Yukon | 73 | 68 | 75 | 63 | 70 | 70 | 73 | 75 | 67 | 63 |

| Northwest Territories | 94 | 96 | 96 | 85 | 82 | 83 | 83 | 79 | 69 | 61 |

| Nunavut | 36 | 42 | 39 | 41 | 39 | 35 | 35 | 36 | 36 | 34 |

Gross domestic product

GDP measures the value added created by production activities within an economy and can be measured in three

To measure income-based GDP from administrative files, different approaches are required for incorporated and unincorporated businesses. For incorporated businesses, compensation of employees and gross operating surplus represent remuneration to labour and capital from production, respectively. These values can be measured from T2 returns and are reported in Table 2. For unincorporated businesses, the T1 returns do not distinguish between the entrepreneur’s labour income and the payment to their capital. In this case, the combined value of operating surplus and compensation of employees is known as mixed income and is shown in Table 2. Together, these values constitute a measure of GDP at factor cost. Subsidies, derived from government ledger files, are added at factor cost to calculate the GDP at basic prices.

Overall, GDP at factor cost increased over the entire study period, except in 2020 when it temporarily dipped (Table 2). This coincides with the first year of the global COVID-19 pandemic (Wise, 2023). Examining the GDP components at factor cost, compensation of employees followed the same pattern as overall GDP at factor cost, dipping in 2020, but recovering in 2021 to the highest level observed during the study period. Compensation of employees drove the growth in GDP at factor cost, increasing from $3.0 billion in 2013 to $5.9 billion in 2022. Because these figures represent economy-wide totals, they are affected by changes in wages and changes in the number of hours worked by employees. Unfortunately, the data do not contain information on wages or hours worked. As a result, it is unclear how much of the growth is explained by changes in wages or changes in the size of the ELCC workforce.

Unlike compensation to employees, corporate gross operating surplus (from T2 returns) (i.e., profits on services) increased in 2020. This suggests that the expenses of incorporated child care businesses fell by more than their revenues. In contrast, unincorporated mixed income (from T1 returns) trended downward over the study period, consistent with the decline in the number of unincorporated child care businesses over time.

| 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | |

|---|---|---|---|---|---|---|---|---|---|---|

| millions of dollars | ||||||||||

| Notes: GDP = gross domestic product. ELCC = early learning and child care.

Sources: Statistics Canada, Canadian Employer–Employee Dynamics Database; government ledger files; and table 36-10-0711-01 Gross domestic product (GDP) at basic prices, by industry, provinces and territories (x 1,000,000). |

||||||||||

| Corporate compensation of employees (T2 Corporation Income Tax Return) | 3,027 | 3,195 | 3,411 | 3,660 | 3,860 | 4,293 | 4,559 | 4,136 | 4,980 | 5,871 |

| Corporate gross operating surplus (T2 Corporation Income Tax Return) | 142 | 130 | 140 | 241 | 224 | 262 | 285 | 435 | 381 | 410 |

| Unincorporated mixed income (T1 Income Tax and Benefit Return) | 1,165 | 1,160 | 1,143 | 1,110 | 1,085 | 1,080 | 1,090 | 809 | 929 | 1,039 |

| GDP at factor cost | 4,334 | 4,486 | 4,694 | 5,010 | 5,169 | 5,635 | 5,935 | 5,380 | 6,290 | 7,321 |

| Plus: Government transfers and expenditures on ELCC predominantly provided to businesses | 5,369 | 5,218 | 4,694 | 4,525 | 5,041 | 5,635 | 6,076 | 6,593 | 6,892 | 8,971 |

| Subtotal for directly measured GDP at basic prices | 9,703 | 9,705 | 9,387 | 9,535 | 10,210 | 11,271 | 12,011 | 11,973 | 13,182 | 16,293 |

| Plus: Imputation for non-childcare enterprises with childcare locations | 67 | 71 | 77 | 88 | 54 | 72 | 73 | 88 | 120 | 151 |

| Plus: Imputation for kindergarten and junior kindergarten | 4,806 | 5,253 | 5,373 | 5,556 | 5,702 | 5,921 | 6,226 | 5,999 | 6,484 | 6,730 |

| ELCC GDP at basic prices | 14,576 | 15,028 | 14,837 | 15,179 | 15,966 | 17,263 | 18,310 | 18,060 | 19,786 | 23,174 |

Government transfers and expenditures on ELCC increased from $5.4 billion in 2013 to $9.0 billion in 2022. As in the 2021 report, the growth of government spending was somewhat higher than the growth in GDP at factor cost (generated within child care businesses through employee compensation, gross operating surplus and mixed income). However, caution is needed when comparing GDP at factor cost to GDP from government transfers and expenditures. In the case of the child care industry, GDP from government transfers and expenditures includes subsidies to child care businesses, meaning that increases in GDP associated with government transfers and expenditures can reflect increases in child care business activity. Both GDP at factor cost and GDP from government transfers and expenditures increased substantially in 2021 and 2022, coinciding with the implementation of the CWELCC system.

