VISTA on the Agri-food Industry and the Farm Community

Effects of the Crop Reporting Cycle on Field Crop Statistics

Archived Content

Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject to the Government of Canada Web Standards and has not been altered or updated since it was archived. Please "contact us" to request a format other than those available.

by Omar Youssouf

Introduction

The Field Crop Reporting Series produces national and provincial estimates on seeded and harvested areas, yields, production and on-farm stocks over the course of a crop cycle. The data provide an overview of field crops and insight into the farming industry in Canada. The timing of the survey collection period is crucial and ensures a timely and accurate picture of the crop situation, thereby meeting the industry need for these data.

The March farm survey provides preliminary area estimates for the type of crop area that, at the time of collection, farmers intend to seed. The acreage is often reported at a time when there is still snow on the ground. However, the data on seeding intentions are used by Agriculture and Agri-Food Canada (AAFC) to calculate its first grain estimates for the summer farm income forecast.

The June farm survey provides the final estimates of the area that farmers actually seeded. The preliminary data obtained in the July farm survey provide AAFC with an early indication of production for the upcoming crop year. These estimates are used as a basis for subsequent surveys throughout the year (harvested area, yield and production).

The model-based principal field crop estimates released in September provide yield and production data for select crops later in the season when crops are closer to maturity or in some cases when harvest has begun. Prior to 2016, traditional survey methodology was used to collect yield and production data for all crops at this time of year. In 2016, the September farm survey was replaced with model-based estimates derived using an innovative approach developed by Statistics Canada and AAFC.

Lastly, the November farm survey collects final yield and production data once harvest is finished, except for a few crops for which harvest may continue later into the fall.

In the field crop industry, several factors have a significant impact on farmers’ seeding decisions, affecting the preliminary intention (March) and final seeded area (June) data that producers provide to Statistics Canada. Factors such as price variability, weather events and socioeconomic influences have important impacts on seeded area estimates. With regard to production estimates, weather variances that occur between all the surveys can explain differences between estimates.

Comparisons between March seeding intentions and June final seeded area

Canola and all wheat

Trends published regarding the seeding area of Canada’s two top crops—canola and all wheat—were consistent when the March and June surveys were compared (charts 1 and 2) from 2008 to 2018.

From 2008 to 2014, the canola area estimates from the June surveys were an average of 4.4% higher than those from the March occasion. The difference between the two survey occasions decreased to an average of 3.5% from 2015 to 2018.

Trends in seeded area estimates for all wheat were similar in the two survey occasions. From 2008 to 2018, the difference between the March and June estimates of actual seeded area varied from almost 0.0% in 2008 to a maximum difference of 4.7% in 2011.

Data table for Chart 1

| March seeded area | June seeded area | |

|---|---|---|

| thousands of acres | ||

| 2008 | 14,805 | 15,812 |

| 2009 | 14,990 | 15,825 |

| 2010 | 16,907 | 17,895 |

| 2011 | 19,225 | 19,800 |

| 2012 | 20,372 | 21,273 |

| 2013 | 19,133 | 19,738 |

| 2014 | 19,801 | 20,228 |

| 2015 | 19,416 | 19,840 |

| 2016 | 19,345 | 20,020 |

| 2017 | 22,387 | 22,837 |

| 2018 | 21,383 | 22,740 |

| Source: Statistics Canada, Field Crop Reporting Series, 2008 to 2018. | ||

Data table for Chart 2

| March seeded area | June seeded area | |

|---|---|---|

| thousands of acres | ||

| 2008 | 25,109 | 25,100 |

| 2009 | 25,161 | 24,932 |

| 2010 | 23,221 | 22,720 |

| 2011 | 24,724 | 23,568 |

| 2012 | 24,325 | 23,812 |

| 2013 | 26,618 | 25,906 |

| 2014 | 24,766 | 24,087 |

| 2015 | 24,765 | 24,142 |

| 2016 | 23,846 | 23,177 |

| 2017 | 23,182 | 22,361 |

| 2018 | 25,259 | 24,710 |

| Source: Statistics Canada, Field Crop Reporting Series, 2008 to 2018. | ||

Soybeans and corn for grain

While soybeans and corn for grain have a later growing season, Statistics Canada’s March survey results are in line with the final June survey results (charts 3 and 4). From 2008 to 2011, the average difference between the two survey occasions for corn for grain estimates was -2.2%. From 2008 to 2018, the difference between the March and June survey results was at its lowest in 2015 at -0.5%, while the highest difference was in 2014 at -7.4%.

Canada’s soybean area grew significantly from 3.0 million acres in 2008 to 6.3 million acres in June 2018. Statistics Canada was able to capture the expansion of soybean acreage in its March estimates, a trend confirmed in the June final estimates. From 2008 to 2018, the average percentage difference between the estimates from the two surveys was +3.9%. In 2008, the difference between the survey results was at its lowest at +0.3%. In contrast, the largest relative difference between the estimates from the two surveys was +8.7% in 2012.

Data table for Chart 3

| March seeded area | June seeded area | |

|---|---|---|

| thousands of acres | ||

| 2008 | 2,985 | 2,993 |

| 2009 | 3,284 | 3,476 |

| 2010 | 3,532 | 3,724 |

| 2011 | 3,757 | 3,885 |

| 2012 | 3,969 | 4,316 |

| 2013 | 4,294 | 4,589 |

| 2014 | 5,264 | 5,583 |

| 2015 | 5,375 | 5,420 |

| 2016 | 5,306 | 5,465 |

| 2017 | 6,956 | 7,282 |

| 2018 | 6,452 | 6,320 |

| Source: Statistics Canada, Field Crop Reporting Series, 2008 to 2018. | ||

Data table for Chart 4

| March seeded area | June seeded area | |

|---|---|---|

| thousands of acres | ||

| 2008 | 3,005 | 2,975 |

| 2009 | 3,084 | 3,041 |

| 2010 | 3,016 | 2,981 |

| 2011 | 3,211 | 3,041 |

| 2012 | 3,562 | 3,638 |

| 2013 | 3,813 | 3,645 |

| 2014 | 3,369 | 3,119 |

| 2015 | 3,268 | 3,252 |

| 2016 | 3,477 | 3,330 |

| 2017 | 3,751 | 3,576 |

| 2018 | 3,758 | 3,634 |

| Source: Statistics Canada, Field Crop Reporting Series, 2008 to 2018. | ||

Barley and oats

As is the case for other principal field crops, Statistics Canada’s area estimates for barley and oats consistently exhibit the same trends between the two survey occasions (charts 5 and 6). For oat estimates, the lowest percentage difference between the estimates from the two surveys was in 2013 at -0.2%, while the greatest percentage difference was in 2012 at -9.4%. Over the last five years, the difference between the March and June estimates was, on average, below 5.0%.

For barley, the lowest percentage difference between the two estimates was in 2015 at +0.5%. The highest percentage difference was -8.9% in 2011, a year when severe flooding occurred across the nation.

Data table for Chart 5

| March seeded area | June seeded area | |

|---|---|---|

| thousands of acres | ||

| 2008 | 4,485 | 4,382 |

| 2009 | 3,955 | 3,879 |

| 2010 | 3,992 | 3,738 |

| 2011 | 4,056 | 3,814 |

| 2012 | 3,393 | 3,074 |

| 2013 | 3,379 | 3,371 |

| 2014 | 3,188 | 3,046 |

| 2015 | 3,645 | 3,403 |

| 2016 | 2,972 | 2,861 |

| 2017 | 3,419 | 3,220 |

| 2018 | 3,148 | 3,053 |

| Source: Statistics Canada, Field Crop Reporting Series, 2008 to 2018. | ||

Data table for Chart 6

| March seeded area | June seeded area | |

|---|---|---|

| thousands of acres | ||

| 2008 | 9,332 | 9,072 |

| 2009 | 9,476 | 8,778 |

| 2010 | 8,344 | 8,052 |

| 2011 | 7,833 | 7,139 |

| 2012 | 7,968 | 7,365 |

| 2013 | 7,240 | 7,175 |

| 2014 | 6,311 | 6,089 |

| 2015 | 6,478 | 6,511 |

| 2016 | 6,777 | 6,385 |

| 2017 | 5,880 | 5,771 |

| 2018 | 6,059 | 6,499 |

| Source: Statistics Canada, Field Crop Reporting Series, 2008 to 2018. | ||

Preliminary July and September production estimates compared to final November production

Canola and all wheat

For canola, the greatest percentage difference between the July and November survey estimates was in 2015 at 29.1%, while the lowest was in 2011 at +7.4%. From 2008 to 2017, the average difference between the July estimate and final production in November was 13.7%, compared with an average difference of 10.6% between September and November.

The difference between the July and November survey results for all wheat production estimates was at its lowest in 2012 at 0.7%, while the greatest difference was in 2013 at +22.8%. The average difference between the July estimate and November production was 9.5%, falling to 6.1% when the September estimate is compared with November final production.

Results show that the September occasion consistently provides estimates closer to the final November results. The crops are further advanced in the growing season, and farmers are able to provide better estimates about harvest and yield.

In 2016, Statistics Canada began using a yield-model approach, which incorporates remote sensing technology to produce estimates of yields. Results from this new approach have been consistent with September data produced using traditional survey techniques. Specifically, both the survey and the yield-model data for September align more closely with final production data from November than preliminary estimates from July.

In the last decade, relative differences between preliminary and final production estimates for canola and all wheat were on average greater than the differences for the other major field crops (charts 7 and 8).

Data table for Chart 7

| July production | September production | November production | |

|---|---|---|---|

| thousands of tonnes | |||

| 2008 | 10,375 | 10,870 | 12,643 |

| 2009 | 9,541 | 10,270 | 11,825 |

| 2010 | 10,867 | 10,430 | 11,866 |

| 2011 | 13,192 | 12,928 | 14,164 |

| 2012 | 15,409 | 13,359 | 13,309 |

| 2013 | 14,734 | 15,963 | 17,960 |

| 2014 | 13,908 | 14,080 | 15,555 |

| 2015 | 13,343 | 14,298 | 17,231 |

| 2016 | 17,024 | 18,384 | 18,424 |

| 2017 | 18,203 | 19,708 | 21,313 |

| Source: Statistics Canada, Field Crop Reporting Series, 2008 to 2017. | |||

Data table for Chart 8

| July production | September production | November production | |

|---|---|---|---|

| thousands of tonnes | |||

| 2008 | 25,426 | 27,266 | 28,611 |

| 2009 | 23,614 | 24,581 | 26,515 |

| 2010 | 22,659 | 22,205 | 23,167 |

| 2011 | 24,076 | 24,160 | 25,261 |

| 2012 | 27,012 | 26,733 | 27,205 |

| 2013 | 30,562 | 33,026 | 37,529 |

| 2014 | 27,704 | 27,481 | 29,281 |

| 2015 | 24,625 | 26,061 | 27,594 |

| 2016 | 30,487 | 31,530 | 31,729 |

| 2017 | 25,541 | 27,130 | 29,984 |

| Source: Statistics Canada, Field Crop Reporting Series, 2008 to 2017. | |||

Soybeans and corn for grain

The difference between the July and November survey estimates for soybeans varied from -0.3% in 2017 to a maximum difference of +11.9% in 2012. From 2008 to 2017, final soybean production estimates were on average 6.6% greater than the preliminary production figures captured in July (Chart 9). The overall average difference fell to 4.6% when the September estimates were compared with final production from November.

The average difference between the July and November production estimates for corn for grain was virtually the same as the difference for soybeans—final production estimates were on average 6.5% greater than the July estimates (chart 10). The lowest relative difference between the estimates from the two surveys was +0.5% in 2014, and the greatest difference occurred in 2012 at +11.6%. The average difference between the September estimate and November final production for corn for grain was lower than the difference between the July estimate and November final production, falling to 5.3%.

Soybeans and corn for grain start to mature in September. This causes uncertainty with regards to the reporting of production figures in July. Regardless, Statistics Canada July survey results have been in line with the final November estimates on numerous occasions.

Data table for Chart 9

| July production | September production | November production | |

|---|---|---|---|

| thousands of tonnes | |||

| 2008 | 3,167 | 3,240 | 3,336 |

| 2009 | 3,483 | 3,597 | 3,504 |

| 2010 | 3,951 | 4,028 | 4,345 |

| 2011 | 3,862 | 3,921 | 4,246 |

| 2012 | 4,405 | 4,280 | 4,929 |

| 2013 | 4,798 | 4,817 | 5,198 |

| 2014 | 5,901 | 5,961 | 6,049 |

| 2015 | 5,857 | 5,928 | 6,235 |

| 2016 | 5,827 | 6,058 | 6,463 |

| 2017 | 7,743 | 8,321 | 7,717 |

| Source: Statistics Canada, Field Crop Reporting Series, 2008 to 2017. | |||

Data table for Chart 10

| July production | September production | November production | |

|---|---|---|---|

| thousands of tonnes | |||

| 2008 | 9,892 | 9,893 | 10,592 |

| 2009 | 9,437 | 9,739 | 9,561 |

| 2010 | 10,823 | 10,865 | 11,715 |

| 2011 | 9,983 | 10,067 | 10,689 |

| 2012 | 11,703 | 11,576 | 13,060 |

| 2013 | 13,075 | 12,943 | 14,194 |

| 2014 | 11,431 | 11,397 | 11,487 |

| 2015 | 12,312 | 12,204 | 13,559 |

| 2016 | 12,349 | 13,118 | 13,193 |

| 2017 | 13,645 | 14,313 | 14,095 |

| Source: Statistics Canada, Field Crop Reporting Series, 2008 to 2017. | |||

Barley and oats

In the last decade, barley final production estimates were on average relatively close to the July and September estimates when compared with those for other principal field crops (Chart 11). Barley estimates in November were on average 2.1% greater than the July estimate. The difference ranged from ‑15.7% in 2012 to a maximum of +16.2% in 2013. The average difference between the September estimate and the November estimate was slightly higher, at 2.2%.

Oat production figures were on average 4.2% greater in July than in November (Chart 12). The difference ranged from +33.7% in 2013 to -5.7% in 2009. When the September production estimates were compared to the final November estimates, the average difference fell to 2.9%.

When reporting production figures in July, farmers rely on their best assessment given the growth stage of the crop at the time of the interview. Although predicting growing conditions and their impact on production figures remains a challenge for anyone in the agricultural industry, the preliminary July estimates have proven to be an important indicator of final production figures.

Data table for Chart 11

| July production | September production | November production | |

|---|---|---|---|

| thousands of tonnes | |||

| 2008 | 10,876 | 11,219 | 11,781 |

| 2009 | 8,948 | 9,165 | 9,517 |

| 2010 | 8,488 | 8,259 | 7,605 |

| 2011 | 8,274 | 7,898 | 7,755 |

| 2012 | 9,507 | 8,591 | 8,012 |

| 2013 | 8,807 | 9,247 | 10,237 |

| 2014 | 7,163 | 7,120 | 7,119 |

| 2015 | 7,305 | 7,610 | 8,226 |

| 2016 | 8,704 | 8,562 | 8,784 |

| 2017 | 7,212 | 7,306 | 7,891 |

| Source: Statistics Canada, Field Crop Reporting Series, 2008 to 2017. | |||

Data table for Chart 12

| July production | September production | November production | |

|---|---|---|---|

| thousands of tonnes | |||

| 2008 | 4,061 | 4,321 | 4,273 |

| 2009 | 2,967 | 2,900 | 2,798 |

| 2010 | 2,392 | 2,321 | 2,298 |

| 2011 | 2,886 | 2,887 | 2,997 |

| 2012 | 2,994 | 2,939 | 2,684 |

| 2013 | 2,907 | 3,163 | 3,888 |

| 2014 | 2,639 | 2,686 | 2,908 |

| 2015 | 3,312 | 3,292 | 3,428 |

| 2016 | 3,018 | 2,976 | 3,147 |

| 2017 | 3,685 | 3,802 | 3,724 |

| Source: Statistics Canada, Field Crop Reporting Series, 2008 to 2017. | |||

Impact of weather events on seeded area and production estimates

Preliminary and final seeded area

The field crop industry is heavily dependent on weather since the weather plays a major role in determining the success of a crop. Despite all other factors, weather events could result in late seeding or land left idle.

The year 2011 serves as a prime example of how weather variability and its effect on seeding can cause differences in area estimates published by the Field Crop Reporting Series between March and June. In 2011, temperatures across Canada, including the Prairies, where the majority of field crops are grown, were below average (Map 1).

Map 1

Description for Map 1

"Monthly Mean Temperature Difference from Normal (National), March 2011"

This map image represents Canada in static scale details the mean temperature difference from normal in March 2011

The mean temperature differences were at least 2.0 degrees Celsius below normal for the majority of western Canada. All other regions experienced no difference, to above normal temperature difference from normal.

Source: Agriculture and Agri-Food Canada, Drought Watch Map Archive.

As the growing season progressed, planting conditions, such as heavy rains (Map 2), and later-than-normal snow melt resulted in severe flooding in some parts of the Prairies. This left several thousand acres of land unplanted. Although 2011 is an extreme example, more moderate variability in weather and even economic factors can result in farmers altering their seeding decisions between March and June.

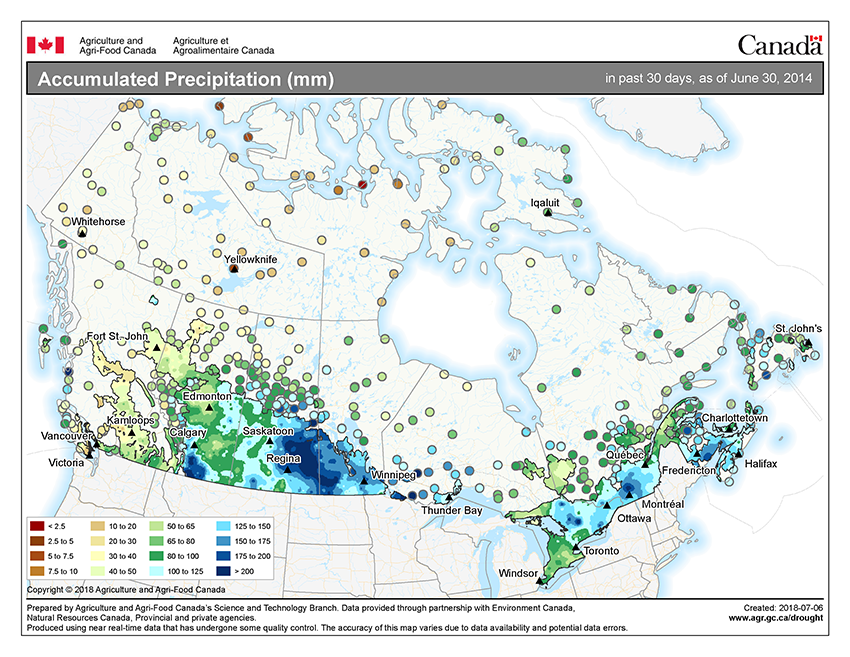

Map 2

Description for Map 2

"1 Month (30 Days) Accumulated Precipitation (National), May 22, 2011 to June 20, 2011"

This map image represents Canada in static scale details the accumulated precipitation between May 22, 2011 to June 20, 2011.

The accumulated precipitation ranged between 70 to 250 mm for the majority of cropable land in western Canada. All other regions experienced accumulated precipitation ranging from 10 to 100 mm.

Source: Agriculture and Agri-Food Canada, Drought Watch Map Archive.

Chart 13 indicates the percentage differences between the March and June survey results for all six major field crops in Canada from 2008 to 2018. The largest difference between seeding intentions and final seeding estimates occurred in 2011, when the average percentage difference between the two occasions for the six major field crops was -3.1%. This further confirms that the variability of weather events between survey collection periods can influence survey results.

Data table for Chart 13

| Canada | Average difference |

|---|---|

| percent | |

| 2008 | 0.2 |

| 2009 | 0.0 |

| 2010 | -0.3 |

| 2011 | -3.1 |

| 2012 | -0.6 |

| 2013 | 0.3 |

| 2014 | -1.6 |

| 2015 | -1.0 |

| 2016 | -1.7 |

| 2017 | -1.5 |

| 2018 | 0.5 |

|

Note: The average change represents the sum of the acreage of the six major field crops when comparing March and June seeded area estimates. Source: Statistics Canada, Field Crop Reporting Series, 2008 to 2018. |

|

Similar weather events occurred in 2014, when a late snow melt coupled with heavy precipitation near planting season caused farmers to change their seeding intentions (Maps 3 and 4). During this year, the relative difference between the estimates for the six major field crops from the two surveys ranged from ‑7.4% to 6.1%. In the same year, canola estimates accounted for the largest increase in acreage between the two occasions at +427,000 acres, while areas for all wheat varieties accounted for the largest difference at -680,000 acres.

Map 3

Description for Map 3

"Monthly Mean Temperature Difference from Normal (National), March 2014"

This map image represents Canada in static scale details the mean temperature difference from normal in March 2014.

The mean temperature differences were below normal for the majority of Canada.

Source: Agriculture and Agri-Food Canada, Drought Watch Map Archive.

Map 4

Description for Map 4

"Accumulated Precipitation (mm), in past 30 days, as of June 30, 2014"

This map image represents Canada in static scale details the accumulated precipitation in the past 30 days as of June 30, 2014.

The accumulated precipitation ranged between 100 to 200 mm for regions encompassing most of Saskatchewan, southern portions of Manitoba, eastern regions of Ontario and southern part of Quebec. The vast majority of the Maritimes also accumulated similar ranges of precipitation. All other regions experienced precipitation between 10 to 100 mm.

Source: Agriculture and Agri-Food Canada, Drought Watch Map Archive.

Preliminary and final production estimates

The weather variations captured between the July and September preliminary production estimates and the November final productions contributed to the variability between the survey results. However, Statistics Canada was able to capture the direction of the final estimates of Canada’s top six major field crops with the July preliminary survey (charts 7 to 12).

For instance, at the time of both the July and September 2013 surveys, Prairies farmers reported that recent weather events, such as hail and heavy rain episodes, may have had adverse effects on some areas to be harvested. However, during the November 2013 survey, producers reported that, despite a late start to the spring seeding, weather conditions that prevailed up to the end of the summer led to higher yields. This was especially true in Western Canada, and it paved the way for what was referred to as the “bumper crop year”. July 2013 results pegged national canola production at 14.7 million tonnes; however, results from September occasion placed estimates at 16.0 million tonnes, closer to the November 2013 final production at 18.0 million tonnes (up 21.9% compared with July 2013). Similarly, all wheat production increased 22.8% from the 30.6 million tonnes estimated in July 2013 to 33.0 million tonnes in September and finally 37.5 million tonnes estimated in November 2013.

The year 2015 serves as another important example of how weather variances can influence estimates in the two survey occasions. At the time of the July 2015 survey, Alberta and Saskatchewan farmers reported concerns of lower yields and decreased harvestable areas because of excessively dry growing conditions. Leading up to harvest, soil conditions in Alberta and Saskatchewan improved. The early dry weather gave way to mid- to late-summer rains. As a result, expected yield improved through the latter parts of the growing season. Canola production was estimated at 13.3 million tonnes in July 2015 but increased to 14.3 million tonnes by September and was updated to 17.2 million tonnes in November 2015 (up 29.1% from the July 2015 estimate). Likewise, national barley production increased from the 7.3 million tonnes estimated in July 2015, to 7.6 million tonnes in September, to 8.2 million tonnes in November 2015.

Although weather can negatively affect the production estimates between July and November, Statistics Canada has captured instances when the opposite was true. For example, in 2012, producers in Western Canada reported weather conditions to be close to normal. However, during the November 2012 survey, the producers reported that disease coupled with hail had an impact on their canola yields. National canola production was 13.3 million tonnes in November, down 13.6% from the 15.4 million tonnes anticipated in July 2012, but in line with the September estimate, which projected 13.4 million tonnes. Similarly, national barley production was 8.0 million tonnes in November, down 15.7% from the 9.5 million tonnes expected in July 2012 and down 6.7% from the September estimate of 8.6 million tonnes. Eastern regions experienced favourable growing conditions, which contributed to higher yields of corn for grain and soybeans, which are predominantly grown in Eastern Canada. Corn for grain production increased 11.6% between the July and November survey occasions, while soybean production increased 11.9%.

Market conditions

Crop farming can also be affected by market conditions on a national or global scale. One such factor is the exchange rate and the role that it can play in crop planting decisions. Competitive pricing of Canadian agricultural goods in the global market can be affected by currency fluctuations. A weak currency can increase global demand for more competitively priced crops, thereby strengthening crop returns and encouraging farmers to seed specific crops. In contrast, high exchange rates can introduce a decrease in returns for the producer, causing a change in planting decisions.

Another market condition that can affect crop seeding intentions is a change in production with a stagnant demand. If demand for a specific crop remains low for a prolonged period of time, farmers who traditionally grew this crop may decide to diversify. As a result, farmers may turn to crops that are in high demand and more likely to result in higher returns. This could influence the crop planting intentions of farmers with low risk tolerance to change. A variety of factors, ranging from political to socioeconomic, can explain why some producers change their crop selection. In addition to those previously mentioned, other factors can result in changes to crop selection, including transportation issues, recent pest and disease issues, and tariffs imposed by foreign governments on Canadian agricultural goods.

Conclusion

By analyzing data obtained through Statistics Canada’s Field Crop Reporting Series, this article evaluates the differences between preliminary and final data related to the area and production of Canada’s six major field crops.

The accuracy of the March seeding intentions is strong, especially when general trends in crop area are compared. The relative changes between both datasets at the national level are minor. From 2008 to 2018, the average percentage difference at the national level in the preliminary acreage reports collected through the March farm survey ranged between +/-5.0% for Canada’s major field crops (i.e., wheat, canola, soybeans, barley, oats and corn for grain). On occasions when estimates for a particular crop exceeded +/-5.0%, factors such as weather usually played an important role. Weather events or market conditions can cause unexpected differences between the preliminary and final seeded area and production estimates. Regardless of these differences, Statistics Canada is accurately projecting the direction of the field crop estimates with data obtained through its preliminary surveys (March and July). Therefore, both the March and the July surveys serve as important indicators of final field crop statistics.

While production data collected in July and September tended to differ from final production data to varying extents depending on crop type, trends in estimated production were generally characterized correctly. Differences between production estimates and final production data can largely be attributed to weather events including excess or inadequate precipitation and temperature. In addition, the differences between the July and September estimated yields and November’s final production point allude to the inherent difficulty of predicting one’s crop production. Even in so-called “bumper crop years,” general optimism regarding yield is often muted because projecting one’s yield based on a visual inspection of standing crops is difficult.

| Seeded area | Canola | All Wheat | Soybeans | Barley | Oats | Corn for grain |

|---|---|---|---|---|---|---|

| thousand of acres | ||||||

| 2018 | ||||||

| March | 21,383 | 25,259 | 6,452 | 6,059 | 3,148 | 3,758 |

| June | 22,740 | 24,710 | 6,320 | 6,499 | 3,053 | 3,634 |

| % Difference | 6.3% | -2.2% | -2.0% | 7.3% | -3.0% | -3.3% |

| 2017 | ||||||

| March | 22,387 | 23,182 | 6,956 | 5,880 | 3,419 | 3,751 |

| June | 22,837 | 22,361 | 7,282 | 5,771 | 3,220 | 3,576 |

| % Difference | 2.0% | -3.5% | 4.7% | -1.9% | -5.8% | -4.7% |

| 2016 | ||||||

| March | 19,345 | 23,846 | 5,306 | 6,777 | 2,972 | 3,477 |

| June | 20,020 | 23,177 | 5,465 | 6,385 | 2,861 | 3,330 |

| % Difference | 3.5% | -2.8% | 3.0% | -5.8% | -3.7% | -4.2% |

| 2015 | ||||||

| March | 19,416 | 24,765 | 5,375 | 6,478 | 3,645 | 3,268 |

| June | 19,840 | 24,142 | 5,420 | 6,511 | 3,403 | 3,252 |

| % Difference | 2.2% | -2.5% | 0.8% | 0.5% | -6.6% | -0.5% |

| 2014 | ||||||

| March | 19,801 | 24,766 | 5,264 | 6,311 | 3,188 | 3,369 |

| June | 20,228 | 24,087 | 5,583 | 6,089 | 3,046 | 3,119 |

| % Difference | 2.2% | -2.7% | 6.1% | -3.5% | -4.4% | -7.4% |

| 2013 | ||||||

| March | 19,133 | 26,618 | 4,294 | 7,240 | 3,379 | 3,813 |

| June | 19,738 | 25,906 | 4,589 | 7,175 | 3,371 | 3,645 |

| % Difference | 3.2% | -2.7% | 6.9% | -0.9% | -0.2% | -4.4% |

| 2012 | ||||||

| March | 20,372 | 24,325 | 3,969 | 7,968 | 3,393 | 3,562 |

| June | 21,273 | 23,812 | 4,316 | 7,365 | 3,074 | 3,638 |

| % Difference | 4.4% | -2.1% | 8.7% | -7.6% | -9.4% | 2.2% |

| 2011 | ||||||

| March | 19,225 | 24,724 | 3,757 | 7,833 | 4,056 | 3,211 |

| June | 19,800 | 23,568 | 3,885 | 7,139 | 3,814 | 3,041 |

| % Difference | 3.0% | -4.7% | 3.4% | -8.9% | -6.0% | -5.3% |

| 2010 | ||||||

| March | 16,907 | 23,221 | 3,532 | 8,344 | 3,992 | 3,016 |

| June | 17,895 | 22,720 | 3,724 | 8,052 | 3,738 | 2,981 |

| % Difference | 5.8% | -2.2% | 5.4% | -3.5% | -6.4% | -1.2% |

| 2009 | ||||||

| March | 14,990 | 25,161 | 3,284 | 9,476 | 3,955 | 3,084 |

| June | 15,825 | 24,932 | 3,476 | 8,778 | 3,879 | 3,041 |

| % Difference | 5.6% | -0.9% | 5.8% | -7.4% | -1.9% | -1.4% |

| 2008 | ||||||

| March | 14,805 | 25,109 | 2,985 | 9,332 | 4,485 | 3,005 |

| June | 15,812 | 25,100 | 2,993 | 9,072 | 4,382 | 2,975 |

| % Difference | 6.8% | 0.0% | 0.3% | -2.8% | -2.3% | -1.0% |

| Average % change by crop type | 4.1% | -2.4% | 3.9% | -3.1% | -4.5% | -2.8% |

| Source: Statistics Canada, Field Crop Reporting Series, 2008 to 2018. | ||||||

| Production | Canola | All Wheat | Soybeans | Barley | Oats | Corn for grain |

|---|---|---|---|---|---|---|

| thousand of metric tonnes | ||||||

| 2017 | ||||||

| July | 18,203 | 25,541 | 7,743 | 7,212 | 3,685 | 13,645 |

| September | 19,708 | 27,130 | 8,321 | 7,306 | 3,802 | 14,313 |

| November | 21,313 | 29,984 | 7,717 | 7,891 | 3,724 | 14,095 |

| % Difference (July-Nov) | 17.1% | 17.4% | -0.3% | 9.4% | 1.1% | 3.3% |

| % Difference (Sept-Nov) | 8.1% | 10.5% | -7.3% | 8.0% | -2.1% | -1.5% |

| 2016 | ||||||

| July | 17,024 | 30,487 | 5,827 | 8,704 | 3,018 | 12,349 |

| September | 18,384 | 31,530 | 6,058 | 8,563 | 2,976 | 13,118 |

| November | 18,424 | 31,729 | 6,463 | 8,784 | 3,147 | 13,193 |

| % Difference (July-Nov) | 8.2% | 4.1% | 10.9% | 0.9% | 4.3% | 6.8% |

| % Difference (Sept-Nov) | 0.2% | 0.6% | 6.7% | 2.6% | 5.7% | 0.6% |

| 2015 | ||||||

| July | 13,343 | 24,625 | 5,857 | 7,305 | 3,312 | 12,312 |

| September | 14,297 | 26,061 | 5,928 | 7,610 | 3,292 | 12,204 |

| November | 17,231 | 27,594 | 6,235 | 8,226 | 3,428 | 13,559 |

| % Difference (July-Nov) | 29.1% | 12.1% | 6.5% | 12.6% | 3.5% | 10.1% |

| % Difference (Sept-Nov) | 20.5% | 5.9% | 5.2% | 8.1% | 4.1% | 11.1% |

| 2014 | ||||||

| July | 13,908 | 27,705 | 5,901 | 7,164 | 2,639 | 11,431 |

| September | 14,080 | 27,481 | 5,961 | 7,120 | 2,686 | 11,397 |

| November | 15,555 | 29,281 | 6,049 | 7,119 | 2,908 | 11,487 |

| % Difference (July-Nov) | 11.8% | 5.7% | 2.5% | -0.6% | 10.2% | 0.5% |

| % Difference (Sept-Nov) | 10.5% | 6.5% | 1.5% | 0.0% | 8.3% | 0.8% |

| 2013 | ||||||

| July | 14,735 | 30,562 | 4,798 | 8,807 | 2,907 | 13,075 |

| September | 15,963 | 33,026 | 4,817 | 9,247 | 3,163 | 12,943 |

| November | 17,960 | 37,530 | 5,198 | 10,237 | 3,888 | 14,194 |

| % Difference (July-Nov) | 21.9% | 22.8% | 8.3% | 16.2% | 33.7% | 8.6% |

| % Difference (Sept-Nov) | 12.5% | 13.6% | 7.9% | 10.7% | 22.9% | 9.7% |

| 2012 | ||||||

| July | 15,410 | 27,013 | 4,405 | 9,508 | 2,994 | 11,703 |

| September | 13,359 | 26,733 | 4,280 | 8,591 | 2,939 | 11,576 |

| November | 13,310 | 27,205 | 4,930 | 8,012 | 2,684 | 13,060 |

| % Difference (July-Nov) | -13.6% | 0.7% | 11.9% | -15.7% | -10.4% | 11.6% |

| % Difference (Sept-Nov) | -0.4% | 1.8% | 15.2% | -6.7% | -8.7% | 12.8% |

| 2011 | ||||||

| July | 13,193 | 24,076 | 3,862 | 8,274 | 2,886 | 9,983 |

| September | 12,928 | 24,160 | 3,921 | 7,898 | 2,887 | 10,067 |

| November | 14,165 | 25,261 | 4,246 | 7,756 | 2,997 | 10,689 |

| % Difference (July-Nov) | 7.4% | 4.9% | 9.9% | -6.3% | 3.8% | 7.1% |

| % Difference (Sept-Nov) | 9.6% | 4.6% | 8.3% | -1.8% | 3.8% | 6.2% |

| 2010 | ||||||

| July | 10,867 | 22,659 | 3,951 | 8,488 | 2,392 | 10,823 |

| September | 10,430 | 22,205 | 4,028 | 8,259 | 2,321 | 10,865 |

| November | 11,866 | 23,167 | 4,345 | 7,605 | 2,298 | 11,715 |

| % Difference (July-Nov) | 9.2% | 2.2% | 10.0% | -10.4% | -3.9% | 8.2% |

| % Difference (Sept-Nov) | 13.8% | 4.3% | 7.9% | -7.9% | -1.0% | 7.8% |

| 2009 | ||||||

| July | 9,541 | 23,614 | 3,483 | 8,948 | 2,967 | 9,437 |

| September | 10,270 | 24,581 | 3,597 | 9,165 | 2,900 | 9,739 |

| November | 11,825 | 26,515 | 3,504 | 9,517 | 2,798 | 9,561 |

| % Difference (July-Nov) | 23.9% | 12.3% | 0.6% | 6.4% | -5.7% | 1.3% |

| % Difference (Sept-Nov) | 15.1% | 7.9% | -2.6% | 3.8% | -3.5% | -1.8% |

| 2008 | ||||||

| July | 10,375 | 25,426 | 3,167 | 10,876 | 4,061 | 9,892 |

| September | 10,870 | 27,266 | 3,240 | 11,219 | 4,321 | 9,893 |

| November | 12,643 | 28,611 | 3,336 | 11,781 | 4,273 | 10,592 |

| % Difference (July-Nov) | 21.9% | 12.5% | 5.3% | 8.3% | 5.2% | 7.1% |

| % Difference (Sept-Nov) | 16.3% | 4.9% | 3.0% | 5.0% | -1.1% | 7.1% |

| Average % change by crop type (July-Nov) | 13.7% | 9.5% | 6.6% | 2.1% | 4.2% | 6.5% |

| Average % change by crop type (September-Nov) | 10.6% | 6.1% | 4.6% | 2.2% | 2.9% | 5.3% |

| Source: Statistics Canada, Field Crop Reporting Series, 2008 to 2017. | ||||||

- Date modified: