Economic and Social Reports

Housing, wealth and debt: How are young Canadians adapting to current financial and housing pressures?

DOI: https://doi.org/10.25318/36280001202400300004-eng

Text begins

Introduction

Barriers to important life cycle milestones and transitions have intensified in Canada. Sustained food inflation, elevated housing prices, and increasingly unaffordable rental costs across much of the country are casting a shadow over the homeownership dream for many households—and, in particular, for young families.Note

Young Canadians recently reported that they are less satisfied and less hopeful about the future (Statistics Canada, 2023). In 2022, concerns over rising prices led about one third of youth to reconsider buying a home or moving to a new rental. The current environment of higher borrowing costs and elevated housing and rental costs has different implications for Canadian households depending on where they are in their economic life cycle. This article provides an overview of household balance sheets and key financial metrics for households whose primary earner is less than 35 years of age of as they adjust to current market conditions and begin to build financial resilience.

Prospective young homeowners turning away from the housing market

Over the better part of the last decade, consumer spending has been a key source of economic growth, but it has also led to greater debt burdens. Today, Canada has the highest household debt to disposable income ratio in the G7, at 185% compared with an average of 125% for all G7 countries.Note Investments in housing, an important contributor to the buildup of household assets and debt, have long been critical for building wealth, especially among young households and middle class families. The sharp rise in debt servicing costs has left many households in a more precarious financial situation, compounded by increases in the costs of many household staples which persist as inflationary pressures ease.

The most recent data from the Distributions of household economic accounts suggest that younger households are starting to turn away from the housing market, as their overall mortgage balances have declined in recent quarters.Note While total mortgage liabilities grew by nearly $73 billion on a year-over-year basis in the third quarter of 2023, households where the primary earner is under 35 years of age were the only age cohort to reduce their mortgage burden.Note This suggests that young families may be choosing not to enter the housing market, paying off existing debt faster, or downgrading to more affordable accommodations. Lower balances in recent quarters also contrast with the sharp buildup of mortgage debt among young families early in the pandemic when many took advantage of more favourable borrowing conditions.

Data table for Chart 1

| Less than 35 years | 35 to 44 years | 45 to 54 years | 55 to 64 years | 65 years and over | |

|---|---|---|---|---|---|

| index (Q4 2019=100) | |||||

| 2019 | |||||

| Q4 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 |

| 2020 | |||||

| Q1 | 98.88 | 100.67 | 102.88 | 99.08 | 99.21 |

| Q2 | 100.83 | 102.82 | 105.74 | 102.08 | 103.01 |

| Q3 | 104.83 | 105.71 | 108.75 | 104.75 | 105.99 |

| Q4 | 106.25 | 106.19 | 109.02 | 104.95 | 107.26 |

| 2021 | |||||

| Q1 | 109.97 | 108.61 | 111.46 | 107.21 | 109.26 |

| Q2 | 115.75 | 113.65 | 116.60 | 112.26 | 113.85 |

| Q3 | 121.72 | 117.69 | 119.49 | 114.50 | 115.19 |

| Q4 | 118.85 | 116.15 | 117.93 | 112.82 | 113.61 |

| 2022 | |||||

| Q1 | 120.65 | 118.16 | 120.00 | 114.99 | 115.67 |

| Q2 | 123.18 | 121.40 | 123.21 | 118.23 | 118.15 |

| Q3 | 124.75 | 123.06 | 124.60 | 119.62 | 118.37 |

| Q4 | 123.43 | 123.53 | 125.38 | 120.65 | 119.51 |

| 2023 | |||||

| Q1 | 121.54 | 123.70 | 126.18 | 122.07 | 120.82 |

| Q2 | 120.03 | 124.44 | 127.87 | 124.80 | 123.38 |

| Q3 | 118.56 | 124.81 | 129.00 | 126.42 | 124.13 |

| Source: Statistics Canada, Distributions of Household Economic Accounts, Table 36-10-0660-01. | |||||

Household debt-to-disposable income ratios provide information on the extent to which households are able to manage their debt at current income levels. The amount of debt that young households are carrying relative to their income levels has declined over the past year, reflecting the reduction in mortgage balances coupled with robust wage growth. In 2023, the disposable income of young households rose by 2.5%, reflecting broad-based wage increases, while their average net saving rose 9.2%. The household debt-to-income ratio of young households fell to 165.2% in the third quarter of 2023, about 10 percentage points below its level during the same quarter in 2022.

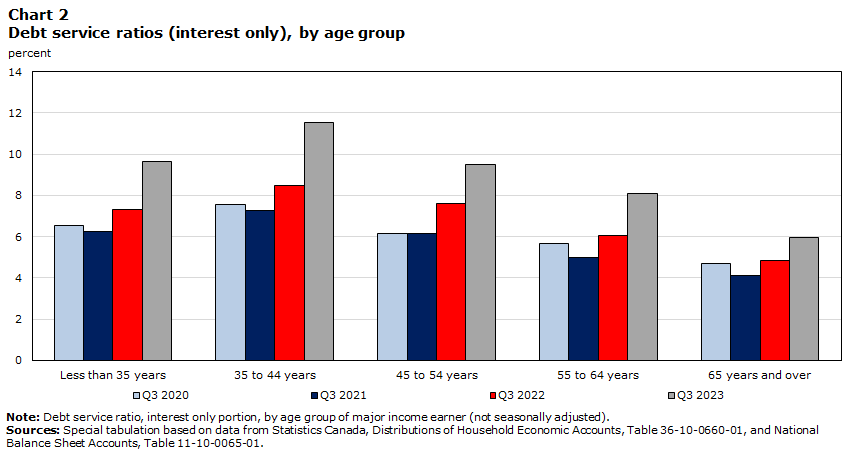

While their mortgage balances and debt to income ratios have fallen, debt servicing costs have increased markedly. Younger households have experienced some of the largest increases in their debt service ratios over the past year, as they tend to have higher mortgage balances to pay off than older households at this point in their life cycle, and the costs of servicing mortgage debt has risen due to higher interest rates. Among those less than 35 years of age, the ratio of interest costs to disposable income rose 2.4 percentage points to 9.7% in 2023. Essentially, young households spent 10 cents of every dollar earned towards servicing their debt, up from around 7 cents in 2022.

Data table for Chart 2

| Q3 2020 | Q3 2021 | Q3 2022 | Q3 2023 | |

|---|---|---|---|---|

| percent | ||||

| Less than 35 years | 6.6 | 6.2 | 7.3 | 9.7 |

| 35 to 44 years | 7.6 | 7.3 | 8.5 | 11.5 |

| 45 to 54 years | 6.2 | 6.2 | 7.6 | 9.5 |

| 55 to 64 years | 5.7 | 5.0 | 6.1 | 8.1 |

| 65 years and over | 4.7 | 4.1 | 4.9 | 6.0 |

|

Note: Debt service ratio, interest only portion, by age group of major income earner (not seasonally adjusted). Sources: Special tabulation based on data from Statistics Canada, Distributions of Household Economic Accounts, Table 36-10-0660-01, and National Balance Sheet Accounts, Table 11-10-0065-01. |

||||

Housing continues to be critical for wealth creation

Housing has long been a critical source of wealth creation and financial security for Canadian families. Real estate represents about 55% of overall household wealth and mortgages account for about 75% of household debt. The importance of real estate is more pronounced among younger families (Chart 3). Housing assets account for 89% of their total wealth, making them more exposed to fluctuations in the real estate market. As households less than 35 years of age reduced the value of their real estate holdings over the past year, their wealth grew at a slower-than-average pace.

Data table for Chart 3

| Lowest wealth quintile | Second wealth quintile | Third wealth quintile | Fourth wealth quintile | Highest wealth quintile | Less than 35 years | 35 to 44 years | 45 to 54 years | 55 to 64 years | 65 years and over | Owner with mortgage | Owner without mortgage | Renter | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| dollars | |||||||||||||

| Financial assets | 11,543 | 81,448 | 222,019 | 486,096 | 1,985,955 | 167,702 | 344,949 | 736,178 | 904,923 | 626,037 | 521,134 | 973,578 | 206,022 |

| Real estate | 30,149 | 155,043 | 390,602 | 665,062 | 1,431,681 | 290,413 | 519,258 | 785,635 | 704,607 | 463,209 | 755,538 | 783,604 | 63,076 |

| Other non-financial assets | 15,938 | 36,179 | 51,813 | 67,644 | 112,236 | 39,900 | 61,690 | 76,265 | 71,762 | 45,334 | 73,975 | 68,610 | 27,131 |

| Mortgage liabilities | -25,328 | -100,320 | -162,461 | -171,143 | -187,919 | -129,667 | -233,024 | -235,234 | -106,604 | -26,520 | -333,963 | -21,459 | -10,729 |

| Other liabilities | -33,187 | -35,988 | -45,729 | -54,513 | -66,254 | -42,901 | -57,319 | -74,435 | -62,825 | -20,576 | -66,974 | -46,773 | -26,131 |

| Net worth (wealth) | -885 | 136,362 | 456,244 | 993,146 | 3,275,700 | 325,446 | 635,555 | 1,288,409 | 1,511,862 | 1,087,484 | 949,711 | 1,757,561 | 259,369 |

|

Note: Trends by age group reflect life cycle accumulation of wealth and debt. Source: Statistics Canada, Distributions of Household Economic Accounts, Table 36-10-0660-01. |

|||||||||||||

Risks to socio-economic mobility on the horizon

Economic pressures on young households are weighing on their future outlook. The Bank of Canada’s third quarter Canadian Survey of Consumer Expectations found that the gap between perceptions of inflation and actual inflation is unusually wide, particularly for young Canadians who may be responding to the sticker shock of cumulative price increases (2023). As noted, this may partly reflect spending on food and shelter, both of which have experienced sustained price increases that are felt acutely by renters, many of whom are younger households (Bank of Canada, 2023). In October 2023, people living in a rented dwelling (41.3%) were more likely to be experiencing difficulties meeting their financial needs than homeowners with a mortgage (35.5%) or without a mortgage (20.4%) (Statistics Canada, 2023).

Sustained affordability pressures related to shelter, if they persist over the long term, pose substantial risks for socio-economic mobility as it becomes increasingly difficult for young households with fewer resources to achieve important milestones related to financial resiliency, such as purchasing a home. Research at CIBC Economics has shown that down-payment gifts have become increasingly important for first time home buyers (2021). In 2021, the share of first-time buyers that received help from family members was just under 30%, up from 20% in 2015; during this period, the value of the average gift rose from $52,000 to $82,000. (Tal, 2021). The financial realities of those with limited access to parental supports may contribute to heightened inequality, particularly if important sources of wealth accumulation, such as owning a home, are delayed or become inaccessible to larger numbers of young Canadians.

Authors

James Gauthier is with the National Economic Accounts Division, Macroeconomic Accounts Branch, at Statistics Canada. Carter McCormack is with the Strategic Analysis, Publications and Training Division, Analytical Studies and Modelling Branch, at Statistics Canada.

References

Bank of Canada. 2023. Canadian Survey of Consumer Expectations – Third Quarter of 2023. Vol. 4.3, October 16, 2023.

Statistics Canada, 2024. Research to Insights: Disparities in wealth and debt among Canadian families. Catalogue no. 11-631-X.

Statistics Canada. 2023. Navigating Socioeconomic Obstacles: Impact on the Well-being of Canadian Youth. The Daily. September 20, 2023.

Statistics Canada. 2023. Labour Force Survey, October 2023. The Daily. November 3, 2023.

Statistics Canada. 2024. The Daily — Distributions of household economic accounts for income, consumption, saving and wealth of Canadian households, third quarter 2023 (statcan.gc.ca), January 22, 2024.

Statistics Canada. 2023. The Daily — National balance sheet and financial flow accounts, third quarter 2023 (statcan.gc.ca), December 13, 2023.

Statistics Canada. 2024. Nationally, renters report lower quality of life than homeowners. The Daily. February 19, 2024.

Tal, Benjamin. 2021. Gifting for a down payment – perspective. Economics in Focus. October 25, 2021.

- Date modified: