5 Discussion

Jan de Haan and Rens Hendriks

Previous | Next

5.1 Comparing GREG to

SPAR

The most interesting question arising from Section 4 is:

why are the GREG and SPAR index numbers so similar in spite of their very

different construction methods? It is not remarkable that the trends are

similar: although the GREG index does not rely on the matched-model

methodology, this index does aim at the same target as the SPAR index. If the

sample sizes and would approach the population size which in reality will of course never happen then both price indexes approach the value

change of the fixed housing stock. Put differently, the two methods are both

asymptotically unbiased or 'consistent'.

What may come as a surprise

is that the GREG index exhibits roughly the same amount of volatility over time

as the SPAR index. To understand the reason why, recall that, with OLS, the

regression residuals sum to zero in every time period. This implies and For the basic regression models (3.1) and (3.5),

the SPAR index can thus alternatively be written as

using (3.2) and (3.6) for and respectively, where and for short. There is a striking similarity

between the last expression on the right-hand sides of (5.1) and (3.10). The

only difference is that the SPAR index (5.1) divides the coefficients and by the sample means of appraisals, and whereas the GREG index (3.10) divides them

both by the fixed, non-stochastic population mean Essentially, the SPAR index is a fully

sample-based estimator of the GREG index.

Compared with the SPAR method, the GREG approach

eliminates one source of sampling error, i.e.,

the sampling variability of the mean appraisals. In accordance with generalized

regression theory, we would intuitively expect the GREG method to reduce the

sampling error of the price index and produce a less volatile time series

(under the reasonable assumption that and are uncorrelated across periods Put differently, while the GREG method has

been designed as an improvement over the ratio of sample means, we might have

expected it to work as a smoothing procedure for the SPAR index also. But, as

was shown in Section 4, in

practice this is hardly the case. This result can be explained as follows.

The variance reduction of

the GREG index relative to the SPAR depends on the value of the intercept terms

from the regressions in periods 0 and If the regression lines passed exactly through

the origin then the GREG index and SPAR index would both

be equal to the ratio of the slope coefficients and no reduction in variance would be

achieved. In the less extreme case, when and are close to 0 and the ratios and in (3.10) and (5.2) are very small compared to

and the GREG and SPAR indexes will differ only

slightly and the variance reduction will be marginal; see also the Appendix.

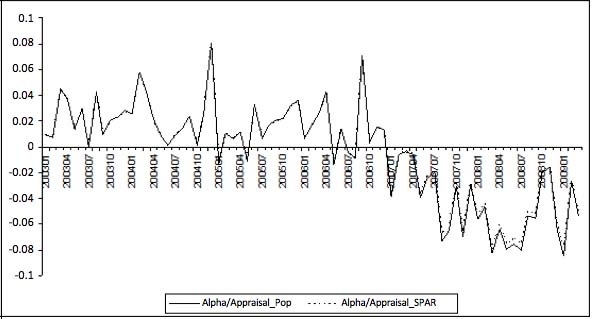

The latter is indeed what happens in practice, as can be

seen from Figures 5.1 and 5.2 where the values of and and those of are plotted over time. The ratios and are remarkably similar and small as compared

to the Although we cannot ignore those ratios, it is

the change in that mainly drives the GREG and SPAR indexes.

The SPAR index is not only a fully sample-based estimator of the GREG index, as

mentioned above, it appears to be almost as efficient.

Description for figure 5.1

Figure 5.1

Intercepts divided by appraisal means

Description for figure 5.2

Figure 5.2 Slope

coefficients

5.2 The volatility of

the slope coefficient

Several factors may have contributed to the volatility

of the slope coefficients in our regressions of selling prices on

appraisals and hence of the GREG and SPAR indexes. We will briefly discuss

three of these factors: sample mix change, heteroskedasticity and outliers.

A sample of houses can be viewed as a sample of

locations, or addresses, since houses are attached to the land they are built

on. A change in the sample mix is nothing else than a change in the observed

mix of locations at the lowest level. A location

mix change affects the sample composition in terms of the average quality

characteristics of the properties, such as the number of rooms, surface area, etc. In our simple framework, where we

observe only one (non-physical) characteristic, namely the appraised value, a

location mix change boils down to a change in the sample distribution of the

appraisals. This, together with any varying price changes across market

segments, induces a change in the sample distribution of the ratios which in turn leads to a change in in the two-variable regression model (3.5).

Other than by stratification there is little we can do

about the effect of changes in the sample mix of locations (but stratifying by

province and type of dwelling did not help much), so the volatility of

and therefore of the GREG and SPAR indexes,

will be difficult to reduce. Controlling for location at the address level is

also impossible in hedonic imputation methods. Here, the effect of (location)

mix change is mitigated by controlling for region plus a range of physical

characteristics. However, this does not necessarily mean that hedonic

imputation will produce more stable index series than the GREG or SPAR methods.

Most standard hedonic models fit the cross sectional data less well than our

model does, and the characteristics' coefficients typically exhibit a great

deal of variability over time. So maybe it is not surprising that Bourassa,

et al. (2006)

find that "the

SPAR index [….] reliably tracks house price changes, but exhibits less volatility

than index methods that require more parameter estimates.�

We can alternatively look at the variability of the

slope coefficient from a purely statistical perspective. It is well known that

in a two-variable model the OLS estimator can be written as

where denotes the sample correlation coefficient in

period between selling prices and appraisals, which

is equal to the square root of and are the corresponding sample standard

deviations. A comparison of Figures 4.1 and 5.2 suggests that sudden changes in

are largely responsible for the volatility of In December 2004 for example, a substantial

drop in coincides with a significant decrease of (and with a decrease in the GREG and SPAR

indexes, as shown by Figure 4.4).

Least squares regression can either be weighted or

unweighted. In the absence of heteroskedasticity,

i.e., when the variance of the errors

is constant, OLS should be used. Weighted Least Squares (WLS) is preferred if

there is evidence of heteroskedasticity; using appropriate weights, WLS will

lead to more stable coefficients than OLS. In this case the unweighted sample

sum of the residuals differs from zero so the estimator (3.9) has to be applied.

To facilitate the interpretation of the GREG index and the comparison with the

SPAR index, in Section 3 we assumed away the problem of heteroskedasticity and

restricted ourselves to OLS.

Note that the (OLS) GREG estimator (3.10) remains asymptotically design

unbiased if heteroskedasticity is present.

The most interesting form of (classical)

heteroskedasticity and, given our data set, the only form we

would have been able to reduce would arise if the variance of the errors of

our regression model (3.5) depended on the appraisal value, being the only

regressor. However, the residuals from our OLS regressions do not point to

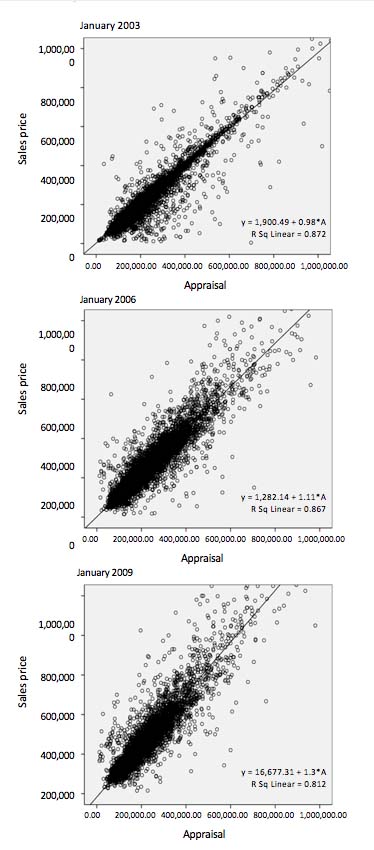

substantial heteroskedasticity of this type. This is illustrated in Figure 5.3

for three months, including the base period (January 2003), where the sale

prices are plotted against the appraisals; the regression lines are also given. To be sure, we also performed the

White (1980) test. This test did not point towards the presence of this form of

heteroskedasticity either.

Description for figure 5.3

Figure 5.3

Scatter plots and regression lines

Our initial data set of sale prices and appraisals

included some obvious outliers. To

estimate the GREG index we therefore made use of a cleaned data set that has

been prepared to compute the official Dutch house price index. Statistics Netherlands

applies several data cleaning procedures. Houses that were sold more than once

in a month are excluded from the data set. To delete entry errors and outliers

that may unduly affect the results, properties with sale prices or appraisals

below 10,000

or above 5,000,000

and properties with 'unrealistic' sale price-appraisal ratios are also removed. The removal of 'unrealistic'

observations is done by looking at the distribution of the logarithm of the

sale price-appraisal ratios; all observations are deleted for which the log

ratio differs more than 5 standard deviations from the mean. For more

information, see Statistics Netherlands (2008).

These procedures are rather arbitrary. For

regression-based estimators such as the GREG it is more appropriate to delete

observations with high leverage, i.e.,

to delete those sample units that have a big impact on the regression

coefficients when they are excluded from the sample. A well-known measure in

this context is the DFBETA of a sample unit (Cook and Weisberg 1982). Since the

SPAR can be written as a regression-based index, this measure could be used

here as well to detect and delete outliers. The scatter plots in Figure 5.3

show that the cleaned data set still contains some big outliers. Whether these

have high leverage, and whether removing them will reduce the volatility of the

and the GREG and SPAR indexes, remains to be

seen.

5.3 Some further

points

The GREG method is based on the premise of a fixed

housing stock. That is, we have assumed that there are no entries (e.g., newly-built houses) or exits

(discarded houses) and that housing quality remains fixed over time. Our approach is non-symmetric in

that we condition on the base period

stock. From an index number point of view we estimate a Laspeyres price index

for the housing stock where the quantities are all equal to 1 because every

house is treated as a unique property. An equally justifiable approach would be

to measure the price change of the current period stock, which includes

additions to the stock in each period, using a Paasche index. Taking the

geometric mean of both indexes would lead to the Fisher index. The Fisher index

is a preferred measure of price change due to its symmetric form. The

construction of a Fisher-type GREG index is, however, infeasible since the

Paasche component requires real time assessed values for houses that are new to

the stock, which are obviously not available.

The assumption of a fixed (base period) housing stock

can be relaxed through annual chaining, provided that the housing stock is

re-assessed annually. This is the current state of affairs in the Netherlands; in

the past, assessments were undertaken once every three or four years. Annual

updating of the appraisals might also adjust for quality changes of the

properties, to some extent at least, because the updated appraisals likely

account for major repairs, remodelling and depreciation.

One final remark is in order. For some purposes it is

desirable to decompose the overall house price index into two components: a

component that measures the change in the price of the structure and a

component that measures the change in the price of the land. Neither our GREG

method nor SPAR and repeat sales methods are fit for that purpose. Hedonic

imputation methods might work, notwithstanding practical problems like

multicollinearity; see

Diewert, de Haan and Hendriks (2012) for a first attempt. If data on

structure size, plot size and other price-determining attributes became

available for all properties in the housing stock, then we would be able to

estimate a "hedonic imputation GREG index�, including the land-structure split.

The chances of getting such data in the Netherlands are unfortunately

negligible.

Previous | Next