Across the provinces and territories, the largest GDP values were in Quebec and Ontario, while the smallest expenditures were in the territories (Table 3). While these values are affected by population size, they are not completely proportional to population estimates (Statistics Canada, 2026). To examine GDP further, Table 4 shows provincial and territorial GDP by the number of children aged 0 to 5 in the respective province or territory.

| 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | |

|---|---|---|---|---|---|---|---|---|---|---|

| millions of dollars | ||||||||||

| Sources: Statistics Canada, Canadian Employer–Employee Dynamics Database; government ledger files; and table 36-10-0711-01 Gross domestic product (GDP) at basic prices, by industry, provinces and territories (x 1,000,000). | ||||||||||

| Canada | 14,575 | 15,028 | 14,837 | 15,181 | 15,967 | 17,263 | 18,309 | 18,059 | 19,788 | 23,173 |

| Newfoundland and Labrador | 95 | 102 | 103 | 100 | 100 | 120 | 130 | 132 | 148 | 178 |

| Prince Edward Island | 36 | 38 | 39 | 42 | 43 | 50 | 57 | 64 | 81 | 104 |

| Nova Scotia | 160 | 160 | 164 | 169 | 178 | 196 | 280 | 301 | 336 | 456 |

| New Brunswick | 174 | 184 | 188 | 202 | 213 | 233 | 259 | 281 | 298 | 386 |

| Quebec | 5,378 | 5,566 | 5,650 | 5,708 | 5,815 | 6,101 | 6,370 | 6,445 | 6,910 | 7,676 |

| Ontario | 6,206 | 6,392 | 6,049 | 6,219 | 6,513 | 6,977 | 7,205 | 6,711 | 7,342 | 8,519 |

| Manitoba | 380 | 394 | 413 | 443 | 454 | 461 | 510 | 475 | 554 | 656 |

| Saskatchewan | 251 | 264 | 270 | 287 | 302 | 314 | 327 | 327 | 406 | 524 |

| Alberta | 830 | 888 | 876 | 867 | 1,135 | 1,331 | 1,405 | 1,285 | 1,492 | 2,028 |

| British Columbia | 1,010 | 984 | 1,028 | 1,083 | 1,144 | 1,404 | 1,689 | 1,961 | 2,123 | 2,537 |

| Yukon | 20 | 20 | 21 | 22 | 24 | 27 | 28 | 28 | 45 | 52 |

| Northwest Territories | 21 | 22 | 23 | 23 | 28 | 32 | 32 | 32 | 35 | 34 |

| Nunavut | 14 | 14 | 15 | 16 | 16 | 17 | 18 | 18 | 20 | 22 |

The highest GDP per child aged 0 to 5 was in Quebec, Ontario, Yukon and the Northwest Territories (Table 4). These numbers reflect differences in child care provisions and spending on formal schooling. Because of its universal child care program, Quebec has had higher child care use than other provinces (Sinha, 2014; Findlay and Wei, 2021; Statistics Canada, 2021; Zhang et al., 2021), and higher spending in Ontario may be explained by the presence of full-day junior kindergarten (Macdonald, 2025). Similarly, Nova Scotia’s GDP per child aged 0 to 5 increased in 2019 when full-day junior kindergarten was introduced.

Over the study period, GDP per child aged 0 to 5 in Yukon and the Northwest Territories was higher than the Canadian average; however, this comparison should be interpreted with caution, as no adjustment is made for differences in prices between the north and the south (Table 4). Although a child care-specific estimate is not available, existing research shows that service prices are higher in Yukon and the Northwest Territories, and that public services such as education are more costly to provide because of relatively higher wages for workers providing the services (Landry et al., 2025). The relatively low value per child in Nunavut may reflect differences in institutional structures, such as the use of informal child care arrangements within families or the provision of ELCC incorporated into cultural learning.

| 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | |

|---|---|---|---|---|---|---|---|---|---|---|

| dollars | ||||||||||

| Source: Statistics Canada, Canadian Employer–Employee Dynamics Database; government ledger files; and table 36-10-0711-01 Gross domestic product (GDP) at basic prices, by industry, provinces and territories (x 1,000,000). | ||||||||||

| Canada | 6,290 | 6,468 | 6,381 | 6,495 | 6,783 | 7,312 | 7,757 | 7,683 | 8,539 | 10,052 |

| Newfoundland and Labrador | 3,259 | 3,532 | 3,631 | 3,591 | 3,603 | 4,431 | 5,000 | 5,231 | 6,057 | 7,346 |

| Prince Edward Island | 4,127 | 4,350 | 4,520 | 4,821 | 4,851 | 5,530 | 6,350 | 7,223 | 9,257 | 11,692 |

| Nova Scotia | 3,658 | 3,701 | 3,858 | 3,999 | 3,425 | 3,760 | 5,340 | 5,750 | 6,525 | 8,778 |

| New Brunswick | 3,288 | 3,516 | 3,631 | 3,912 | 5,041 | 5,533 | 6,180 | 6,785 | 7,260 | 9,348 |

| Quebec | 10,079 | 10,405 | 10,608 | 10,729 | 10,919 | 11,427 | 11,978 | 12,194 | 13,310 | 14,804 |

| Ontario | 7,146 | 7,391 | 7,016 | 7,181 | 7,449 | 7,927 | 8,144 | 7,575 | 8,379 | 9,765 |

| Manitoba | 3,918 | 4,010 | 4,148 | 4,368 | 4,426 | 4,472 | 4,938 | 4,612 | 5,435 | 6,517 |

| Saskatchewan | 2,862 | 2,967 | 3,005 | 3,151 | 3,286 | 3,408 | 3,579 | 3,639 | 4,622 | 6,061 |

| Alberta | 2,636 | 2,763 | 2,689 | 2,642 | 3,438 | 4,039 | 4,275 | 3,950 | 4,695 | 6,459 |

| British Columbia | 3,746 | 3,638 | 3,771 | 3,920 | 4,089 | 5,018 | 6,044 | 7,040 | 7,666 | 9,218 |

| Yukon | 8,087 | 7,813 | 7,844 | 8,119 | 8,968 | 9,744 | 10,117 | 10,210 | 15,999 | 19,162 |

| Northwest Territories | 5,366 | 5,966 | 5,910 | 5,930 | 7,417 | 8,522 | 8,600 | 8,811 | 9,665 | 9,797 |

| Nunavut | 2,710 | 2,762 | 2,824 | 3,032 | 3,115 | 3,145 | 3,327 | 3,394 | 3,612 | 3,987 |

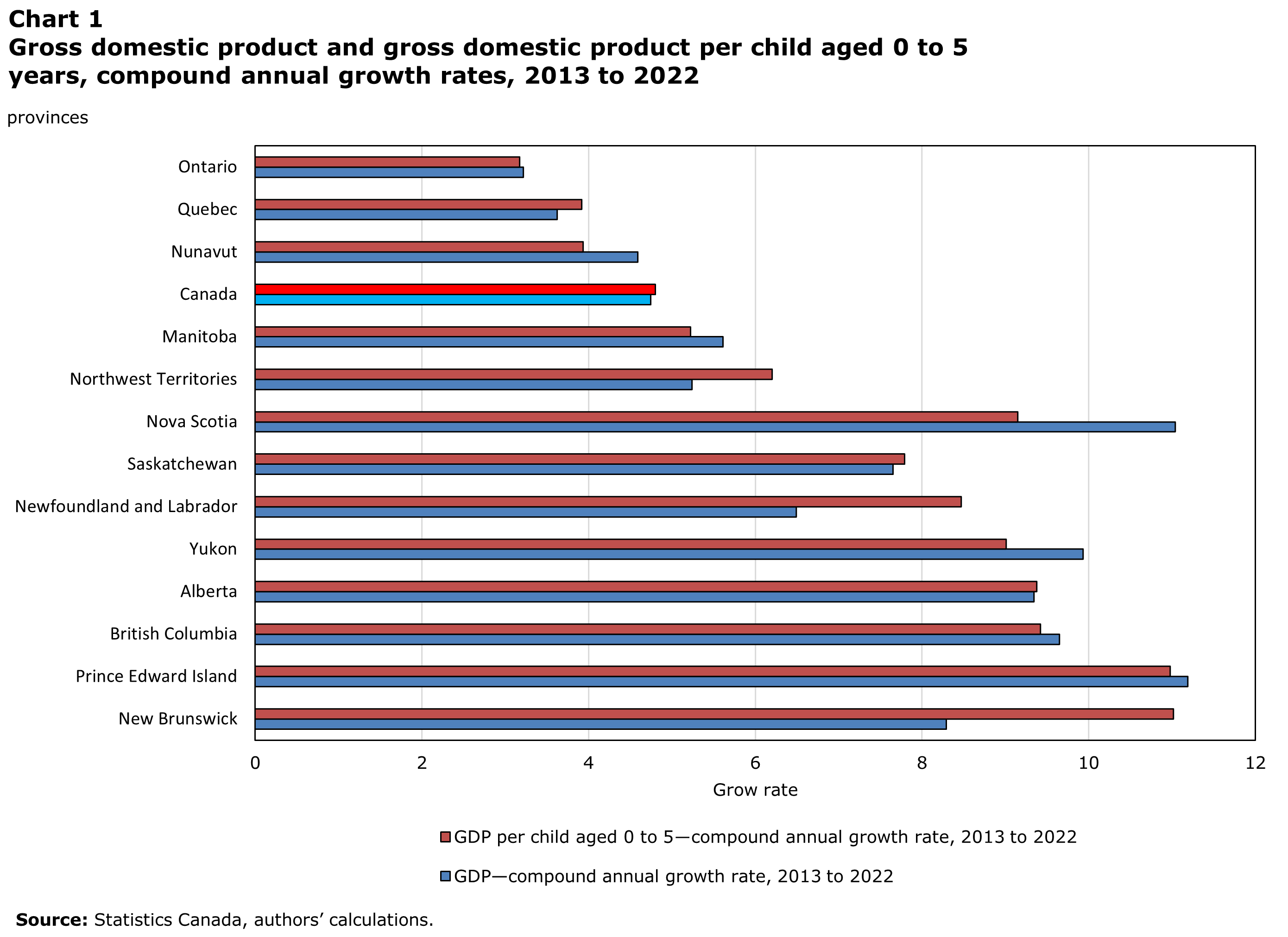

As shown in Chart 1, provinces and territories with initially higher levels of GDP per child aged 0 to 5 tended to have lower growth, leading to a narrowing of regional differences over time. The exceptions are Yukon, which had high initial spending and strong growth, and Nunavut, which had low initial spending and weak growth. An important caveat is that these growth rates are based on nominal rather than real GDP, i.e., they do not account for inflation. Therefore, growth driven by increases in the quantity of child care cannot be distinguished from growth driven by increases in prices and wages.

Data table for Chart 1

| GDP—compound annual growth rate, 2013 to 2022 | GDP per child aged 0 to 5―compound annual growth rate, 2013 to 2022 | |

|---|---|---|

| Source: Statistics Canada, authors’ calculations. | ||

| New Brunswick | 8 | 11 |

| Prince Edward Island | 11 | 11 |

| British Columbia | 10 | 9 |

| Alberta | 9 | 9 |

| Yukon | 10 | 9 |

| Newfoundland and Labrador | 6 | 8 |

| Saskatchewan | 8 | 8 |

| Nova Scotia | 11 | 9 |

| Northwest Territories | 5 | 6 |

| Manitoba | 6 | 5 |

| Canada | 5 | 5 |

| Nunavut | 5 | 4 |

| Quebec | 4 | 4 |

| Ontario | 3 | 3 |

Business dynamics

To align with other Statistic Canada estimates, only businesses with at least one employee (here after called employer businesses) are included in business dynamics calculations (Statistics Canada, 2025b). As a result, most home-based child care businesses, which typically do not have employees, are excluded, and the estimates primarily capture centre-based child care. A business entry is when a business is present in a given year but not in the preceding year, while a business exit is when a business is not present in a given year but was present in the preceding year. Under these definitions, re-openings and temporary exits are included. In the context of child care businesses, exits imply that families have to search for new arrangements; therefore, higher exit rates are more disruptive for families and children.

Over the study period, entry rates were similar for all employer businesses and ELCC employer businesses (Archer et al.,

Table 5 presents entry and exit rates by business size for ELCC employer businesses. ELCC employer businesses with one to five employees had much higher entry and exit rates than ELCC employer businesses with six or more employees. For example, in 2022, the entry rate for ELCC businesses with one to five employees was 23.8%, compared with 8.2% for those with six or more employees, and the exit rate was 21.7%, compared with 3.3% for those with six or more employees. Note that businesses may reduce the number of employees before closing.

| 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | |

|---|---|---|---|---|---|---|---|---|---|

| rate | |||||||||

| Note: ELCC = early learning and child care.

Source: Statistics Canada, Canadian Employer-Employee Dynamics Database. |

|||||||||

| Entry rates | |||||||||

| All employer firms | 13.2 | 13.3 | 12.9 | 13.2 | 13.2 | 13.3 | 11.0 | 17.5 | 15.6 |

| All ELCC employer firms | 14.4 | 14.1 | 13.7 | 12.3 | 14.4 | 12.3 | 11.0 | 13.1 | 13.9 |

| 1 to 5 employees | 22.0 | 21.9 | 22.0 | 20.2 | 23.8 | 20.2 | 19.7 | 22.3 | 23.8 |

| 6 or more employees | 7.4 | 7.2 | 6.7 | 6.0 | 7.1 | 6.7 | 5.2 | 7.4 | 8.2 |

| Exit rates | |||||||||

| All employer firms | 11.8 | 11.5 | 12.2 | 11.9 | 12.3 | 12.1 | 17.4 | 11.4 | 12.3 |

| All ELCC employer firms | 14.5 | 14.6 | 14.1 | 12.0 | 12.6 | 13.6 | 14.3 | 12.3 | 10.1 |

| 1 to 5 employees | 24.4 | 25.2 | 25.3 | 22.1 | 23.6 | 25.4 | 28.7 | 26.1 | 21.7 |

| 6 or more employees | 5.3 | 5.2 | 4.7 | 4.0 | 4.2 | 4.9 | 4.9 | 3.8 | 3.3 |

The rate at which new businesses exit over time is typically examined using a survival curve, which is calculated for a specific cohort. In year 0, the cohort enters the market, and the survival curve shows the proportion of businesses that remain in each subsequent year. These survival curves are based on permanent exits. Businesses that temporarily exit the market (or had no employees) are still included in the year of temporary exit. As shown in Table 6, survival curves were higher for the 2016 cohort (relative to 2014 and 2015 cohorts) and the 2020 cohort (relative to all previous years), suggesting that more recent ELCC employer businesses were surviving

| years after entry | 0 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 9 |

|---|---|---|---|---|---|---|---|---|---|

| percentage of businesses remaining active | |||||||||

|

|||||||||

| 2014 cohort | 100.0 | 74.0 | 63.6 | 56.0 | 50.9 | 45.9 | 41.3 | 37.6 | 33.7 |

| 2015 cohort | 100.0 | 73.5 | 62.2 | 55.7 | 50.5 | 46.1 | 42.1 | 38.3 | ... not applicable |

| 2016 cohort | 100.0 | 81.6 | 70.2 | 61.2 | 53.9 | 47.8 | 43.0 | ... not applicable | ... not applicable |

| 2017 cohort | 100.0 | 81.1 | 71.1 | 61.3 | 54.4 | 49.3 | ... not applicable | ... not applicable | ... not applicable |

| 2018 cohort | 100.0 | 80.4 | 70.3 | 61.1 | 55.6 | ... not applicable | ... not applicable | ... not applicable | ... not applicable |

| 2019 cohort | 100.0 | 81.4 | 69.8 | 61.4 | ... not applicable | ... not applicable | ... not applicable | ... not applicable | ... not applicable |

| 2020 cohort | 100.0 | 84.9 | 74.4 | ... not applicable | ... not applicable | ... not applicable | ... not applicable | ... not applicable | ... not applicable |

| 2021 cohort | 100.0 | 84.2 | ... not applicable | ... not applicable | ... not applicable | ... not applicable | ... not applicable | ... not applicable | ... not applicable |

Conclusion

From 2013 to 2022, the GDP of the child care industry grew rapidly, despite a decrease in the number of child care businesses. This pattern reflects a concentration of larger, incorporated businesses with employees in the child care market, especially after 2015. Specifically, the number of unincorporated businesses (typically associated with home-based child care businesses) fell, while incorporated businesses (typically associated with licensed centre-based child care) made up a greater proportion of businesses and generated a greater proportion of GDP over the study period. This phenomenon was not yet apparent from previous estimates, which were available only through 2016 (Archer et al., 2021). This change in the composition of the industry accelerated at the beginning of the COVID-19 pandemic in 2020.

GDP grew rapidly over the period studied, and GDP from government transfers and expenditures grew more rapidly than GDP at factor cost (GDP generated within child care businesses). Growing employee compensation was the largest driver of GDP at factor cost. Growth in GDP at factor cost and GDP from government transfers and expenditures increased significantly after the introduction of the CWELCC system in 2021.

This report departs from the 2021 report in its calculation of entry and exit rates, which are now based on businesses with employees only, consistent with Statistic Canada’s official estimates. In the 2021 report, all ELCC businesses were included, and ELCC businesses had higher entry and exit rates than all private sector businesses. In the current report, ELCC employer businesses have similar entry rates to those of all private sector businesses, but higher exit rates.

There are other important caveats to this study. Administrative data are used to capture most businesses, and imputation is applied to account for expenditures in the education system (i.e., for 4- and 5-year-olds in kindergarten), allowing for comparisons across provinces. However, complete data on charities’ gross operating surplus are not always available, meaning charities are underrepresented in GDP calculations. While the report accurately captures charities in terms of counts and compensation to employees (based on T4 slips), they are not fully reflected in the GDP estimates.

The administrative data used to compile the report also do not delineate licensed and unlicensed child care businesses. While unincorporated businesses are less likely to be licensed and incorporated businesses with multiple employees are likely to be licensed, there is no certainty for individual businesses. Similarly, the data do not inform about the number of child care spaces, divisions between full- and part-time child care, or the quality of child care. Some of these dimensions could be addressed in future work by linking the CEEDD to other data sources.

References

Archer, J., Duhamel, B., Macdonald, R., Watt, J., & Yam, H.N. (2021). The early learning and child care industry in Canada: Business characteristics and industry gross domestic product. Economic and Social Reports, 1(8).

Findlay, L., & Wei, L. (2021). Use of child care for children younger than six during COVID-19. Economic and Social Reports, 1(8).

Hacioglu, B., Burns, S., Davidson, A., Perlman, M., & White, L. A. (2024). Examining the Stability and Durability of Child Care Arrangements during the COVID-19 Pandemic in Canada. Canadian Public Policy, 50(3).

Employment and Social Development Canada (ESDC). (2025). Progress and impact of Canada-wide Early Learning and Child Care.

Landry, B., Macdonald, R., Tarassoff, P., & Watt, J. (2025). Purchasing Power Parities for Consumption and Household Income Across the Canadian Provinces and Territories (Analytical Studies: Methods and References, No. 58).

Macdonald, D. (2025). Cash cow: Assessing child care space creation progress. Canadian Centre for Policy Alternatives.

Department of Justice Canada. (2025). Canada Not-for-profit Corporations Act (S.C. 2009, c. 23).

Sinha, M. (2014). Childcare in Canada (Spotlight on Canadians: Results from the General Social Survey).

Statistics Canada. (2002). Gross Domestic Product by Industry (System of National Accounts). Statistics Canada.

Statistics Canada. (2010). A brief guide to the BR. Ottawa: Statistics Canada.

Statistics Canada. (2019). Statistics Canada Quality Guidelines (6th Ed.). Ottawa: Statistics Canada.

Statistics Canada. (2021). Survey on Early Learning and Child Care Arrangements, 2020. The Daily.

Statistics Canada. (2024). North American Industry Classification System (NAICS) Canada 2022 Version 1.0.

Statistics Canada. (2025a). Business Register (BR). Ottawa: Statistics Canada.

Statistics Canada. (2025b). Table 33-10-0164-01, Business Dynamics measures, by industry [Data table].

Statistics Canada. (2025c). Table 36-10-0711-01, Gross domestic product (GDP) at basic prices, by industry, provinces and territories (x 1,000,000) [Data table].

Statistics Canada. (2026). Table 17-10-0005-01, Population estimates on July 1, by age and gender [Data table].

United Nations, European Commission, International Monetary Fund, Organisation for Economic Co-operation and Development, and World Bank. (2025). System of National Accounts 2025.

Wise, J. (2023). Covid-19: WHO declares end of global health emergency. BMJ 381, 1041.

Zhang, S., Garner, R., Heidinger, L., & Findlay, L. (2021). Parents’ use of child care services and differences in use by mothers’ employment status. Insights on Canadian Society, July 2021.

- Date modified: